Unit IV

Overheads

Question bank

Q1) Describe factory functional overhead. (8)

A1) Production/factory overhead

This is also known as manufacturing overhead, work overhead, and factory overhead. All overheads incurred on the factory premises in connection with the production of goods and services are treated as production overheads. Factory rents, fees, lighting, heating, idle wages, factories, buildings, depreciation of factories and machinery, cafeteria costs, etc. are examples of production overhead. Works overheads or manufacturing overheads refer to indirect factory-related costs that are incurred when a product is manufactured. They consist of

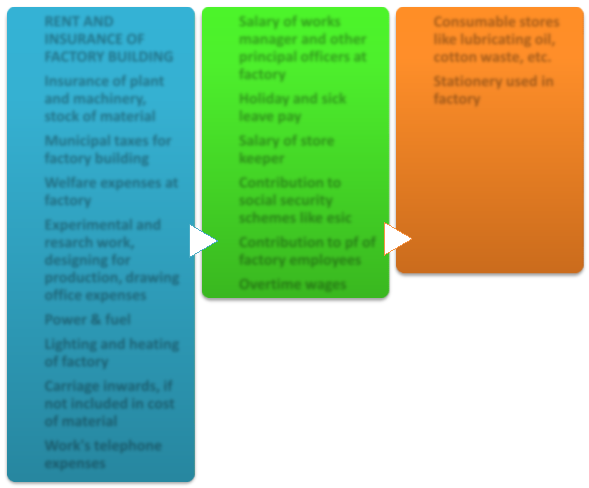

RENT AND INSURANCE OF FACTORY BUILDING

RENT AND INSURANCE OF FACTORY BUILDING

Insurance of plant and machinery, stock of material

Municipal taxes for factory building

Welfare expenses at factory

Experimental and resarch work, designing for production, drawing office expenses

Power & fuel

Lighting and heating of factory

Carriage inwards, if not included in cost of material

Work's telephone expenses

Salary of works manager and other principal officers at factory

Holiday and sick leave pay

Holiday and sick leave pay

Salary of store keeper

Contribution to social security schemes like esic

Contribution to pf of factory employees

Overtime wages

Consumable stores like lubricating oil, cotton waste, etc.

Stationery used in factory

Stationery used in factory

Some factory overheads have been discussed in detail as follows:

1. Depreciation

Depreciation means a decrease in the value of a fixed asset as a result of the use of the fixed asset and / or wear over time. In costing, you need to record depreciation to find the true cost of a manufactured product.

There are several ways to claim depreciation:

--Fixed installment method A method of billing a fixed amount of depreciation expense calculated using the initial cost, scrap price, and expected useful life every year.

--Machine time rate method that estimates the useful life of an asset in hours. The rest is the same as the previous method. Calculate the depreciation amount by dividing the original cost minus the scrap value by the useful life of the asset.

--The depreciation method charges depreciation every year at a fixed rate for depreciation depreciation (that is, depreciation deducted).

Compared to the above method, the depreciation method charges more depreciation in the first year.

--The revaluation method calculates depreciation by comparing the value of an asset at the beginning and end of the year. It is usually used for livestock, loose tools, etc.

--The exchange cost method charges the exchange price of an asset at a fixed rate for depreciation, provides the market value of the asset at the end of its useful life, and takes into account the current production cost.

Note: Even if the asset is in good working order, if the asset's depreciation value no longer exists, it is recommended that you record a reasonable amount of depreciation in your cost account. This expense should be transferred to the costing profit and loss account like any other out-of-pocket profit. Or loss. In addition, if a machine is scrapped before its useful life due to premature obsolescence, the difference between the book value and the realized value at the time of sale is considered an extraordinary loss and will be transferred to the costing income statement.

2. Cost of defective work

Defects are said to be normal if they are unique to the nature of the manufacturing process. For normal defects, the cost of fixing them should be spread across the output. That is, it is included in the manufacturing cost. If the number of defective products exceeds the normal limit or there are abnormal defective products, the correction cost is transferred directly to the profit and loss account of costing.

3. Provisions regarding disobedience

An entity may assume that the commercial life of a plant or machine may be shorter than the estimated useful life used to calculate depreciation. In such cases, this allowance is treated as additional depreciation and is included in the factory overhead. If it's just a precautionary measure, it's a disposal of profits and should be excluded from costing.

4. Machine removal and / or removal costs

Such costs are neither recurring costs nor the usual characteristics of labor. Therefore, these cannot be treated as manufacturing costs.

The cost of installing or constructing a new machine is capitalized and absorbed into production costs through depreciation. In the case of dismantling and re-installing the machine due to a change of location, these costs may be treated as overheads.

If the machine is permanently dismantled before its useful life due to inadequacy or redundancy to accommodate new assets, the difference between the acquisition price and the depreciation amount must be treated as anomalous loss. There is. After deducting the realized amount from the sale of the machine, this loss will be billed in the same year or will be distributed over the useful life of the machine.

If such costs are incurred in cases other than those listed above, the costs should be debited on the costing income statement.

5. Experimental cost

If a company incurs experimental costs for a particular job or order, they should be billed directly for that job or order, and if the same thing happens throughout the organization, it will be overhead for the work should be added.

6. Factory construction rent

If the factory building is owned by the company, financial accounting does not record some amount as rent in the expense account and should include reasonable costs in the overhead costs to facilitate comparison.

7. Idle facility / capacity

First, it is important to understand the difference between idle facilities and idle capacity. The former refers to idle plants, machines, or services, the latter actually or effectively for production purposes due to unavoidable reasons such as lack of demand, availability of resources, or availability. Refers to some of the capacity of an unused plant or equipment. Avoidable false plans.

Idle facilities and installed capacity do not reduce the burden of fixed costs such as rent and insurance. You can handle such costs as follows:

a) If the plant downtime is unavoidable, these costs must be included in the construction overhead and added to the capacity used using supplementary charges.

b) If the facility is not being used for unusual reasons, such as a trade recession, the resulting costs should be included in the costing of the income statement.

c) If the reason is avoided, such costs should be recorded in the costing income statement.

8. Interest in capital

The treatment of interest on capital in costing is a controversial issue.

Claims in favor of including interest in costs:

(a) Interest rate costs are similar to wage costs. Wages are paid for the use of labor and interest is paid for the use of capital. Therefore, both wages and interest must be included in production costs when determining total costs.

(b) If interest is not taken into account, cost comparisons can be misleading. For example, a timber merchant buys standing timber, waits a few years before he can seasonally adjust the timber himself, use or sell it, and then another merchant buys his own already seasoned timber, It may be ready for use or sale. The second merchant pays a much higher amount price. For the purpose of cost comparison, the former merchant needs to add interest on the waiting period.

(c) It is not possible to compare the benefits of different jobs that require different capital or require different completion periods without interest. For example, job 1 is 3 months and Rs. 10,000 capital yield Rs. Job 2 requires Rs, but a profit of 1500. With a capital of 25,000 he will complete in 4 months. Yielding Rs. 2000 profit. If you impose an interest rate of 12%, the profit on your first job will be reduced to Rs. 1200 and Rs. 1250 in the second job. This facilitates a better comparison.

Replacement of existing machines with new ones are not appropriate without due consideration of profits.

(e) The cost comparison of products with substantial value differences is inappropriate without interest, as the amount of capital required for each product varies significantly.

(f) For stocks that fluctuate significantly, it is important to include interest as the amount of capital required to maintain them varies.

(g) When submitting a bid or estimating a price, you must give due consideration to the monetary interest required to undertake the job.

Counterargument to the inclusion of interest in costs:

(a) Interest payments are a matter of internal funding as they are purely dependent on the company's financial policies. The company may work primarily with the owner's capital or have more borrowed capital. The amount of interest varies from case to case and the inclusion of such interest can lead to erroneous results.

(b) It is difficult to determine the amount of capital for which interest is calculated. According to some people, working capital fluctuates, so interest should only be accrued on fixed capital. The process can be very tedious if you need to allocate interest to different departments.

(c) Determining the right interest rate is also difficult and depends on many factors such as risk, maturity, bank interest rates, industry and job nature.

(d) Allowing interest on non-borrowed capital will increase production costs and lead to overvaluation of inventories. However, you can maintain a provision for unrealized profits.

(e) It is not advisable to include interest if the turnover rate is high and the cost of each unit produced is low.

Conclusion: It is theoretically sound to include interest, but given the actual difficulties involved, interest should be excluded from the costing record, even if it was actually paid.

However, capital interests must be taken into account when making business decisions.

9 Research& Development expenses

"Research costs are the cost of finding improved or new products, materials and methods of application. Development costs are the cost of producing new or improved products or adopting new or improved methods. The cost of a process that begins with the implementation of a decision and ends with the formal production of the product or method. ”Defined by CIMA in London.

There are two types of research, basic research or basic research and applied research.

--Basic research is conducted to investigate the possibility of technological development and improve the accumulation of basic knowledge of technological process know-how. The purpose is to improve the knowledge of engineers. The cost of basic research is inherently repetitive. The cost of such basic research is treated as manufacturing overhead.

--Applied research is about the application of basic research knowledge for the introduction or improvement of products, production methods or technologies.

Development costs may be billed as revenue expenditures during the period in which a particular product is incurred. If the costs are high, they can generally be billed as deferred revenue expenditures for a period not exceeding three years. If the product is abandoned at a later stage, the undepreciated balance may be charged to the costing income statement.

10. Pre-manufacturing costs

These costs are incurred when running the prototype before formal production. It usually occurs when a new product line is introduced or when a new factory is in the process of being set up. Such costs expense and charged for future production costs (excluding those capitalized).

Q2) What are the administrative expenses? (5)

A2) Administrative and administrative expenses are detailed as follows:

1. Audit fee

Fees paid to statutory or internal auditors are included in administrative and administrative expenses. Expenses incurred are also recorded as expenses.

The fluctuation range of office costs is much smaller than the fluctuation range of construction costs. After careful consideration of known or expected changes, you can easily make an estimate based on last year's income statement.

2. Financing fee for acquisition of fixed assets

Interest on loans, corporate bonds, etc. paid for the acquisition of fixed assets are called financial fees. These costs are purely financial in nature and can be excluded from costing. The company can also decide to include them as part of the cost. If these costs are incurred to purchase materials for long-term storage such as seasonings, the costs will be recorded as material costs. The assumed interest on the owned capital and the actual interest on the borrowed funds are recorded as administrative and administrative expenses.

3. Nominated salary supervised by the employer

Cost accounts record both actual and assumed costs. Estimated salary is the amount that would be paid to another person if the owner himself did not work for the organization. This estimated salary must be included in administrative and administrative expenses.

Q3) Explain sales and distribution expenses. (7)

A3) Sales and distribution expenses are described in detail as follows:

1. Catalog and price list

The cost of printing the catalog and price list must be transferred to another account and billed equally during the period of use.

2. Bad debt

Credit selling essentially results in some bad debt. Expected bad debt to some extent is included in sales overhead. If the amount is unusual and significantly higher, it should be amortized to the costing P & L account.

3. Regular exhibition fee

Such costs are treated as sales expenses, and if the profits arising from such costs span the period between the two exhibitions, they are treated as deferred revenue expenditures and distributed over the expected lifetime of the profits. Should be done.

4. Market research

The cost of market research conducted on a particular product is included in the cost of that product and is treated as an annual deferred revenue expenditure that is expected to generate that profit. If costs are incurred to investigate market conditions and identify market potential, they should be allocated to different products based on sales.

5. Packing cost

Direct material costs include the cost of containers for which the product cannot be sold. For example, perfumes cannot be sold without bottles. If attractive packaging is in place, they will be treated as advertisements and will therefore be included in sales expenses.

6. Discounts and rebates

Discounts include transaction discounts or cash discounts. In some cases, cash discounts of a purely financial nature are excluded from costing, but trade discounts are deducted from the cost of purchase or sale. Rebates are usually offered for early payments and are therefore included in the cash discount.

7. Subscriptions and donations

Donations usually refer to charities, but subscriptions are usually made to a welfare system or facility. For welfare institutions where employees benefit, subscriptions are treated as overhead costs, while subscriptions or subscriptions to commercial institutions that help find prospects' financial position are treated as sales overheads.

8. Post-sale service costs

These costs must be charged to various products based on the sales achieved.

Q4) What are behavioural cost? (8)

A4) Classification of spending behavior:

This overhead is categorized based on trends that change with production / sales volume or activity level. Some costs change directly to increase or decrease in output, others remain constant as the level of activity of interest changes, others remain constant only up to a certain level, and then. , What fluctuates by changing its properties, which depends on the amount of output, but is not proportional.

Based on this behavior, costs are categorized as follows:

(a) Fixed overhead,

(b)Variable overhead

(c) Semi-variable or semi-fixed overhead.

This classification is not absolute, but for convenience. All costs fluctuate over the long term. This classification is important for cost control and decision making.

(a) Fixed cost:

Fixed overhead costs (also known as term costs and policy costs) are costs incurred over time and tend to be unaffected by fluctuations in activity levels within a certain range. These costs are fixed in total as the output or production activity increases or decreases over a period of time. Fixed overhead per unit decreases as production increases and increases as production decreases.

Examples of fixed costs are building rent, storage space, factory and machine depreciation, building depreciation, space salary and allowance, factory and machine depreciation, building depreciation. , Officers, managers' salaries and allowances, secretaries, accountants, etc., office expenses, stationery and postage, banking fees, litigation costs, work manager salaries, capital interest, costs.

Fixed overhead costs are not always completely fixed in nature.

If concerns increase its capacity, additional equipment and buildings will need to be introduced and more staff will need to be appointed to meet the changed production requirements. As a result, fixed costs are high.

Fixed overhead is constant only within plant capacity limits, and obvious changes in plant capacity affect fixed overhead. The definition that fixed overhead is constant regardless of activity level changes applies only in the short term when there is no apparent change in capacity.

Fixed overhead costs must be incurred during a specific period of time, regardless of changes in production. Therefore, fixed overhead is a period cost that represents a fixed amount of spending during a particular period. In some cases, it is also called the shutdown or standby cost.

Fixed overhead costs are constant in total during the accounting period, but fluctuate per unit as production volume changes. Fixed overhead per unit decreases as production increases as the same amount is distributed to more units. On the other hand, it increases if production capacity remains unused or if production declines due to production inefficiencies.

Fixed overhead costs fall into the uncontrollable cost category from a business management perspective, as there is little room for management action to reduce spending once certain equipment is installed. However, to minimize fixed costs per unit, it is desirable to make the most effective use of plant capacity.

(b) Variable overhead:

This is a cost that tends to follow the level of activity (in the short term). Variable overhead costs fluctuate in total in direct proportion to production. These costs per unit are relatively constant as production changes. In this way, variable costs fluctuate in direct proportion to total production, but tend to remain constant per unit even if production activity changes. Examples include indirect materials, indirect labor, corruption, tools, defective work losses, lubricants, idle time, lighting and heating costs, and sales commissions.

Fluctuating overhead rarely reveals the hallmark of complete volatility: spending that directly changes to fluctuations in production. They tend to change simply, rather than in direct proportion to the output.

In practice, you come across three types of variable overhead:

(i) 100% variable cost. For all productions, variable spending per unit of production is constant.

(ii) The cost per unit of production decreases as the production volume decreases, but gradually increases as the production volume increases.

(iii) The cost per production unit increases as the production volume decreases, but gradually decreases as the production volume increases.

c. Semi-variable costs (also known as mixed or semi-fixed costs) are costs that include both fixed and variable factors and are therefore partially affected by fluctuations in activity levels. These costs are partly fixed and partly variable. For example, telephone charges include a fixed portion of the annual charge and variable charges depending on the call, so the total telephone charges are semi-variable.

Similarly, if a salesperson is eligible to receive a fixed salary and a commission that exceeds a certain amount of sales, the salesperson's compensation is semi-variable overhead, the fixed element is constant at all levels, and the variable element is specified. Works after the level being done. Achieved sales.

There are two types of semi-variable overhead he follows:

(a) The first type shows the semi-variable cost in which the variable elements operate at all levels, as shown in the graph below.

(i) Semi-variable costs:

Variable elements work at all levels.

(b) The second type shows the semi-variable cost in which the variable factor works after a certain level of activity, as shown in the graph above.

(ii) Semi-variable cost:

The variable element works after a certain range.

Step cost:

These costs are progressively increasing costs. These remain constant in various small ranges of output, but the activity increases in discontinuous amounts as he moves from one range to the next. Examples include wages for employees in the employee cafeteria and salaries for supervisors.

Determining cost variability:

Separating semi-variable overhead into fixed and variable overhead is critical to accurate cost confirmation, cost control, and decision making.

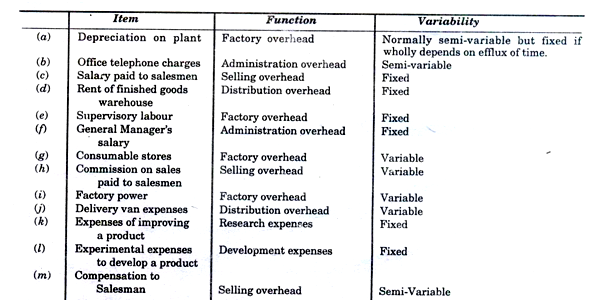

Q5) Classify the following items of expenses by functions and variability (7)

(a) Depreciation on plant;

(b) Office telephone charges;

(c) Salary paid to salesmen;

(d) Rent of finished goods warehouse;

(e) Supervisory labour;

(f) General Manager’s salary;

(g) Consumable stores;

(h) Commission on sales paid to salesmen;

(i) Factory power;

(j) Delivery van expenses;

(k) Expenses of improving a product;

(I) Experimental expenses to develop a product;

(m) Compensation (fixed salary plus commission on sales).

A5)

Q6) What are the reasons for usage of individual charges? (5)

A6) Individual charges are used for four reasons:

1. Fixed costs, which are policy costs, may not be recovered from costs in certain circumstances (such as a recession), but variable costs are fully recovered under normal circumstances.

2. The higher management level responsibility center is for managing fixed costs, while the variable cost overhead center is at the shop level.

3. You may need to adopt different criteria (working hours criteria or direct material cost criteria) to recover indirect costs from costs.

4. Marginal costs can be applied along with profits to establish an important business foundation.

The number of standing order numbers in a factory depends on the size of the factory, the type of cost, and the scope of control required. There are more continuous orders for a wide variety of spending or many types of spending in the factory. For better management, it is desirable to have less expense subdivision.

Q7) What are the requirement for a valid automated money transfer system? (5)

A7) The required requirements for a valid automated money transfer system are:

1. These numbers need to be clearly defined in order to understand the classification and correctly classify each item of cost.

2. There should be no ambiguity as a schedule or manual that requires proper annotation of the permanent order number to help you properly classify each item of expense.

3. The system of standing order numbers must meet the needs of concern. To avoid increasing the cost of clerical work, do not go into too much detail. The classification should not be too broad so that it loses clarity and is useless for administrative purposes.

4. The code should be used for each heading. This is to help you find the item in a convenient way that avoids confusion and ultimately facilitates the collection of overhead.

Q8) What are the causes of over-absorption? (5)

A8) Reasons for overhead over or under absorption

The reasons for over absorption or under absorption of overhead are as follows:

1. Actual working hours are more or less than budget hours.

2. Actual overhead costs are different from budget overhead costs.

3. Both actual overhead costs and actual activity levels differ from budget costs and levels.

4. The overhead absorption method may be incorrect.

5. Unexpected costs may be incurred during the fiscal year end.

6. Overhead costs may be included in the calculation of overhead absorption rates.

7. Major changes, such as changing from manual to mechanical. This leads to increased capacity levels.

8. Seasonal variation of overhead costs over time.

Q9) Explain the concept of under and over absorption of overheads. Also describe the reasons of under and over absorption of overheads.(8)

A9) Overhead is absorbed over a period of accounting or a specific period, depending on the actual production of the product, based on a given overhead absorption rate. Budgeted overhead and budgeted output are used to determine overhead rates. If the budget overhead and budget output differ between the actual overhead and the actual output, then 3 is the difference between the given overhead rate and the actual overhead rate.

If the overhead absorbed is greater than the overhead actually incurred, it is called overabsorption. If the overhead absorbed is less than the actual overhead incurred during the accounting period, it is said to be absorbed.

Reasons for overhead over or under absorption

The reasons for overabsorption or under absorption of overhead are as follows:

1. Actual working hours are more or less than budget hours.

2. Actual overhead costs are different from budget overhead costs.

3. Both actual overhead costs and actual activity levels differ from budget costs and levels.

4. The overhead absorption method may be incorrect.

5. Unexpected costs may be incurred during the fiscal year end.

6. Overhead costs may be included in the calculation of overhead absorption rates.

7. Major changes, such as changing from manual to mechanical. This leads to increased capacity levels.

8. Seasonal variation of overhead costs over time.

Handling of over or under absorption overhead

Overhead or shortage overhead is treated in the cost account in one of the following ways:

1. Application of additional charges

The subsidy rate is calculated by dividing the amount of underabsorption or overabsorption by the actual basis. In the case of overabsorption, the compensation rate is applied to adjust the overrecovery amount and vice versa.

2. Cost of sales adjustment

Over- or under-absorbed overhead costs are closed and transferred to the cost of goods sold account. This is done by the cost accountant at the end of each month or at the end of the accounting period. If a transfer is made at the end of the accounting period, excess / unabsorbed expenses will be treated as deferred income in the case of over-application and deferred expense in the case of under-application and will be carried forward monthly.

3. Amortization to costing profit and loss account

If the overhead or underabsorption overhead is small, it is amortized by transferring it to the costing profit and loss account. If so, the closing inventory valuation is overvalued or undervalued.

4. Adjust to gross profit

Under-absorbed or over-absorbed overhead balances are closed by adjusting gross profit.

5. Carry over to the next year

Over-absorbed or over-absorbed overhead costs can be carried forward to the next fiscal year. It may be transferred to an overhead suspense account or an overhead reserve account. This overhead suspense account or overhead reserve account appears on your balance sheet.

Debit and credit balances that represent absorbed overhead or absorbed overhead that appear on the asset or liability side of the balance sheet. The basic idea is that he offsets the underabsorption overhead in one year and the overabsorbed overhead in another year. However, many accountants disagree with this idea. The reason is that the balance of unabsorbed / overabsorbed overhead must not be carried over from one year to another. This method is also known as the use of reserve accounts.

Q10) What are the advantages and disadvantages of direct labour method?(8)

A10) The advantages of this method are:

(i) Wages paid are usually proportional to working hours, so the time factor is automatically taken into account.

(ii) The labor rate is more stable than the material price.

(iii) Certain variable overhead costs vary to some extent depending on the number of workers employed, so costs for production are related to wage payments proportional to the number of workers.

(iv) The basic data needed to calculate this rate is readily available from the wage statement and there is no additional labor cost.

Disadvantage:

The main drawbacks are:

(i) There is no distinction between skilled and unskilled labor and the difference in wage rates. Jobs carried out by high-paying workers cost more than jobs involving low-paying workers. This is unreasonable because unskilled workers incur more costs in the form of material waste, depreciation, and so on.

(ii) If the worker is paid on a piece-by-piece basis, the time element is completely ignored.

(iii) There is no distinction between the production of manual workers and the production of mechanical workers.

(iv) Overtime pays higher hourly wages, so this method has inaccurate results when workers are paid extra overtime wages. However, overhead costs increase at the same rate. In fact, many costs remain unchanged.

(v) There is no distinction between fixed and variable costs.

(vi) Absorption of overhead costs is unfair if labor is not an important factor in production. Ignore important factors such as widespread use of plants and equipment.

(vii) For pay-as-you-go workers, both efficient and time-consuming workers and inefficient and time-consuming workers apply the same rate to absorb the indirect costs of all workers. , This is not appropriate.

Q11) What is prime cost method? What are its limitations? (7)

A11) Prime cost method:

Under the prime cost method, recovery is calculated by dividing budgeted overhead costs by the sum of direct material costs and direct labor costs for all products in the cost center.

If the budget overhead is Rs 50,000 and the estimated costs of direct materials and labor are Rs 30,000 and Rs 20,000, then the overhead recovery is 100%, or Rs 50,000 / Rs 30,000 + Rs 20,000 x 20,000 x 20,000. Suppose.

This method is simple and easy to operate. The data needed to calculate this rate is easily available from the record. This can be adopted when standard products are produced that require a certain amount of material and the number of hours it takes to manufacture it.

Limitations:

This method is not typically used due to the following limitations:

I. When material cost is the main item of the main cost and the time factor is not fully considered.

Ii. There is no distinction between manual labor and mechanical worker production.

Iii. There is no distinction between fixed and variable costs.

Iv. Combines the shortcomings of both direct materials and direct labor law.

v. In the calculation of overhead costs, both direct materials and direct labor are equally important. Overhead is, of course, more related to labor than material.