Unit-1

Shares and Mutual Funds

Share is the smallest unit of the capital of a company. In other words, A unit of ownership, that represents an equal proportion of a company’s capital is called as shares.

A share is the interest of a shareholder in a definite portion of the capital. It expresses a proprietary relationship between the company and the shareholder. A shareholder is the proportionate owner of the company.

A share is the smallest unit of the total share capital of the company

The share is regarded as unit of account that can represent several monetary instruments such as stocks, mutual funds, etc.

Share market is the aggregation of buyers and sellers of stock shares or stock.

Any stock exchange is for trading the stocks.

There are two stock exchanges in India-

- National stock exchange

- Bombay stock exchange

Note- If a person owns the shares of a company’s stock is known as shareholder.

Here we study two types of shares-

Ordinary shares or common stock-

These types of shares entitle the shareholder to share in the earnings of the company as and when they occur and to cast a vote at the company’s annual general metting’s and other official mettings.

Note- if the share is ordinary in the course of company’s business then it is called equity share.

Preference shares or preferred stock-

These types of shares entitle the shareholder to a fixed periodic income or interest but generally do not give him or her voting rights.

These types of shares are cumulative, non-cumulative, convertible etc.

Types of shares:

Mainly the shares are of two types i) Preference shares and ii) Equity shares or common shares or ordinary shares.

i) Preference shares: These shares have a priority over the equity shares. From the profits made by a company, a dividend at a fixed rate is paid to them first, before distributing any profit amount to the equity shareholders. Also, if and when the company is closed down then while returning of the capital, these shareholders get a preference.

Further types are:

- Cumulative and non-cumulative preference.

- Participating and non-participating preferences.

- Convertible and non-convertible preferences.

- Redeemable and non-redeemable preferences.

Again, preference shares are mainly of two types:

Cumulative Preference shares: In case of loss or inadequate profit, the preference shareholders are not paid their fixed rate of dividend, then the dividend is accumulated in the subsequent years to these shareholders & is paid preferentially whenever possible.

Non-cumulative Preference shares: As in the case of cumulative preference shares, here the unpaid dividends do not accumulate.

Stock: A group of fully paid shares as put together is known as stock.

Face value or nominal value:

It is the original cost of the stock shown on certificate.

Or

Face value: Each share is assigned the value in Rs as its worth called Face value.

Market value:

A share being a transferable document, it can be sold in the open market.

The market value is the value at which the shares are traded

i) If market value = face value, then the share is to be par

Ii) If market value < face value, the share is said to be below par or at a discount

Iii) If Market value > Face value, then the share is said to be above par or at premium.

Share Market

Shareholders are allowed to buy or sell shares like commodities. Selling or buying a share for a price higher than its face value is legal. The share prices are allowed to be subject to the market forces of demand and supply and thus the prices at which shares are traded can be above or below the face value.

The place at which the shares are bought and sold is called a share market or stock Exchange and the price at which a share is traded is called its Market Price (MP) or the Market value. If the market price of a share is same as its face value, then the share is said to be traded at Par.

If M.P. Is greater than face value of a share, then the share is said to be available at a premium or above par and is called premium share or above par share

If M.P. Is lower than face value of a share, then the share is said to be available at a discount or below par & the share is called a discount share or below par share.

Brokerage-

Brokerage is the commission charged by broker for buying and selling of shares from buyer or seller.

Important formulae-

Note-

- Buying: Actual price of the share = Market value + Brokerage per share

- Selling: Actual price of the share = Market value - Brokerage per share

Key takeaways-

- A share is the interest of a shareholder in a definite portion of the capital.

- Share market is the aggregation of buyers and sellers of stock shares or stock.

- If the share is ordinary in the course of company’s business then it is called equity share.

- A group of fully paid shares as put together is known as stock.

- Each share is assigned the value in Rs as its worth called Face value.

Dividend-

A share is a Part of the company. When the company makes profit, you often receive a part of it. This is the primary source of income. Dividend depends on the profit made by a company.

Dividend is declared by the company on the face value of a share. When the company makes profit, we receive a part of it and it is the primary source of income

Equity shares:

These are sold in the market to public, there by collecti8ng the required huge capital for the company. They are entitled to get dividend only after the fixed rate of dividend is paid to preference shareholders. Similarly, at the time of winding up of the company, only after returning preference share capital in full, and if there is any surplus, it will be paid to equity share holder.

Bonus shares: Bonus shares are additional shares given to the shareholder without any additional cost; based on the number of shares that a shareholder own. Normally, bonus shares are declared in the ratio.

These shares are issued to existing equity shareholders and represent divided paid in the form of shares instead of cash payment. These are fully paid shares and are distributed in proportion of numbers of shares in possession of the share’s holders.

Brokerage: Brokerage is the commission charged by broker for buying and selling of shares from buyer or seller. If you are buying shares, brokerage is added to the market price and if you selling shares, brokerage is subtracted from the market value.

The profit made by the company is passed on to the shareholders in the form of dividends. But the dividend on a share is calculated on its face value, whereas the market value, which is actual amount invested by the shareholder is generally very much higher than the place value. Therefore, dividend is not always the option

The other form of passing the profit by the company to their shareholder is to reward the shareholders by way of bonus shares.

Splitting of shares

A share of face value ₹100 is broken up into 10 shares of face value ₹10. The investor having old x shares of face value ₹100 each. Is then assigned new 10x shares of face value ₹10.

Bonus Shares | Right Issue |

| These are not free, are sold to the shareholder, but at a discounted price |

2. Given away proportionately | Offered proportionately for sale |

3. The purpose is to distribute the profit | The purpose is to generate additional fund |

Examples on bonus shares:

Example: Nitu had bought 100 shares of Colgate at ₹685 per share, the face value of each share begins₹10. The company decided to split the shares so that. The new face value would be ₹ 2 per share. If the market price of the shares after the spilt is ₹250 each, find out the numbers of shares held by Nitu and her gain after split

Solution:

Nitu bought 100 shares of face value ₹ 10, at ₹ 685 per share.

She spent ₹ (100 x 685) =₹68,500 for buying these shares

When a share of face value ₹ 10 was split into shares of face value ₹ 2 each, then foe old value 10/2 = 5 new shares are assigned. Thus 100 shares of nitu with face value 10 were converted 100 x 10/2 = 500 shares of face value of ₹ 2 each.

Thus, into now has 500 shares of Colgate with face value ₹ 2.

The market value of each share after spilt is ₹ 250

The market value of 500 shares of Nitu is

₹ (500 x 250) = ₹ 125000

Her gain is ₹ (1,25,000-68,500) = ₹ 56,500.

Example: A salesman is appointed on a fixed monthly salary of Rs. 1,500/- together with a commission at 5% on the sales over Rs. 10,000/- during a month. If his monthly income is Rs. 2,050/-, find his sales during that month.

Solution:

Commission at 5% on the sales over Rs. 10,000/-

= monthly income - monthly salary

=Rs. 2050-1500

= Rs. 550/- the sales over Rs. 10,000/-

= Rs. 550 ×  = Rs. 11,000/-

= Rs. 11,000/-

Total sales during the month = Rs. (10,000 + 11,000) = Rs. 21,000/-

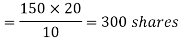

Q3. Mr. Prashant invested Rs. 75,375/- to purchase equity shares of a company at market price of Rs. 250 /- through a brokerage firm, charging 0.5% brokerage. The face value of a share is Rs. 10/-. How many shares did Mr. Prashant purchase?

Solution:

Brokerage per share = 250 x

= 1.25 cost of purchasing one share

= 250+1.25

=251.25

∴Number of shares purchased = = 300

= 300

Example: Mr. Sandeep received Rs. 4,30,272 /- after selling shares of a company at market price of Rs. 720 /- through Share khan Ltd., with brokerage 0.4%. Find the number of shares he sold.

Solution:

Brokerage per share = 720 x 0.4/100

= 2.88 100 selling prices of a share

= 720 - 2.88

= 717.12

∴Number of shares sold =  = 600

= 600

Example: Mr. Deepal Rana purchased 30 shares of Rs. 10/- each of Medi computers Ltd. On 20th Jan. 2007, at Rs. 36/- per share. On 3rd April 2007, the company decided to split their shares from the face value of Rs. 10/- per share to Rs. 2/- per share. On 4th April 2007, the market value of each share was Rs. 8/- per share. Find Mr. Deepal Rana’s gain or loss, if he was to sell the shares on 4th April 2007? (No brokerage was involved in the transaction).

Solution:

On 20th Jan 2007 purchase cost of 30 shares

= 30 x 36 = 1080/-

On 3rd April 2007, each Rs. 10/- share became 5 shares of Rs. 2/- each.

No. Of shares = 30 x 5 =150

On 4th April 2007, market value of 150 shares was @ Rs. 8 each

= 150 x 8 = 1200

∴His gain = 1200-1080 = 120/-

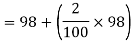

Example: Rahul purchased 500 shares of Rs. 100 of company A at Rs. 700 /-. After 2 months, he received a dividend of 25 %. After 6 months, he also got one bonus share for every 4 shares held. After 5 months, he sold all his shares at Rs. 610/- each. The brokerage was 2% on both, purchases &sales. Find his percentage return on the investment.

Solution: For purchase: Face value = Rs. 100 /-

No. Of shares = 500, market price = Rs.700/-

Dividend = 25%, brokerage = 2%

Purchase price of one share = 700 + x700= 714

∴Total purchase = 500 x 714 = Rs.3,57,000/-

Dividend = of 100 i.e. Rs. 25 /- per share

of 100 i.e. Rs. 25 /- per share

∴Total dividend = 500 x25 = Rs. 12,500 /-

Now, bonus shares are 1 for every 4 shares.

No. Of bonus shares = x 500 = 125

x 500 = 125

∴Total No. Of shares = 500 +125 =625

For sales, No. Of shares = 625, market price = 610,

Brokerage 2%

Sale price of one share = 610 - 2% of 610 = 597.8

∴Total sale value = sale price of one share x No. Of shares = 597.8 x 625 = Rs. 3, 73,625/-

Net profit = sale value + Dividend - purchase value = 3,73,625 + 12500 - 3,57,000 = Rs. 29,125/-

∴% gain =  x 100 = 8.16

x 100 = 8.16

= 8.16

Key takeaways

- Dividend is declared by the company on the face value of a share.

- Bonus shares are additional shares given to the shareholder without any additional cost; based on the number of shares that a shareholder own. Normally, bonus shares are declared in the ratio.

- Brokerage is the commission charged by broker for buying and selling of shares from buyer or seller.

“Mutual Fund is a pool of money collected from investors and invest in stocks.”

In other words- An investment programme funded by shareholder’s, that trades in diversified holding and professionally managed is called as mutual funds.

A mutual fund is basically at less risk as compared to shares. All the profits or losses of the fund are shared by all the investors in the same proportion as the amount of contribution made by them.

Mutual fund investments are subject to market risk.

There are many mutual funds but all mutual funds are of two types- open ended funds and closed ended funds.

Open-ended Fund-

There is no limit to the number of units purchased and sold in open ended fund

It has no fixed maturity period.

A number called Net Asset Value is used to determine the value of a share in open-ended fund at any time.

Investor can buy and sells his units at Net Asset Value (NAV) which are declared on a daily basis.

Closed-ended Fund-

In closed-ended fund will issue a fixed number of shares are issued to the public. The price of share in a closed-ended fund is determined by market-demand.

These types of funds are not redeemable.

This fund also known as “Closed-end investment” or “closed-end mutual fund.”

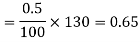

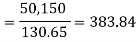

Example: How many shares of market price of Rs.130 each, can be purchased for Rs.50150 with brokerage being 0.5%?

Sol.

It is given that-

Market price for one share = Rs. 130

Total amount invested = Rs.50,150

And brokerage = 0.5

Brokerage per share = 0.5% of market price

Purchased price for one share = Market price + Brokerage

= 130+0.65 = 130.65

Example: There are two investments given below, then find out which investment is better?

7% of Rs. 100 shares at Rs. 120 or 8% of Rs. 10 shares at Rs. 13.50?

Sol.

Suppose the investment amount is = Rs. X

First situation-

It is given that- rate of dividend = 7%

F.V = 100, and Market value = Rs. 120

Second situation-

It is given that- rate of dividend = 8%

F.V = 10, and Market value = Rs. 13.50

Here we see that the dividend in second situation is more than the first situation.

Hence we conclude that the second situation is more profitable for investment.

Example: Mrs. Kapoor invested to Rs. 80,000 to purchase equity shares of Reliance company at market value of Rs. 210 each through a broker, charging 1% brokerase. The face value of a share is Rs. 10. How many shares did saptak purchase?

Sol.

It is given that-

Total Investment = 80,000

M.V. = Rs. 210, F.V. = Rs. 10, Brokerage = 1%

Now, Brokerage per share = 1% of M.V.

So that, Purchase price of 1 share = M.V. + Brokerage

= 210 + 2.1 = 212.10

Example: Amandeep purchased 150 shares of BOB at Rs. 210 on 3rd Jan 2019. On 13th Feb. 2019, the company decided to split all the shares of company so that the face value of the share become Rs. 10 from Rs. 20 per share. The market price as on 30th July, 2019 is Rs. 300. Find number of shares held by Amandeep as on 30th July 2019. Also Find gain as on 30th July 2019.

Sol.

It is given that-

Total number of shares = 150

M.V. = Rs. 210, F.V. =Rs. 20.

Total amount invested = Number of shares × M.V.

= 150 × 210

= 31,500

Number of shares held on 30th July 2019

Actual value of shares on 30th July 2014

= 300 × 300

= 90,000

Profit = 90,000 – 31,500

= 58,500

Key takeaways-

- “Mutual Fund is a pool of money collected from investors and invest in stocks.”

- A number called Net Asset Value is used to determine the value of a share in open-ended fund at any time.

- In closed-ended fund will issue a fixed number of shares are issued to the public.

A mutual fund price per share is known as Net Asset Value (N.A.V.).

N.A.V. May represent the value of the total equity.

Net Asset Value-

A mutual funds price per share or unit is called Net Asset Value or N.A.V. All mutual funds buy and sells, orders are processed at the N.A.V of the trade date

Entry Load and Exit load-

Entry load and Exit load are the brokerage while buying and selling the mutual fund respectively.

Entry load is charged at the time, an investor purchases the units and exit load is charged at the time of sale of all units.

Note-

- Buying: Actual price of the Mutual fund = N.A.V + Entry load per share

- Selling: Actual price of the Mutual fund = N.A.V - Exit load per share.

Example: Amit invests Rs. 65,000 in ABC mutual fund where N.A.V. Of Rs. 98. How many units he bought, if entry load is 2%.

Sol.

Amount Invested = Rs. 65,000

N.A.V. = Rs. 98, Entry Load = 2%

Actual Purchase amount of 1 unit = NAV + Entry load

Example: If a ICICI M.F. Had a N.A.V. Of Rs. 60 at the beginning of the year and if percentage increase in NAV during the year was 15% Find absolute change in N.A.V.

Sol.

NAV at the beginning of the year = Rs. 60

Percent change in NAV = 15%

Absolute change in NAV = (% change in NAV) × (NAV at beginning of year)

NAV at the end of the year = (Absolute change in NAV) + (NAV at beginning of the year)

= 9 + 60 = 69

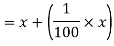

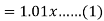

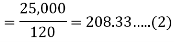

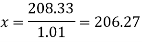

Example: Rakhi invested Rs. 25,000 in LPU M.F. With entry load 1%. Find the N.A.V. If the number of units purchased was 120.

Sol.

Let N.A.V. Of 1 unit = Rs. X

Purchase price of 1 unit = NAV + Entry load

It is given that-

Amount investment = Rs. 25,000

No. Of unit purchase = 120.

From equation (1) and (2), we get-

1.01 X = 208.33

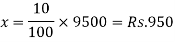

Example: Mr. Sharma purchased 500 units of Bajaj M.F. At Rs. 8,000 and sold all the units after 2 months when NAV of Rs. 35. The short term gain tax was 10% of the profit. Find his net profit or loss.

Sol.

It is given that-

No. Of unit purchased = 500

Purchase Amount = Rs. 8,000

Now selling Price of all the units

= 35 × 500 = 17,500

So that

Profit = SP – Purchasing Price = 17,500 – 8,000 = 9,500

Short term gain tax = 10% of profit

Net profit = 9,500 – 950 = Rs. 8,550

Key takeaways-

- A mutual funds price per share or unit is called Net Asset Value or N.A.V. All mutual funds buy and sells,

- Entry load and Exit load are the brokerage while buying and selling the mutual fund respectively.

Systematic Investment Plan-

S.I.P is plan where investors make regular, equal payment into a mutual fund. In this plan, investor can be benefitted by buying more units when the price falls and less units when the price rises.

This scheme helps reduce the average cost per unit of investment, through a method called Average Rupee cost or Rupee cost Averaging.

Also, in this plan investor may choose to increase or decrease the investment amount. In India, a recurring payment can be set for SIP using Electronic Clearing Services (ECS).

SIP is like a recurring deposit in a bank, where you put a fixed amount every month.

Example: Mr. Dev invested Rs. 5,000 every month for 5 months in RELIANCE systematic investment plan (SIP) with N.A.V. Of 35, 41, 40, 45 and 50 respectively the entry load was

2%. After 9 months she sold all the units when N.A.V. Of 48.

Sol.

Amount invested every month = 5,000.

Entry Load = 2%. Exit Load = Nil.

Selling price of 1 unit = 48

Month | N.A.V. | Entry load | Purchased price of 1 unit | Number of unit purchased |

1 | 35 | 0.70 | 35.70 | 5000/35.70 = 140.056 |

2 | 41 | 0.82 | 40.82 | 119.560 |

3 | 40 | 0.80 | 40.80 | 122.549 |

4 | 45 | 0.90 | 45.90 | 108.932 |

5 | 50 | 1 | 51 | 98.039 |

Total |

|

| 215.22 | 589.136 |

Average price of 1 unit = Total Amount Invested / Total no. Of unit purchased

= 25,000/589.136

= 42.435

Average (mean) price of 1 unit = Total amount / 5

= 215.22 / 5

= 43.044

Total S.P. = 48 × 589.136

= 28,278.528

Gain = S.P. – Purchase price

= 28,278.528 – 25,000 = 3,278.528

Key takeaways-

- S.I.P is plan where investors make regular, equal payment into a mutual fund.

- SIP is like a recurring deposit in a bank, where you put a fixed amount every month.

References-

- Mathematics and Statistics for Business – R. S. Bhardwaj – Excel Books.

- Business Mathematics and Statistics – Subhanjali Chopra – Pearson publication.

- Fundamentals of Business Mathematics and Statistics – ICAI – ICAI.

- Business Mathematics and Statistics – Dr. J K Das, N Das – McGraw Hill Education.

- Mathematical and statistical techniques, Dr. Abhilasha S. Magar & Manohar B. Bhagirath

- IGNOU