The relationship between output and cost is expressed in terms of cost function. The companies use cost function to minimize cost and maximize production efficiently.

Total cost

It is the full cost of producing any given level of output. The cost is divided into 2 parts

i. Firstly, total fixed cost does not vary with the level of output. For ex – land

ii. Secondly, total variable cost changes directly with the output. For ex – labour

Average cost

i. Firstly, Average total cost is the total cost per unit of output

ii. Secondly, Average fixed cost is the fixed cost per unit of output

iii. Thirdly, Average variable cost is the variable cost per unit of output

Marginal cost

Marginal cost is the proportionate change in total cost from the proportionate change in output

Short run cost

Short run cost is the cost where the quantity of one input is fixed and the quantity of other input varies. In this case, the land and machinery is fixed where as the other factors such as labour and capital vary with time. Thus expansion is done in hiring more labour and increasing capita

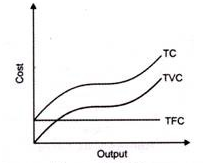

1.Total fixed cost (TFC)-

Total fixed cost remains fixed in short run period. The cost does not change with the change in the level of output.

These costs are also called indirect costs, overhead costs, historical costs, and unavoidable costs.

Definition

In the words of Ferguson, “Total fixed cost is the sum of the ‘short run explicit fixed costs and implicit costs incurred by the entrepreneur.”

From the above figure , we can see TFC curve is horizontal to X axis.TFC remains constant with proportionate change in the output.

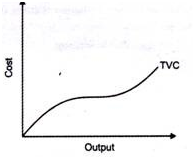

2. Total variable cost

Refers to the cost changes with the change in the level of output.

For instance – cost incurred in purchase of raw material, hiring labour, etc

Definition

According to Ferguson, “total variable cost is the sum of amounts spent for each of the variable inputs used”

If the output is zero, total variable cost is zero. These costs are also called prime costs, direct costs, and avoidable costs.

In the above figure, TVC changes with the change in the level of production

3. Total cost

Total cost is the sum of fixed and variable cost. It changes with the change in the level of production

Therefore, TC = TFC+TVC

In the above fig, initially total cost increases at diminishing rate, means the rate of cost increases with respect to less output. Later total cost increases at increasing rate, as cost increases with respect to output is more.

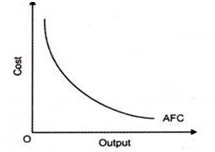

4. Average fixed cost (AFC)–

Refers to fixed cost of production divided by the quantity of output produced.

Therefore AFC= TFC/Output

AFC curve is declining in the above figure. The TFC remains constant as production increases, thus AFC falls

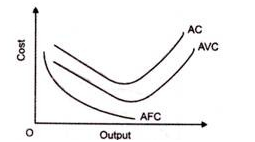

5. Average variable cost (AVC)

It refers to total variable cost divided by total production

AFC = TVC/Output

AVC decreases as the output increases. But after a point, AVC increases as the output increases. Thus, it is U shaped curve

6. Average cost of production (AC)

Refer to the total costs of production per unit of output.

therefore, AC= TC/Output

AC is also equal to the sum total of AFC and AVC. AC curve is also U-shaped curve as average cost initially decreases when output increases and then increases when output increases.

7. Marginal cost (MC)

Refers to change in total cost of production on addition unit of the product.

Similarly, MC = proportionate change in TC/ Proportionate change in output

In the above figure, we can see marginal cost initially decreases as output increases and later, rises as output increases. Thus, MC curve is also a U-shaped curve

Interested in learning about similar topics?