UNIT 4

Banking and Financial Market

Introduction

Origin of banking in India

Banking in India is indeed as old as the Himalayas. But the banking functions became an efficient force only after the first decade of 20th century. Banking is an ancient business in India with a number of oldest references in the writings of Manu. Bankers played a crucial role during the Mogul period. During the early a part of East India Company era, agency houses were involved in banking. Modern banking (i.e. in the sort of joint-stock companies) may be said to have had its beginnings in India as far back as in 1786, with the establishment of the general Bank of India.

Structure of banking industry

Banking System

The structure of banking system differs from country to country depending upon their economic conditions, political structure, and economic system. Banks are often classified on the premise of the quantity of operations, business pattern and areas of operations. They're termed as a system of banking.

A bank is a financial organization that provides banking and other financial services to their customers. A bank is usually understood as an establishment which provides fundamental banking services like accepting deposits and providing loans. There also are nonbanking institutions that provide certain banking services without meeting the legal definition of a bank. Banks are a subset of the financial services industry.

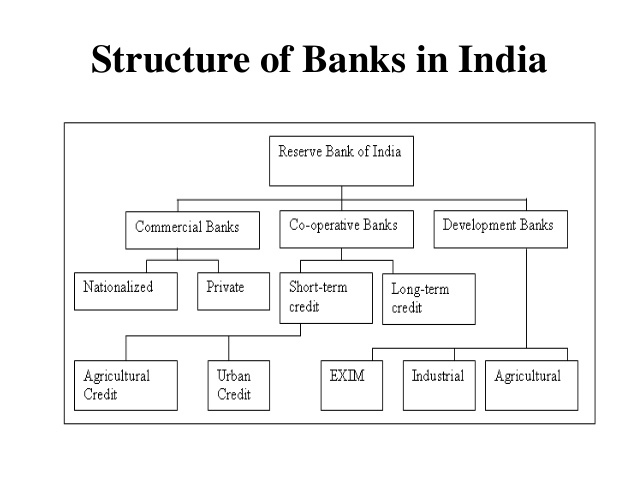

Indian banking system has been divided into two parts, organized and unorganized sectors. The organized sector consists of reserve bank of India, Commercial Banks and Cooperative Banks, and Specialized Financial Institutions (IDBI, ICICI, IFC etc).

1. Reserve banks of India.

2. Indian Scheduled Commercial Banks.

a. State bank of India and its associate banks.

b. Twenty nationalized banks.

c. Regional rural banks.

d. Other scheduled commercial banks.

3. Foreign Banks

4. Non-scheduled banks.

5. Co-operative banks.

Trends in banking

Developments in Commercial Banking in India

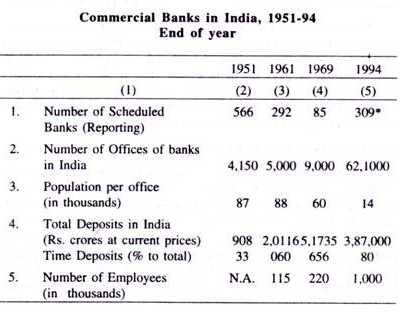

Eight developments in commercial banking after independence (with table) are: 1. Nationalisation of Banks, 2. Regulation of Banks by the RBI, 3. Liquidation and Amalgamation of Banks, 4. Branch Expansion, 5. Lead bank Scheme, The New Strategy of Banking and Area Development, 6. Deposit Growth, 7. Changes within the Composition of Deposits and eight Bank Staff, Productivity and Profits.

Several important developments have taken place in commercial banking, transforming it drastically, after India became a free country 1947. Their quantitative Pleasures since 1951 are summed up in Table below. The importance of those measures is going to be commented upon in appropriate sub-sections in the sequel.

1. Nationalisation of Banks:

The role of the public sector in commercial banking has been greatly enhanced through progressive nationalisation of banks. The primary to be nationalised was the RBI, the country’s central bank, from 1 January 1949. Then came the takeover of the (then) Imperial Bank of India and its conversion into the state bank of India in July 1955, the conversion of eight major state-associated banks into subsidiary tanks of the SBI in 1959, merger of two such banks into one from the start of 1963, thus reducing the amount of the associate banks to seven, nationalisation of 14 other major Indian scheduled banks in July 1969 and of 6 more in April 1980.

The regional rural banks from their inception are being found out in the public sector. As a result, the public-sector banks occupy an edge of dominance in commercial banking in India. Among the public-sector banks, the SBI group of banks is that the largest chain of commercial banks in the country, controlling over a quarter of total bank deposits.

Two main tasks were set before the public-sector banks, namely:

(a) Mobilisation of deposits through a huge programme of branch expansion, especially in unbanked rural and semi-urban areas, and

(b) Diversification of bank credit to ensure flow of monetary assistance to the neglected sectors and sections of the economy in an increasing measure.

2. Regulation of Banks by the RBI:

The RBI has come to play an increasingly important role within the regulation, control, and development of banking altogether its aspects. This has been made possible by the Banking Regulation Act (formerly called the Banking Companies Act), 1949 and its several amendments from time to time. Under the Act, the RBI has been vested with extensive powers of supervision and control over banks.

These powers cover all important aspects of banking from the licensing of banks to their liquidation. The RBI has made good use of those powers and several of the features discussed below are, to an outsized extent, the results of the systematic exercise of those powers.

3. Liquidation and Amalgamation of Banks:

The number of commercial banks has gone down considerably from 566 at the top of 1951 to 271 (including 188 RRBs) at the top of 1990. This is often a result of a deliberate policy of the RBI of systematic removing of substandard non-viable banks through de-licensing and amalgamations and liquidations.

During World War II there had been a mushroom growth of small and ill-managed banks. They were a source of great weakness to the entire banking industry. Their frequent failures were possibly the foremost important reason for the slow spread of banking habits among the public. Therefore, the strengthening of the banking industry required a vigorous implementation of the aforesaid policy.

This has not been an unmixed blessing. Whereas with the removing of the non-viable units, bank failures have now become a thing of the past a great achievement, no doubt the progressive replacement of small banks by large banks has denied the tiny borrower the special attention he used to get more easily from a small local bank.

Moreover, a small local bank wants to enjoy the advantage of adapting its working to the special conditions prevailing within the small area of its operation, which the branch of an enormous national bank managed under an all-India policy doesn't have.

4. Branch Expansion:

The geographical coverage of banking facilities has improved markedly, especially after the nationalisation of 14 major banks in July 1969. Till 1956 the RBI was very cautious in giving licenses for new branches. Its major effort was dedicated to the consolidation and strengthening of the banking industry, and to not expansion.

Consequently till 1954 there was a continual decline in the total number of banking offices, mainly thanks to the amalgamation of smaller banks with larger banks and closure of the offices of non-scheduled and smaller banks.

1956-61 was a period of slow expansion of banking offices, the amount of banking offices increasing from 4,067 to only 5,012. From July 1962 the RBI followed a systematic programme of branch expansion, encouraging banks to open their offices in semi-urban, rural, and other unbanked areas. Under the programme, up to December 1970, the amount of banking offices quite doubled from about 5,000 to about 11,000.

The nationalisation of 14 major banks in July 1969 imparted a new sense of urgency and major impetus to branch expansion in unbanked, especially rural and semi-urban, areas expeditiously. One among the main objectives of bank nationalisation has been this type of expansion of banking facilities in the country. For, the private-sector banks right along had hesitated opening bank offices in small centres, as they didn't expect such offices to be remunerative for several years.

Therefore, it had been thought that the state must come forward in a big way (through the ownership of banks) to open up the countryside to banking and meet the initial costs involved in the interest of larger social goals saving promotion and mobilisation and making available institutional credit and remittance facilities, even in rural areas, for the expansion of agriculture and rural industries. Ever since their nationalisation, the SBI group of banks has played a crucial role in this direction. Since October 1975 the effort has been supplemented by setting up Regional Rural Banks.

Since nationalization of banks, the amount of bank offices has multiplied rapidly from 8,300 in July 1969 to over 62,000 at end June 1995. This has improved substantially the supply of banking facilities in the country. Whereas in 1969 there was just one bank to serve 65,000 population; by the top of 1995, there were five banks for an equivalent number of persons.

The picture becomes far more impressive once we look at the striking increase in the number of bank-offices in rural areas from a mere 1860 in July 1969 to quite 47,000 in June 1995. Taking rural and semi-urban centres together, the amount of bank-offices increased from about 4,200 in July 1969 to quite 47,000 in June 1994, whereas the amount of bank-offices in urban and metropolitan and port towns increased from 3,100 in July 1969 to 8,300 in June 1994.

Also, in recent years, there was greater emphasis on extending banking facilities in deficit districts and in unbanked areas. With the supply of adequate banking infrastructure throughout the country, particularly in rural areas, the RBI has given up its old branch licensing policy and given greater freedom to banks to rationalise their existing branch network in non-rural area.

5. Lead bank Scheme: The New Strategy of Banking and Area Development:

The branch expansion programme of banks in the post- nationalisation phase was alleged to be interwoven with the lead bank Scheme of the RBI, adopted in December 1969. The Scheme was recommended by a Study Group (known because the Gadgil Group) of the National Credit Council. The Group was of the view that due to the diversity of conditions everywhere the country, an area approach was essential for appropriate credit arrangements on the premise of local conditions.

Accordingly, it suggested making major scheduled banks liable for providing integrated and all-round banking facilities under their leadership m all the districts of the country during a well-planned and phased manner. It was hoped that through the instrumentality of credit, these banks would act as catalysts of local development.

Under the Scheme, as adopted, all the 398 districts in the country are distributed among major scheduled banks (in the public sector). They were alleged to play the lead role in the expansion of banking facilities and to act as consortium leaders for coordinating the activities of co-operative, commercial banking and other financial institutions in their respective districts.

Each lead bank is predicted to survey the district, identify unbanked centres, and found out branches in a phased manner. It's also expected to spot and study local problems, evolve an integrated credit plan for the availability of inputs and processing, storage and marketing facilities and other services, which can be locally needed and provide for participation among financing and development agencies operating in the district.

6. Deposit Growth:

Total bank deposits in nominal terms (i.e. at current prices) have grown rapidly after 1961, more so after 1969 (Table 6.1., row 4). What's the growth of bank deposits in real terms due to? what's the relative importance of various factors? How reliable is that the estimated contribution of every factor? The questions are often answered with the assistance of monetary theory and econometric analysis of the data. But we aren't prepared to undertake such a study.

We only note heuristically that the expansion of bank deposits in real terms is thanks to the growth of real income, the spread of banking facilities, the spread of banking habits, strengthening of the banking industry, and the increase in the rate of interest on bank deposits.

7. Changes within the Composition of Deposits:

The relative proportions of demand and time deposits have undergone significant changes (row 4 of Table 6.1). Over the amount covered, the share of time deposits in total deposits has shot up from 33% to 82%. The rise during this ratio has been relatively more spectacular over the last 20 years.

The recorded shift in the composition of deposits is because of several factors, like changes in the composition of bank depositors in favour of households in place of firms, spread of banking facilities in the country, liberalisation of withdrawal conditions in respect of savings deposits, increases within the rates of interest paid on fixed and savings accounts, ban on the payment of interest on current deposits after 1961, and alter in the ‘division of savings deposits between demand and time deposits favouring the latter since 1978.

8. Bank Staff, Productivity and Profits:

With the expansion of banking offices and banking operations, the quantity of bank employees has increased several-fold from 79,000 in 1958 to 10 lakh in 1990. The productivity of their services and the quality of customer service is claimed to have gone down.

This is a real cause for concern for the public also as authorities. It's affected adversely, among other things, the profitability of banks per rupee of their total earnings. The decline during this profitability (in the short-run) also can be attributed partly to rapid branch expansion.

Recent technology trends in banking sector

In recent years, there are many changes in the banking system. These trends in banking have made the entire process of banking very easy. These trends include the following:

1. RTGS – Real Time Gross Settlement

RTGS was introduced in India in March 2004. It's a system through which a bank receives instruction in the sort of electronic for transferring the funds from one bank account to the opposite bank accounts.

As the name suggests, the transfer of funds between the accounts takes place in ‘real time’. The RTGS system is kept running and maintained by the RBI.

So, it's operated by the RBI who provides it the faster and efficient thanks to transfer the funds while facilitating the varied financial operations.

Thus, the cash send under this technique is instantaneous and the beneficiary gets the cash within two hours.

2. E-cheques

This technology has been developed in the US which can replace the conventional paper cheques in India. Thus, to incorporate this method of E-cheque and make it mandatory, a negotiable instruments act has been included within the amendment.

Electronic Clearing Service

ECS is an electronic system that's want to make the payments and receipts that are in bulk. The payments got to be similar in nature which may be smaller in amount and repetitive in nature.

Thus, this facility is specifically beneficial to government agencies and corporations that make or receive large bulk payments.

3. EFT – Electoral Funds Transfer

This is a system to transfer the cash from one’s bank account to other accounts.

So, during this system, the concerning party that desires to make the payment instructs the bank and make cash payment or authorizes the bank to transfer the funds directly.

So, the sender should provide the bank with the entire details just like the name of the receiver, account type, and account number of the respective bank, city name, branch name, and other details to the bank.

Thus, it'll make sure that the amount reaches the beneficiaries account quickly and properly.

4. ATM – cash machine

This is the most popular method in India to withdraw the cash. The customers can enable this service to withdraw the cash 24 by 7.

It allows the customers to perform all day to day bank activities without interacting with any humans. Furthermore, these facilities also are used for the payment of funds, utility bills, etc.

The other trends in the banking sector include some extent of sale terminal, telebanking, and electronic data interchange.

5. Debit Card:

A debit card (also referred to as a bank card or check card) is a plastic card that gives an alternate payment method to cash when making purchases. Functionally, it is often called an electronic cheque, because the funds are withdrawn directly from either the bank account or from the remaining balance on the card. In some cases, the cards are designed exclusively to be used on the internet, so there is no physical card.

The use of debit cards has become widespread in many countries and has overtaken the cheque and in some instances cash transactions by volume. Like credit cards, debit cards are used widely for telephone and Internet purchases, and in contrast to credit cards the funds are transferred from the bearer’s bank account rather than having the bearer to pay back on a later date.

Debit cards can also provide instant withdrawal of money, acting because the ATM card for withdrawing cash and as a cheque guarantee card. Merchants can also offer “cash back”/” cash out” facilities to customers, where a customer can withdraw cash with their purchase

6. Credit Card:

A credit card is an element of a system of payments named after the small plastic card issued to users of the system. It's a card entitling its holder to shop for goods and services supported the holder’s promise to pay for these goods and services.

The issuer of the card grants a line of credit to the buyer (or the user) from which the user can borrow money for payment to a merchant or as an advance to the user. Usage of the term “credit card” to imply a credit card account may be a metonym.

A credit card is different from a charge card, where a credit card requires the balance to be paid fully every month. In contrast, credit cards allow the consumers to ‘revolve’ their balance, at the cost of having interest charged. Most credit cards are issued by local banks or credit unions, and are the form and size specified by the ISO/IEC 7810 standard as ID-1. This is often defined as 85.60 x 53.98 mm in size.

7. Equated Monthly Instalment/Equal Monthly Instalment (EMI):

A fixed payment amount made by a borrower to a lender at a specified date each month

Equated monthly instalments are wont to pay off both interest and principal monthly, in order that over a specified number of years, the loan is paid off fully. With commonest sorts of loans, like land mortgages, the borrower makes fixed periodic payments to the lender over the course of several years with the goal of retiring the loan.

EMIs differ from variable payment plans, during which the borrower is in a position to pay higher payment amounts at his or her discretion. In EMI plans, borrowers are usually only allowed one fixed payment amount every month.

8. Electronic Funds Transfer (EFT):

Electronic Funds Transfer or EFT refers to the computer-based systems wont to perform financial transactions electronically process allowing the lender or the borrower to transfer payments electronically between bank accounts or to a lender.

The term is used for variety of various concepts:

I. Cardholder-initiated transactions, where a cardholder makes use of a payment card

II. Direct deposit payroll payments for a business to its employees, possibly via a payroll services company

III. Direct debit payments from customer to business, where the transaction is initiated by the business with customer permission

IV. Electronic bill payment in online banking, which can be delivered by EFT or paper check Transactions involving stored value of electronic money, possibly during a private currency

V. Wire transfer via an international banking network (generally carries a better fee)

VI. Electronic Benefit Transfer

9. Electronic Clearing Services (ECS):

It is a mode of electronic funds transfer from one bank account to another bank account using the services of a clearing house. This is often normally for bulk transfers from one account to several accounts or vice-versa. This will be used both for creating payments like distribution of dividend, interest, salary, pension, etc. by institutions or for collection of amounts for purposes like payments to utility companies like telephone, electricity, or charges like house tax, water tax, etc or for loan instalments of monetary institutions/banks or regular investments of persons.

There are two sorts of ECS called ECS (Credit) and ECS (Debit).

1. ECS (Credit) is employed for affording credit to an outsized number of beneficiaries by raising one debit to an account, like dividend, interest or salary payment.

2. ECS (Debit) is employed for raising debits to variety of accounts of consumers/ account holders for crediting a specific institution.

10. Point of Sale (POS)

Point of sale (POS), a critical piece of a point of purchase, refers to the place where a customer executes the payment for goods or services and where sales taxes may become payable. It is often during a physical store, where POS terminals and systems are wont to process card payments or a virtual sales point like a computer or mobile device.

11. Doorstep banking

Doorstep banking may be a facility provided to you so that you do not need to visit your bank branch for your routine banking activities like cash deposit, cash withdrawal, cheque deposit or making a demand draft.

Telephone banking may be a service provided by a bank or other financial organization, that permits customers to perform over the telephone a variety of financial transactions which don't involve cash or Financial instruments (such as cheques), without the necessity to visit a bank branch or ATM.

Issues of banking sector

The following points highlight the nine major problems faced by India’s nationalized banks.

1. Losses in Rural Branches:

Most of the rural branches are running at a loss due to high overheads and prevalence of the barter system in most parts of rural India.

2. Large Over-Dues:

The small branches of economic banks are now faced with a new problem—a great deal of overdue advances to farmers. The choice of the former National Front Government to waive all loans to farmers up to the worth of Rs. 10,000 crores have added to the plight of such banks.

3. Non-Performing Assets:

The commercial banks at the present don't have any machinery to ensure that their loans and advances are, in fact, going into productive use in the larger public interest. Thanks to a high proportion of non-performing assets or outstanding thanks to banks from borrowers they're incurring huge losses. Most of them also are unable to keep up capital adequacy ratio.

4. Advance to Priority Sector:

As far as advances to the priority sectors are concerned, the progress has been slow. This is often partly attributable to the very fact that the bank officials from top to bottom couldn't accept nationalization gracefully, viz., and diversion of a particular portion of resources to the top priority and hitherto neglected sectors. This is often also due to the poor and unsatisfactory loan recovery rates from the agricultural and small sectors.

5. Competition from Non-Banking Financial Institution:

As far as deposit mobilization cares, commercial banks are facing stiff challenges from non-banking financial intermediaries like mutual funds, housing finance corporations, leasing and investment companies. Of these institutions compete closely with commercial banks in attracting public deposits and offer higher rates of interest than are paid by commercial banks.

6. Competition with Foreign Banks:

Foreign banks and therefore the smaller private sector banks have registered higher increase in deposits. One reason seems to be that non-nationalized banks offer betters customer service. This creates the impression that a diversion of deposits from the nationalized banks to other banks has probably taken place.

7. Gap between Promise and Performance:

One major weakness of the nationalized banking industry in India is its failure to sustain the specified credit pattern and fill in credit gaps in several sectors. Albeit there has been a reorientation of bank objectives, the bank staff has remained virtually static and therefore the bank procedures and practices have continued to stay old and outmoded.

The post-nationalization period has seen a widening gap between promise and performance. The most reason seems to be the failure of the bank staff to understand the new work philosophy and new social objectives.

“Area approach, agricultural development branches, village adoption plans, etc., are going to be of little avail, if the grass-root level staff isn’t imbued with the motive and therefore the vision of bringing a few silent revolutions in the countryside”.

8. Bureaucratization:

Another problem faced by commercial banks is bureaucratization of the banking industry. This is often indeed the results of nationalization. The graceful functioning of banks has been hampered by red-tapism, long delays, lack of initiative and failure to require quick decisions.

9. Political Pressures:

The smooth working of nationalized banks has also been hampered by growing political pressures from the Centre and therefore the States. Nationalized banks often face many difficulties thanks to various political pressures. Such pressures are created in selection of personnel and grant of loans to particular parties without considering their creditworthiness.

- Cyber threats

- Bank fraud

- Declining profit

- Non- Performing Assets

- Corruption

- Poor service

Challenges in banking sector

- To clean up banks from corruption.

- Eliminate political pressure

- Financial Inclusion

- Improve Efficiency

- Recovery of loans

- Positive Approach

The banking system is undergoing a radical shift, one driven by new competition from Fin Techs, changing business models, mounting regulation and compliance pressures, and disruptive technologies.

The emergence of FinTech/non-bank start-ups is changing the competitive landscape in financial services, forcing traditional institutions to rethink the way they are doing business. As data breaches become prevalent and privacy concerns intensify, regulatory and compliance requirements become more restrictive as a result. And, if all of that wasn’t enough, customer demands are evolving as consumers seek round-the-clock personalized service.

These and other banking system challenges are often resolved by the very technology that’s caused this disruption, but the transition from legacy systems to innovative solutions hasn’t always been a simple one. That said, banks and credit unions got to embrace digital transformation if they want to not only survive but thrive in the current landscape.

1. Increasing Competition

The threat posed by FinTechs, which usually target a number of the most profitable areas in financial services, is critical. Goldman Sachs predicted that these start-ups would account for upwards of $4.7 trillion in annual revenue being diverted from traditional financial services companies.

These new industry entrants are forcing many financial institutions to hunt partnerships and/or acquisition opportunities as a stop-gap measure; actually, Goldman Sachs, themselves, recently made headlines for heavily investing in FinTech. So as to maintain a competitive edge, traditional banks and credit unions must learn from FinTechs, which owe their success to providing a simplified and intuitive customer experience.

2. A Cultural Shift

From artificial intelligence (AI)-enabled wearable’s that monitor the wearer’s health to smart thermostats that enable you to regulate heating settings from internet-connected devices, technology has become ingrained in our culture — and this extends to the banking system.

In the digital world, there’s no room for manual processes and systems. Banks and credit unions got to consider technology-based resolutions to banking system challenges. Therefore, it’s important that financial institutions promote a culture of innovation, within which technology is leveraged to optimize existing processes and procedures for max efficiency. This cultural shift toward a technology-first attitude is reflective of the larger industry-wide acceptance of digital transformation.

3. Regulatory Compliance

Regulatory compliance has become one among the most significant banking system challenges as immediate results of the dramatic increase in regulatory fees relative to earnings and credit losses since the 2008 financial crisis. From Basel’s risk-weighted capital requirements to Dodd-Frank Act, and from the Financial Account Standards Board’s Current Expected Credit Loss (CECL) to the Allowance for Loan and Lease Losses (ALLL), there are a growing number of regulations that banks and credit unions must comply with; compliance can significantly strain resources and is usually dependent on the ability to correlate data from disparate sources.

Faced with severe consequences for non-compliance, banks have incurred additional cost and risk (without a proportional enhancement to risk mitigation) so as to remain up so far on the newest regulatory changes and to implement the controls necessary to satisfy those requirements. Overcoming regulatory compliance challenges requires banks and credit unions to foster a culture of compliance within the organization, also as implement formal compliance structures and systems.

Technology may be a critical component in creating this culture of compliance. Technology that collects and mines data, performs in-depth data analysis, and provides insightful reporting is particularly valuable for identifying and minimizing compliance risk. Additionally, technology can help standardize processes, ensure procedures are followed correctly and consistently, and enables organizations to stay up with new regulatory/industry policy changes.

4. Changing Business Models

The cost related to compliance management is simply one of many banking system challenges forcing financial institutions to vary the way they are doing business. The increasing cost of capital combined with sustained low interest rates, decreasing return on equity, and decreased proprietary trading are all putting pressure on traditional sources of banking profitability. Because of, shareholder expectations remain unchanged.

This culmination of factors has led many institutions to form new competitive service offerings, rationalize business lines, and seek sustainable improvements in operational efficiencies to take care of profitability. Failure to adapt to changing demands isn't an option; therefore, financial institutions must be structured for agility and be prepared to pivot when necessary.

5. Rising Expectations

Today’s consumer is smarter, savvier, and more informed than ever before and expects a high degree of personalization and convenience out of their banking experience. Changing customer demographics play a serious role in these heightened expectations: With each new generation of banking customer comes a more innate understanding of technology and, as a result, an increased expectation of digitized experiences.

Millennial have led the charge to digitization, with five out of six reporting that they like to interact with brands via social media; when surveyed, millennial were also found to form up the largest percentage of mobile banking users, at 47%. Supported this trend, banks can expect future generations, starting with Gen Z, to be even more invested in Omni channel banking and attuned to technology. By comparison, Baby Boomers and older members of generation X typically value human interaction and like to go to physical branch locations.

This presents banks and credit unions with a unique challenge: How can they satisfy older generations and younger generations of banking customers at an equivalent time? The solution is a hybrid banking model that integrates digital experiences into traditional bank branches. Imagine, if you’ll, a physical branch with a self-service station that displays the foremost cutting-edge smart devices, which customers can use to access their bank’s knowledge base. Should a customer require additional assistance, they will use one among these devices to schedule an appointment with one among the branch’s financial advisors; during the appointment, the advisor will answer any of the customer’s questions, also as set them up with a mobile AI assistant which will provide them with additional recommendations based on their behaviour. It'd sound too good to be true, but the branch of the future already exists, and it’s helping banks and credit unions meet and exceed rising customer expectations.

Investor expectations must be accounted for, as well. Annual profits are a serious concern — after all, stakeholders got to know that they’ll receive a return on their investment or equity and, so as for that to happen, banks ought to actually turn a profit. These ties back to customer expectations because, in an increasingly constituent-centric world, satisfied customers are the key to sustained business success — so, the happier your customers are, and the happier your investors are going to be.

6. Customer Retention

Financial services customers expect personalized and meaningful experiences through simple and intuitive interfaces on any device, anywhere, and at any time. Although customer experience is often hard to quantify, customer turnover is tangible and customer loyalty is quickly becoming an endangered concept. Customer loyalty may be a product of rich client relationships that begin with knowing the customer and their expectations, also as implementing an ongoing client-centric approach.

In an Accenture Financial Services global study of nearly 33,000 banking customers spanning 18 markets, 49% of respondents indicated that customer service drives loyalty. By knowing the customer and engaging with them accordingly, financial institutions can optimize interactions that lead to increased customer satisfaction and wallet share, and a subsequent decrease in customer churn.

Bots are one new tool financial organizations can use to deliver superior customer service. Bots are a helpful thanks to increase customer engagement without incurring additional costs, and studies show that the bulk of consumers prefer virtual assistance for timely issue resolution. Because the first line of customer interaction, bots can engage customers naturally, conversationally, and contextually, thereby improving resolution time and customer satisfaction. Using sentiment analysis, bots also are ready to gather information through dialogue, while understanding context through the recognition of emotional cues. With this information, they will quickly evaluate, escalate, and route complex issues to humans for resolution.

7. Outdated Mobile Experiences

These days, every bank or credit union has its own branded mobile application — however; simply because a corporation has a mobile banking strategy doesn’t mean that it’s being leveraged as effectively as possible. A bank’s mobile experience must be fast, easy to use, fully featured (think live chat, voice-enabled digital assistance, and therefore the like), secure, and frequently updated in order to stay customers satisfied. Some banks have even started to reimagine what a banking app might be by introducing mobile payment functionality that permits customers to treat their smart phones like secure digital wallets and instantly transfer money to family and friends.

8. Security Breaches

With a series of high-profile breaches over the past few years, security is one among the leading banking system challenges, also as a serious concern for bank and credit union customers. Financial institutions must invest in the latest technology-driven security measures to stay sensitive customer safe, such as:

- Address Verification Service (AVS)

AVS “checks the billing address submitted by the card user with the cardholder’s billing address on record at the issuing bank” so as to identify suspicious transactions and stop fraudulent activity.

2. End-to-End Encryption (E2EE)

E2EE “is a way of secure communication that stops third-parties from accessing data while it’s transferred from one end system or device to another.” E2EE uses cryptographic keys, which are stored at each endpoint, to encrypt and decrypt private messages.

Banks and credit unions can use E2EE to secure mobile transactions and other online payments, in order that funds are securely transferred from one account to a different or from a customer to a retailer.

3. Authentication

• Biometric authentication “is a security process that relies on the unique biological characteristics of a private to verify that he's who he says he’s. Biometric identification systems compare a biometric data capture to stored, confirmed authentic data in a database.” Common sorts of biometric identification include voice and face recognition and iris and fingerprint scans. Banks and credit unions can use biometric identification in place of PINs, as it’s harder to duplicate and, therefore, safer.

• Location-based authentication (sometimes stated as geolocation identification) “is a special procedure to prove an individual’s identity and authenticity on appearance just by detecting its presence at a definite location.” Banks can use location-based authentication in conjunction with mobile banking to stop fraud by either sending out a push notification to a customer’s mobile device authorizing a transaction, or by triangulating the customer’s location to work out whether they’re in the same location during which the transaction is happening.

• Out-of-band authentication (OOBA) refers to “a process where authentication requires two different signals from two different networks or channels… [By] using two different channels, authentication systems can guard against fraudulent users which will only have access to at least one of those channels.” Banks can use OOBA to get a one-time security code, which the customer receives via automated voice call, SMS text message, or email; the customer then enters that security code to access their account, thereby verifying their identity.

• Risk-based authentication (RBA) — also referred to as adaptive authentication or step-up authentication — “is a way of applying varying levels of stringency to authentication processes supported the likelihood that access to a given system could end in its being compromised.” RBA enables banks and credit unions to tailor their security measures to the risk level of every customer transaction.

9. Antiquated Applications

According to the 2017 Gartner CIO Survey, over 50% of monetary services CIOs believe that a greater portion of business will come through digital channels and digital initiatives will generate more revenue and value.

However, organizations using antiquated business management applications or soloed systems are going to be unable to stay up with this increasingly digital-first world. Without a solid, forward-thinking technological foundation, organizations will miss out on critical business evolution. In other words, digital transformation isn't just an honest idea — it’s become imperative for survival.

While technologies like block chain should be too immature to understand significant returns from their implementation within the near future, technologies like cloud computing, AI, and bots all offer significant advantages for institutions looking to scale back costs while improving customer satisfaction and growing wallet share.

Cloud computing via software as a service and platform as a service solution enable firms previously burdened with disparate legacy systems to simplify and standardize IT estates. In doing so, banks and credit unions are ready to reduce costs and improve data analytics, all while leveraging forefront technologies. AI offers a major competitive advantage by providing deep insights into customer behaviours and wishes, giving financial institutions the power to sell the right product at the right time to the right customer. Additionally, AI can provide key organizational insights required to spot operational opportunities and maintain agility.

10. Continuous Innovation

Sustainable success in business requires insight, agility, rich client relationships, and continuous innovation. Benchmarking effective practices throughout the industry can provide valuable insight, helping banks and credit unions stay competitive. However, benchmarking alone only enables institutions to stay up with the pack — it rarely results in innovation. Because the cliché goes, businesses must benchmark to survive, but innovate to thrive; innovation is a key differentiator that separates the wheat from the chaff.

Innovation stems from insights, and insights are discovered through customer interactions and continuous organizational analysis. Insights without action, however, are impotent — it’s vital that financial institutions be prepared to pivot when necessary to handle market demands while improving upon the customer experience.

Financial service organizations leveraging the newest business technology, particularly around cloud applications, have a key advantage in the digital transformation race: they will innovate faster. The ability of cloud technology is its agility and scalability. Without system hardware limiting flexibility, cloud technology enables systems to evolve alongside your business.

How Hitachi Solutions Can Help

With numerous banking system challenges to deal with, charting a clear path forward can appear to be an overwhelming task — but with the proper team to support your efforts, digital transformation is attainable. The financial services team at Hitachi Solutions has been helping banks and credit unions unlock digital experiences through the facility of the Microsoft platform since 2004. With a large type of products and services tailored to the financial services industry, like Engage for Banking and Retail Banking Sales Insights, we’re conversant in the unique issues financial institutions face and have developed the technology to resolve them.

From data science expertise to business intelligence, AI and beyond, Hitachi Solutions is here to assist your organization tackle banking system challenges and embrace digital transformation.

Insurance sector

Introduction

The insurance industry of India consists of 57 insurance companies of which 24 are in life assurance business and 33 are non-life insurers. Among the life insurers, life assurance Corporation (LIC) is that the sole public sector company. Aside from that, among the non-life insurers there are six public sector insurers. Additionally, to those, there's sole national re-insurer, namely, General Insurance Corporation of India (GIC Re). Other stakeholders in Indian Insurance market include agents (individual and corporate), brokers, surveyors and third-party administrators servicing insurance claims.

HISTORY OF INSURANCE IN INDIA are often BROADLY BIFURCATED INTO THREE ERAS:

Insurance features a long history in India. The business of life assurance started in India within the year 1818 with the establishment of the Oriental life assurance Company in Calcutta.

(a) Pre-Nationalisation

(b) Nationalisation and

(c) Post Nationalisation.

INSURANCE SECTOR

Life Insurance was the first to be nationalized in 1956. General Insurance followed suit and was nationalized in 1973.

After the report submitted by Malhotra Committee in 1994, Insurance Regulatory Development Act was passed in 1999 which gave an entry to private insurance companies the goals of the IRDA are to safeguard the interests of insurance policyholders, also on initiate different policy measures to assist sustain growth in the Indian insurance sector.

The life insurance sector transformed since it had been thrown open to private sector participation in 2000. Life insurance Corporation of India (LIC) was formed in September, 1956 by an Act of Parliament, with capital contribution from the govt of India. Even today, life insurance Corporation of India dominates Indian insurance sector.

The introduction of personal players in the industry has added value to the insurance industry. The initiatives taken by the private players were very competitive and have given immense competition to the on-time monopoly of the market LIC. Since the arrival of the private players in the insurance market it has seen new and innovative steps by the players in this sector. The new players have improved the service quality of the insurance.

Recent trends in insurance industry

Investments and recent Developments

The following are a number of the major investments and developments in the Indian insurance sector.

• The non-life insurance companies witnessed an increase of 14 per cent in their collective premium for April-February 2019-20.

• In November 2019, Airtel partnered with Bharti AXA Life to launch prepaid bundle with insurance cover.

• In September 2019, Competition Commission of India (CCI) approved acquisition of shares in SBI General Insurance by Nepean Opportunities LLP and Honey Wheat.

• As of November 2018, HDFC Ergo is in advanced talks to accumulate Apollo Munich insurance at a valuation of around Rs 2,600 crore (US$ 370.05 million).

• In October 2018, Indian e-commerce major Flipkart entered the insurance space in partnership with Bajaj Allianz to supply mobile insurance.

• In August 2018, a consortium of WestBridge Capital, billionaire investor MrRakeshJhunjunwala announced that it might acquire India’s largest health insurer Star Health and Allied Insurance during a deal estimated at around US$ 1 billion.

• India's leading bourse Bombay stock exchange (BSE) will found out a venture with EbixInc to build a strong insurance distribution network in the country through a replacement distribution exchange platform.

GOVERNMENT INITIATIVES

The Government of India has taken variety of initiatives to boost the insurance industry. a number of them are as follows:

• As per Union Budget 2019-20, 100 per cent foreign direct investment (FDI) permitted for insurance intermediaries.

• In September 2018, National Health Protection Scheme was launched under Ayushman Bharat to supply coverage of up to Rs 500,000 (US$ 7,723) to quite 100 million vulnerable families. The scheme is predicted to increase penetration of insurance in India from 34 per cent to 50 per cent.

• Over 47.9 million famers were benefitted under PradhanMantriFasalBimaYojana (PMFBY) in 2017-18.

• The Insurance Regulatory and Development Authority of India (IRDAI) plans to issue redesigned initial public offering (IPO) guidelines for insurance companies in India, which are to looking to divest equity through the IPO route.

• IRDAI has allowed insurers to invest up to 10 per cent in additional tier 1 (AT1) bonds that are issued by banks to reinforce their tier 1 capital, so as to expand the pool of eligible investors for the banks.

Importance of insurance industry

The following point shows the role and importance of insurance:

Insurance has evolved as a process of safeguarding the interest of people from loss and uncertainty. It’s going to be described as a social device to scale back or eliminate risk of loss to life and property.

Insurance contributes plenty to the general economic growth of the society by provides stability to the functioning of process. The insurance industries develop financial institutions and reduce uncertainties by improving financial resources.

1. Provide safety and security:

Insurance provide financial support and reduce uncertainties in business and human life. It provides safety and security against particular event. There's always a fear of sudden loss. Insurance provides a cover against any sudden loss. For example, in case of life assurance financial assistance is provided to the family of the insured on his death. Just in case of other insurance security is provided against the loss because of fire, marine, accidents etc.

2. Generates financial resources:

Insurance generate funds by collecting premium. These funds are invested in government securities and stock. These funds are gainfully employed in industrial development of a country for generating more funds and utilised for the economic development of the country. Employment opportunities are increased by big investments resulting in capital formation.

3. Life insurance encourages savings:

Insurance doesn't only protect against risks and uncertainties, but also provides an investment channel too. Life insurance enables systematic savings because of payment of regular premium. Life insurance provides a mode of investment. It develops a habit of saving money by paying premium. The insured get the lump sum amount at the maturity of the contract. Thus life assurance encourages savings.

4. Promotes economic growth:

Insurance generates significant impact on the economy by mobilizing domestic savings. Insurance turn accumulated capital into productive investments. Insurance enables to mitigate loss, financial stability and promotes trade and commerce activities those results into economic process and development. Thus, insurance plays an important role in sustainable growth of an economy.

5. Medical support:

A medical insurance considered essential in managing risk in health. Anyone is often a victim of critical illness unexpectedly. And rising medical expense is of great concern. Medical Insurance is one of the insurance policies that cater for various sorts of health risks. The insured gets a medical support just in case of medical policy.

6. Spreading of risk:

Insurance facilitates spreading of risk from the insured to the insurer. The fundamental principle of insurance is to spread risk among a large number of people. a large number of persons get insurance policies and pay premium to the insurer. Whenever a loss occurs, it's compensated out of funds of the insurer.

7. Source of collecting funds:

Large funds are collected by the way of premium. These funds are utilised in the industrial development of a country, which accelerates the economic process. Employment opportunities are increased by such big investments. Thus, insurance has become a vital source of capital formation.

Issues in insurance industry

1. Digitizing small commercial

Because of small commercial insurance is aarge and profitable market for those who know it, it’s now attracting a good deal of attention and under pressure to modernize. As a result, carriers are finally making significant investments in the digital space.

2. Improving the customer experience with data analytics

Insurers' increasing access to customer data, analytical tools and marketing technology is enabling outreach to customers and a transparent line of sight into what resonates with them. Carriers are increasingly ready to quantify the pain points that cause a customer to leave—a true moment of truth—and use this data to enhance the customer experience.

3. Driving change with InsurTech

Reflecting a growing maturity linking technology and strategy, new and existing players are increasingly that specialize in distribution channels and the way carriers interact with policyholders and employees in order to make a beautiful, brand differentiating experience.

4. Getting value from the digital journey

Whether you’re embarking on a digital transformation or simply making targeted improvements, there are a couple of important things to stay in mind to urge value from the digital journey.

5. Insights from experience design

As carriers try new ways of doing business, one among the biggest developments at the company level is experience design owning a seat at the table, due to its vital role in the customer experience and brand architecture.

6. Model risk management 2.0

MRM 2.0 is evolving as a result of revisiting the definition of “model,” a shift to validating new models, rationalizing the three lines of defence and seeking cost efficiencies.

7. LDTI and IFRS 17 implementation synergies

Because both FASB LDTI and the IASB IFRS 17 approaches address similar considerations, companies that require to dual-adopt are finding opportunities for synergies as they refine their approach to implementation. They’ll be ready to align policy decisions while simultaneously adopting both standards without needing to worry about two full implementation plans.

8. Impacts of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act’s provisions have had impacts on insurers' operations and business decisions that go far beyond tax. We highlight the Act's most salient effects on insurers, also as provide perspective on extensive IRS and treasury department guidance under the Act.

Challenges of insurance industry

Insurance firms are summarily viewed as establishments meant to cancel or minimize the adverse consequences of unforeseen misfortunes. Indeed, insurance companies are risk outcomes underwriters. Because we leave in very unpredictable societies that have an extensive sort of risk trajectories, it's commonly expected that a person at a specific point in time will run into unfriendly situations which will endanger his or her life and property no matter status, calibre, education level, and class. Industrialized and matured societies depend upon insurance. This is often evidencing why many companies and industries in developed nations don't liquidate or “go under “in such societies.

Ordinarily, against this contextual, most people expect that insurance firms are going to be viable and popular in societies. However, this is often not the case since many insurance businesses face difficult challenges that seriously threaten their survivals and existences. This is often common in less developed societies where political and socio-economic systems are yet to crystallize. Social, economic, and political systems in such countries present terrible problems to insurance companies. Many of the societies with dangerous conditions to insurance sector are Africa, Asia, Caribbean, and the Latin America.

For sure, if an individual has just started the business of selling insurance, then he or she must understand that having thick skin is a crucial thing for him or her to survive in the industry. Today, each business changes in some ways and therefore the changes can either be negative or positive. In any industry, there are various problems to be faced. Here are the most important challenges for insurance companies.

1. Lack of trust

This is a reason why many individuals dont bother with insurance. Many insurance firms fail to pay claims, and that they dont own up to offering some benefits. Therefore, most of the people just see insurance together of the unnecessary expenses. Many insurance firms do shut down due to financial challenges and individuals who are the victims of the loss dont even think twice about purchasing insurance policies.

2. Competition

Today, there are many insurance firms on the market and therefore there's an intensive challenge for insurers. Each company looks for the simplest way of selling their insurance products in the best possible way and targets a specific group of people. Most insurance businesses, especially the new ones are the foremost doubted companies. In fact, most of the people trust a number of the existing insurance firms compared to the new businesses since the new enterprises are operated on a thin line between failure and success—and nobody will want to require such risks with the little among of cash that they have.

3. Mismanagement

As the owner of the insurance business, one is solely liable for all issues that his or her clients may have regarding the management of the insurance business. All insurance firms that are mismanaged cant hide their faults for a extended time without the clients noticing. As time move, there'll be a constant increase in the number of clients complaints, and if his or her insurance company isn't transparent, then he or she will lose more customers. Also, incompetent management may cost the company tons, particularly if they have poor communication with their clients.

In case an individuals premiums are high, he or she shouldn't advertise. They should search for a market for that policy instead of lying to the overall public or maybe form strategies whereby the clients cut on expenses like providing no-exam life insurance quotes.

4. Economic instability

When the countrys economy is down, all insurance companies are going to be affected. At such situations, the rates are often affected such the insurance companies might be forced to increase their rates, just like interest rates on credit facilities provided by financial institutions.

Of course, no client will appreciate this, even if it's stated clearly in the contract that the insurance rates might change from time to time. Therefore, such situations might create a bad image for a company since costumers can spread the information about a service or product, they weren't happy with very fast.

5. Weak manpower

Non-professionals run many of the insurance companies today. In fact, many of us think that what it takes to be an insurance professional is just some knowledge of Monetary studies with no specialized training. Indeed, this has majorly affected the dependability and operations of insurance firms in this century.

6. Excessive politicization of the insurance industry

Without a doubt, politics play a major role in insurance companies operations depending on the facility play & calculations that are dominant in the operating domains of the insurance firms. The premiums to pay, the outcomes of risk investigations, and therefore the damages and benefits to pay depend upon political conspiracy sometimes.

These are some of the biggest challenges that are faced by insurance companies. They include mismanagement, economic instability, lack of trust, and competition among others.

Key takeaways

- A bank is a financial organization that provides banking and other financial services to their customers.

- Indian banking system has been divided into two parts, organized and unorganized sectors.

- The insurance industry of India consists of 57 insurance companies of which 24 are in life assurance business and 33 are non-life insurers.

- SBI group of banks is that the largest chain of commercial banks in the country, controlling over a quarter of total bank deposits.

Introduction

In an economy, there are various sorts of market. One such form is that the financial market, an area where financial assets are created and exchanged. This financial market has two major classifications – capital market and market. Let us educate ourselves about the functioning of the money markets.

The money market may be a sub-section of the financial market that trades in short term financial funds and financial assets. These instruments and assets usually have a maturity period of but one year and are highly liquid. Therefore, the buying and selling of such instruments, like commercial papers and T-bills, occurs in the money market.

This market isn't a physical location. Most of the trading happens over the phone and now over the web. It’s a virtual marketplace for trading in low-risk, liquid, and unsecured instruments to meet short-term financial needs a company may have. Companies turn to monetary market mostly to satisfy their working capital requirements.

MONEY MARKETS

The major players and institutions of this market are the reserve bank of India, all the commercial banks of the country, NBFC’s, LIC, Mutual Funds, large corporate, and even the respective state governments. Let us look at other features of this market.

• Unlike the stock exchange, the money market doesn't have geographical restrictions. Most transactions happen in the virtual world with institutions which will be spread out over the entire country, the entire world even.

• While the market is quite flexible and unrestricted, it only deals in short-term securities (maturity period between at some point and 364 days)

• There is not any need for brokers or other intermediaries. The transactions can happen without them.

• There are many securities in the money market like T-bills, commercial bills, call money etc

Structure of Indian money markets

The Indian monetary market has two broad categories – the organized sector and the unorganized sector.

Organized Sector: This sector comprises of the governments, the RBI, the opposite commercial banks, rural banks, and even foreign banks. The RBI organizes and controls this sector. Other corporations just like the LIC, UTI, etc also participate during this sector but indirectly. Other large companies and corporate also participate during this sector through banks.

Unorganized Sector: These are the indigenous banks and therefore the local money lenders and hundis etc. Their activities aren't controlled by the RBI or the other body, so they are the unorganized sector.

Objectives of money market

The main objectives of the monetary market are as follows,

• The main objective is to supply borrowers with short-term funds at reasonable rates. And since the securities are all short-term the lenders also will have the benefit of liquidity.

• Turns savings and idle funds of the public into effective investments. This is often beneficial for the entire economy

• Allows the reserve bank of India to regulate the amount of liquidity in the economy. This is often one of the most functions of the RBI.

• Companies and corporations have short-term deficits from time to time. They'll also need help with their capital requirements. The money market will facilitate the funds necessary.

• Helps the govt implement monetary policies via their open market operations which are direct and effective in nature.

Limitations of market structure

Indian money market is considered underdeveloped market. The major shortcomings of Indian market are as follows:

1. Absence of Coordination:

There is no coordination between organised and unorganized sectors of the money market. Sometimes there's even wasteful competition between them.

Such a situation is extremely harmful for the economic progress of the country.

2. Absence of Developed Bill Market:

An important shortcoming of Indian money market is that the absence of a well-developed money market. Though both inland and foreign bills are traded in Indian market yet its scope is extremely limited. In spite of the efforts of reserve bank in 1952 and in 1970, only a limited bill market exists in India. Thus, an organised bill market within the real sense of the term has not yet been fully developed in India. The most obstacles in the development of bill market appear to be the following:

(i) The lack of uniformity in drawing bills in several parts of the country,

(ii) The massive use of money credit as the main sort of borrowing from commercial banks,

(iii) Presence of Inter-call market and

(iv) The pressure of cash transactions. Thus, Bill Market is comparatively underdeveloped.

3. Shortage of Funds in Money Market:

The Indian money market is characterised by shortage of funds. The funds available in the market are inadequate to satisfy the wants of trade and industry. The most reasons liable for shortage of funds are poverty, low level of income and low savings. Inadequate banking facilities also are one of the main causes of shortage of funds.

4. Seasonal Stringency of Funds:

Another defect of Indian money market is the stringency of credit in particular seasons of the year. During the harvest (April to November) there's substantial rise in demand for credit. The availability of credit at such a time doesn't increase in the same proportion in which demand increases.

Consequently, rate of interest shoots up in the busy season and on the opposite hand, during the slack season, thanks to fall in demand for credit, the rate of interest declines. These wide variations within the supply and demand for money are because of inelastic supply of money.

5. Lack of Uniformity in Interest Rates:

In Indian money market, there's no uniformity in rates of interest. The lending rates of commercial banks differ from those of The Rural Regional Banks and cooperative banks. There’s also wide variation in the rates of interest charged by the banks of organised sector and of indigenous banks. The bill finance rate also differs from hundi rate.

6. Underdeveloped Banking Habits:

Inspire of rapid branches expansion of banks and spread of banking to unbanked and rural centres, the banking habits in India are still underdeveloped, (i) There are several reasons for it.

Whereas in U.S.A. For every 1400 persons there's a branch of a commercial bank, in India there's a branch for each 13,000 people, (ii) the utilization of cheques is restricted; (iii) the majority of transactions are settled in cash, (iv) The hoarding habit is widespread.

7. Dominance of Indigenous Bankers:

The indigenous banker still dominates the banking scene in India. Even after banking expansion within the rural areas, the cash lenders still continue to be the sole source to the agriculturists. They exploit their customers by adopting malpractices and charging exorbitant rate of interest the reserve bank exercises no control over them.

Reforms in market structure

Reserve Bank of India is that the biggest regulator of the Indian markets. It controls the monetary policy of India. Its control is however limited to the organised a part of economy and the unorganised sector which features a significant presence is essentially unregulated. RBI frequently introduces many reforms to bolster the Indian economy which is during a state of constant flux and is continuously evolving. The major money market reforms came after the recommendations of S. Chakravarty Committee and Narsimha Committee. These were major changes which helped unfold the banking potential of India and shape our financial institutions to world class standards. It had been soundness of those reforms which helped our economy to easily bridge over the economic crisis which had gripped the world in 2008. These are discussed below:

1. Deregulation of Interest Rates

Interest rates are now subject to plug conditions as the ceiling limit on them are removed by RBI after 1989.The important interest rates in India are-Bank rate, Medium-term lending rate, Prime Lending rate, bank deposit rate, Call rate, Certificate of Deposit rate, commercial paper rate etc. This deregulation got a significant push after the economic liberalisation of 1991. Chakravarty Committee was a robust proponent of free and versatile interest rates to market savings, investments, government financial system and stability. RBI removed the upper ceiling of 16.5% and instead fixed a minimum of 16% per annum. The rates were further relaxed after the Narasimhan Committee report in 1991.

2. Reforms in Call and Term money market

The reforms in call and term money market were done to infuse more liquidity into the system and enable price discovery. RBI undertook several important steps to see the constraints and remove them systematically. It was in October 1998, RBI announced that non-banking financial institutions shouldn't participate in call/term money market operations and it should purely be an interbank operating segment and encouraged other participants to migrate to collateralised segments to boost stability. Also, reporting of all call/notice money market transactions through negotiated dealing system within 15 minutes of conclusion of transaction was made mandatory. The volume of operations in this segment wasn't increased much even after the reforms.

3. Introduction of new money market instruments

RBI introduced many new market instruments to diversify the market. These were certificates of deposit in 1989, commercial papers in 1990 and interbank participation certificates with/without risk in 1988.

4. Fixing Discount and Finance House of India

Discount and Finance House of India was found out in 1988 to impart more liquidity and also further develop the secondary market instruments. However, maturities of existing instruments like CDs and CPs were gradually shortened to encourage wider participation. Likewise, ad hoc treasury bills were abolished in 1997 to prevent automatic monetisation of fiscal deficit.

5. Introducing Liquidity Adjustment Facility

RBI introduced a Liquidity Adjustment Facility in June 2000 which was operated through fixed repo and reverse repo rates. This helped establishment of rate of interest as a crucial monetary instrument and granted greater flexibility to RBI to reply to market needs and suitably adjust liquidity in the market. Repo and Reverse Repo rates were introduced in 1992 and 1996 respectively.

6. Refinance by RBI

This is a potent tool by RBI to satisfy the any liquidity shortages and for credit control to select sectors. The export credit refinance facility to banks is provided under Section 17(3) of RBI Act 1934. It's available to all or any scheduled commercial banks who are authorised to deal in foreign exchange and have extended credit. The SCBs are provided export credit to the tune of 50 of the outstanding export credits. The concept of directed credit was also changed because the Narasimhan Committee recommended reduction of directed credit from 40 to 10%. It also suggested narrowing of priority sector and realigning focus to small farmers and low-income target groups. The refinance rate is linked to bank rate.

7. Regulation of Non-Banking Financial Companies

RBI Act was amended in 1997 to bring the NBFCs under its regulatory framework. A NBFC is a company registered under Companies Act, 1956 and is involved in making loans and advances, acquisition of shares, stocks, bonds, securities issued by government etc. they're almost like banks but are different from the latter as they can't accept demand deposits and can't issue cheques. They need to be registered with RBI to work within India. There are a number of regulations which NBFCs need to follow to smoothly operate within India like accept deposit for a minimum period, cannot accept rate of interest beyond the prescribed rate given by RBI.

8. Debt Recovery

RBI has set up special Recovery Tribunals which provide legal assistance to banks for recovery of dues.

Key takeaways-

- The money market may be a sub-section of the financial market that trades in short term financial funds and financial assets.

- The major players and institutions of this market are the reserve bank of India, all the commercial banks of the country, NBFC’s, LIC, Mutual Funds, large corporate, and even the respective state governments.

- Reserve Bank of India is that the biggest regulator of the Indian markets. It controls the monetary policy of India.

NEWS

INTRODUCTION

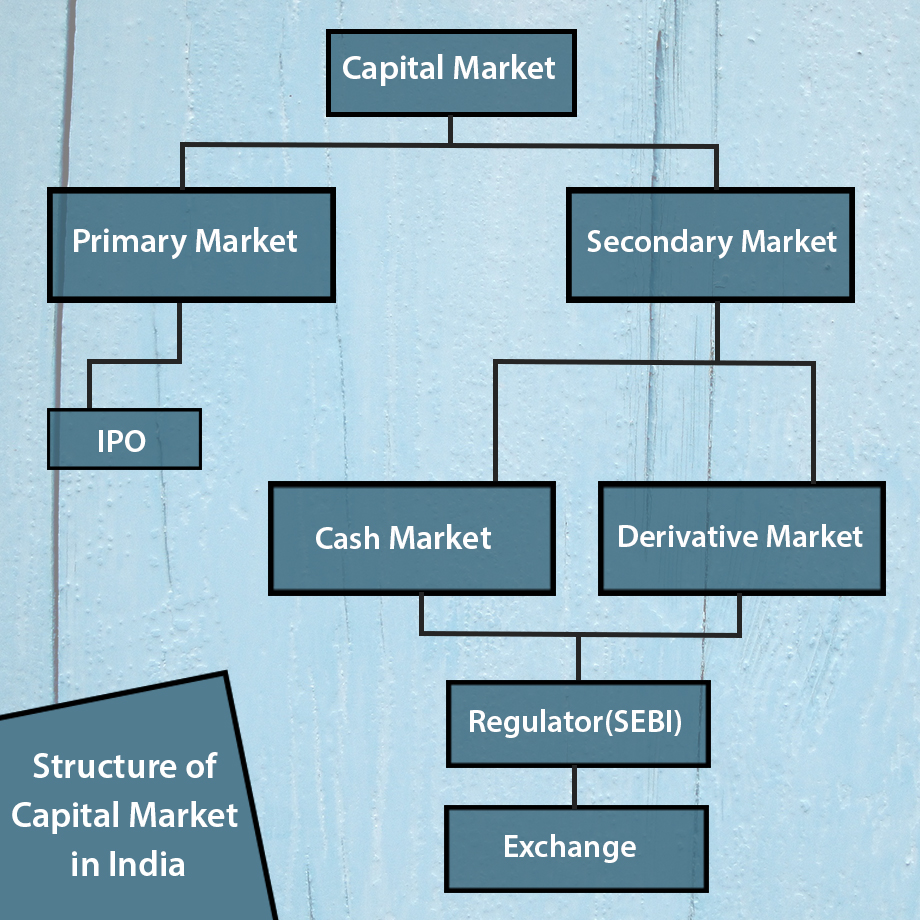

Capital market structure of India is complex. Also, it makes up the many a part of a financial market. Let us look at the essential definition of the Capital Market. It’s an area for long-term financial assets which have long or indefinite maturity. The capital market provides long-term debt and equity finance for the govt and the corporate sector.

Further, Capital market divides into the first market and secondary market

Primary Market:

Primary market is one sort of capital market where various companies issues their shares and bonds first time to boost funds from the public, it's called Initial Public Offering (IPO).

Secondary Market:

A secondary market may be a sort of capital market where issued securities are bought and sold. Structure of Capital Market in India Secondary Market has got two wings namely Cash Market and Derivative Market

Capital Market Regulator:

SEBI (Securities and Exchange Board of India) is a regulator of Indian capital Market. It had been established in 1988. The essential function of SEBI is to guard the interest of investors.

SEBI is additionally the Regulator for Commodity Market. Before this forward market Commission (FMC) was the regulator of the commodity market.

Exchanges of Capital Market in India:

Exchange provides an electronic and transparent platform to shop for and sell the shares. Stock market also provides the power for issue and redemption of securities. In India, there's two national Exchange of stock exchange. They're the NES and the BSE. Further, there are two national exchanges for commodity, MCX & NCDEX.

A BRIEF HISTORY OF INDIAN EXCHANGES

The history of Exchanges of Indian capital Market is much back to the 1800s. The following are the milestones in the Indian capital market.

The 1800s

• 1854: Dalal Street got a permanent location.

• 1875: BSE has established as “The Native Shares and Stock Brokers Association”

The 1900s

• 1956: In 1956 BSE became the first stock market to be recognized under the Securities Contract Act.

• 1993: In 1993 NSE has recognized as a stock market.

The 2000s

• 2000: in the year 2000 internet trading has started at NSE.

• 2000: Derivative Trading (Index Futures) has started at NSE.

• 2001: Derivative Trading has started at BSE.

Indian Broker

The broker acts as a bridge between the exchange and traders (Buyers & Sellers). Moreover, any Indian can invest or trade in a stock exchange or commodity market. But for this, you have the open Demat account with a registered broker.

The New Delhi market is that the marketplace for long term loan able funds as distinct from money market which deals in short-term funds.

Growth and classification of Indian capital market

It refers to the facilities and institutional arrangements for borrowing and lending ‘term funds’, medium term and future funds. In principal capital market loans are employed by industries mainly for fixed investment. It doesn't deal in capital goods, but cares with raising money capital or purpose of investment.

CLASSIFICATION:

The capital market in India includes the subsequent institutions (i.e., supply of funds tor capital markets comes largely from these); (i) Commercial Banks; (ii) Insurance Companies (LIC and GIC); (iii) Specialised financial institutions like IFCI, IDBI, ICICI, SIDCS, SFCS, UTI etc.; (iv) Provident Fund Societies; (v) Merchant Banking Agencies; (vi) Credit Guarantee Corporations. Individuals who invest directly on their own in securities also are suppliers of fund to the capital market.

Thus, like all the markets the capital market is additionally composed of these who demand funds (borrowers) and people who supply funds (lenders). An ideal capital market at tempts to supply adequate capital at reasonable rate of return for any business, or industrial proposition which offers a prospective high yield to form borrowing worthwhile.

The Indian capital market is split into gilt-edged market and therefore the industrial stock exchange. The gilt-edged market refers to the marketplace for government and semi-government securities, backed by the RBI. The securities traded during this market are stable in value and are much wanted by banks and other institutions.

The industrial securities market refers to the marketplace for shares and debentures of old and new companies. This market is further divided into the new issues market and old capital market meaning the stock exchange.

The new issue market refers to the raising of latest capital within the form of shares and debentures, whereas the old capital market deals with securities already issued by companies.

The capital market is additionally divided in primary capital market and secondary capital market. The first market refers to the new issue market, which relates to the issue of shares, preference shares, and debentures of non-government public limited companies and also to the realising of fresh capital by government companies, and therefore the issue of public sector bonds.

The secondary market on the opposite hand is that the marketplace for old and already issued securities. The secondary capital market consists of industrial security market or the stock exchange in which industrial securities are bought and sold and the gilt- edged market in which the govt and semi-government securities are traded.

Growth of Indian capital market

Indian Capital Market before Independence:

Indian capital market was hardly existent in the pre-independence times. Agriculture was the mainstay of economy but there was hardly any future lending to agricultural sector. Similarly, the growth of industrial stock exchange was very much hampered since there were only a few companies and the number of securities traded in the stock exchanges was even smaller.

Indian capital market was dominated by gilt-edged marketplace for government and semi-government securities. Individual investors were very few in numbers and that too were limited to the affluent classes in the urban and rural areas. Last but not the least, there were no specialised intermediaries and agencies to mobilise the savings of the general public and channelize them to investment.

Indian Capital Market after Independence:

Since independence, the Indian capital market has made widespread growth in all the areas as reflected by increased volume of savings and investments. In 1951, the number of joint stock companies (which is a vital indicator of the growth of capital market) was 28,500 both public limited and private limited companies with a paid-up capital of Rs. 775 crores, which in 1990 stood at 50,000 companies with a paid-up capital of Rs. 20,000 crores. The rate of growth of investment has been phenomenal in recent years, in keeping with the accelerated tempo of development of the Indian economy under the impetus of the five-year plans.

Factors influencing capital market

The firm trend in the market is basically affected by two important factors: (i) operations of the institutional investors in the market; and (ii) the excellent results flowing in from the corporate sector.

New Financial Intermediaries in Capital Market: