UNIT 1

Introduction and Basic Concepts

Business Economics, also called Managerial Economics, is the application of economic theory and methodology to business. Business involves decision-making. Decision making means the process of selecting one out of two or more alternative courses of action. The question of choice arises because the basic resources such as capital, land, labour and management are limited and can be employed in alternative uses. The decision-making function thus becomes one of making choice and taking decisions that will provide the most efficient means of attaining a desired end, say, profit maximation.

Definition

According to Mc Nair and Meriam, “Business economic consists of the use of economic modes of thought to analyse business situations.”

According to Mansfield, “business economics is concerned with the application of economic concepts and economic analysis to the problem of formulating rational decision making”.

Nature of business economics

- Microeconomics - Business economics is microeconomic in character. This is because it studies the problems of an individual business unit. It does not study the problems of the entire economy.

2. Normative science - Managerial economics is a normative science. Under particular circumstances it is concerned with what management should do. It determines the goals of the enterprise. Then it develops the ways to achieve these goals.

3. Pragmatic - Business economics is pragmatic. It concentrates on making economic theory more application-oriented. It tries to solve the managerial problems in their day-to-day functioning.

4. Prescriptive - Managerial economics is prescriptive rather than descriptive. It prescribes solutions to various business problems.

5. Uses macroeconomics - Macroeconomics is also useful to business economics. Macro-economic provides an intelligent understanding of the environment in which the business operates.

6. Management oriented - The main aim of managerial economics is to help the management in taking correct decisions and preparing plans and policies for the future.

Scope of business economics

- Demand Analysis and Forecasting: A business firm is economic organisations which transform productive resources into goods to be sold in the market. A major part of business decision making depends on accurate estimates of demand. A demand forecast can serve as a guide to management for maintaining and strengthening market position and enlarging profits. Demands analysis helps identify the various factors influencing the product demand and thus provides guidelines for manipulating demand.

2. Cost and Production Analysis: A study of economic costs, combined with the data drawn from the firm’s accounting records, can yield significant cost estimates which are useful for management decisions. An element of cost uncertainty exists because all the factors determining costs are not known and controllable. Discovering economic costs and the ability to measure them are the necessary steps for more effective profit planning, cost control and sound pricing practices. Production analysis is narrower, in scope than cost analysis. Production analysis frequently proceeds in physical terms while cost analysis proceeds in monetary terms.

3. Pricing Decisions, Policies and Practices: Pricing is an important area of business economic. In fact, price is the genesis of a firms revenue and as such its success largely depends on how correctly the pricing decisions are taken. The important aspects dealt with under pricing include. Price Determination in Various Market Forms, Pricing Method, Differential Pricing, Product-line Pricing and Price Forecasting.

4. Profit Management: Business firms are generally organised for purpose of making profits and in the long run profits earned are taken as an important measure of the firms success. If knowledge about the future were perfect, profit analysis would have been a very easy task. However, in a world of uncertainty, expectations are not always realised so that profit planning and measurement constitute a difficult area of business economic.

5. Capital Management: Among the various types business problems, the most complex and troublesome for the business manager are those relating to a firm’s capital investments. Relatively large sums are involved and the problems are so complex that their solution requires considerable time and labour.

Importance of business economics

Business economics plays an important role in decision making in an organization. Decision making is a process of selecting the best course of action from the available alternatives

- Business economics covers various important concepts, such as Demand and Supply analysis; Short run cost and Long run costs; and Law of Diminishing Marginal Utility. These concepts support managers in identifying and analysing problems and finding solutions.

- It helps managers to identify and analyse various internal and external business factors and their impact on the functioning of the organisation.

- Business economics helps managers in framing various policies, such as pricing policies and cost policies, on the basis of economic study and findings.

- By studying various economic variables, such as cost production and business capital, organisations can predict the future.

- Business economics helps in establishing relationships between different economic factors, such as income, profits, losses, and market structure. This helps in guiding managers in effective decision making and running the organisation.

Key takeaways

- Business Economics is the integration of economic theory with business practice for the purpose of facilitating decision making and forward planning by management.

- Business Economics applies these tools in the process of business decision making.

Micro economics

Microeconomics (from Greek prefix mikro- meaning "small") is a branch of economics that studies the behavior of individuals and firms in making decisions regarding the allocation of scarce resources. “The interactions among these individuals and firms”

Microeconomics is the study of individuals, households and firm’s behavior in decision making and allocation of resources. It generally applies to markets of goods and services and deals with individual and economic issues.

Definition

Microeconomics is the study of individuals, households and firms' behavior in decision making and allocation of resources. It generally applies to markets of goods and services and deals with individual and economic issues.

Microeconomics is a branch of economics that studies the behavior of individuals and firms in making decisions regarding the allocation of scarce resources and the interactions among these individuals and firms.

This is considered to be basic economics. Microeconomics may be defined as that branch of economic analysis which studies the economic behavior of the individual unit, maybe a person, a particular household, or a particular firm.

The production of goods and services is based on allocation of scarce resources.

Efficient distribution of goods – this studies the matter relating to (a) Product pricing, (b) Factor pricing, (c) Economic welfare.

- Product pricing – it involves the determination of product price under monopoly, perfect competition, etc. considering demand, supply, cost production etc.

- Factor pricing - it involves the determination of price of factor inputs such as: land, labour, capital & organization in the form of rent, wage, interest & profit respectively.

- Economic welfare – it involves the study of maximum profit for producer and maximum benefit to consumer.

Macro economics

The term "macro" was first used in economics by Ragnar Frisch in 1933. However, it originated in the 16th and 17th century mercantilists as a methodological approach to economic problems. They were interested in the entire economic system. In the 18th century,

Physiocrats adopted it in the table economy, demonstrating a "wealth cycle" (i.e., net production) among the three classes represented by the peasant, landowner, and barren classes.

Malthus, Sismondi and Marx in the 19th century dealt with macroeconomic issues. Walrus, Wicksell and Fisher contributed modernly to the development of pre-Keynes macroeconomic analysis.

Certain economists such as Kassel, Marshall, Pigovian, Robertson, Hayek, and Hortley developed the Quantity Theory of Money and General Price Theory in the decade following World War I. But Keynes, who eventually developed the general theory of income, output, and employment in the wake of the Great Depression, has credit.

Economics is a science that deals with the production, Exchange and consumption of various goods in the economic system. It is a scarce resource that can lessen the abundance of human welfare. The central focus of Economics lies in the choice between resource scarcity and its alternative uses. The word "economics" is derived from two the Greek words oikos (House) and nemein (to manage) mean to manage the household budget "using the limited funds possible.

Macroeconomics is an important concept that considers the whole country and works for the welfare of the economy.

1. Business cycle analysis

Timing of economic fluctuations helps prevent or prepare for financial crises and long-term negative situations.

2. Formulation of economic policy

The fiscal and monetary policy system relies entirely on the widespread analysis of macroeconomic conditions in the country.

3. Reduce the effects of inflation and deflation

Macroeconomics is primarily aimed at helping governments and financial institutions prepare for economic stability in a country.

4. Promote material welfare

This stream of economics provides a broader perspective on social or national issues. Those who want to contribute to the welfare of society need to study macroeconomics.

5. Regulate the economic system

It continues to guarantee or check the proper functioning and actual position of the country's economy.

6. Solve economic problems

Macroeconomic theory and problem analysis help economists and governments understand the causes and possible solutions to such macro-level problems.

7. Economic development

By utilizing macroeconomic data to respond to various economic conditions, the door to national growth will be opened.

Key takeaways

- Microeconomics studies individual and business decisions, while macroeconomics analyzes decisions made by countries and governments.

- Microeconomics has been a bottom-up approach, focusing on supply and demand, and other forces that determine price levels.

- Macroeconomics takes a top-down approach, looks at the economy as a whole, and tries to determine its course and nature.

Functional relationship

A 'function' explains the relationship between two or more economic variables. A simple technical term is used to analyze and symbolizes a relationship between variables. It is called a function. It indicates how the value of dependent variable depends on the value of independent or other variables. It also explains how the value of one variable can be found by specifying the value of other variable.

For instance, economist generally links demand for good depends upon its price. It is expressed as D = f (P). Where D = Demand, P = Price and f = Functional relationship.

Functions are classifieds into two type namely explicit function and implicit function. Explicit function is one in which the value of one variable depends on the other in a definite form. For instance, the relationships between demand and price Implicit function is one in which the variables are interdependent.

Variables

A variable is magnitude of interest that can be measured. Variables can be endogenous and exogenous variables. Variables can be independent and dependent

Equations

An equation specifies the relationship between the dependent and independent variables. It specifies the direction of relation. Economic theory is a verbal expression of the functional relationships between economic variables. When the verbal expressions are transformed into algebraic form we get Equations. The term equation is a statement of equality of two expressions or variables. The two expressions of an equation are called the sides of the equation. Equations are used to calculate the value of an unknown variable. An equation specifies the relationship between the dependent and independent variables. Each equation is a concise statement of a particular relation.

For example, the functional relationship between consumption (C) and income (Y) can take different forms. The most simple equation; C = a (Y) states that consumption (C) is related to income (Y). It says nothing about the form that this relation takes.

Here ‘a’ is constant and it has a value greater than zero but less than one (0<a<1). Thus the equation shows that C is a constant proportion of income. For instance, if ‘a’ is 1/2then the consumer would always spend 50% of the income on consumption. The equation shows that if income is zero, consumption will also be zero.

C = a + b Y is yet another form of consumption function. Here value of a is positive and b is 0<b<1.

Graph

Graph is a geometric tool used to express the relationship between variables. It is a pictorial representation of data which shows how two or more sets of data or variables are related to one another.

A graph or a diagram presents the relationship between two or more sets of data or variables that are related to one another. Graph is most commonly used tool in modern economics. Graph depicts the functional relationship between two or more economic variables. The use of graph provides a better understanding of the economic generalizations. Graph presents a visual picture of an abstract idea. Also it is useful for accuracy and precision.

Graph can be drawn only two dimensional figures on a plain paper. It represents the values of only two variables at a time. The common method of constructing a graph or a diagram is described below:

A graph has a horizontal line termed as X axis and a vertical line termed as Y axis. The point of intersection between X and Y axis is termed as 'origin' point.

The surface is divided into four parts, each part is called a quadrant. The four quadrants are numbered in anticlockwise direction as depicts in following diagram.

|

Curves

The functional relationship between the variables specified in the form of equations can be shown by drawing line or outline which gradually deviates from being straight for some or all of its length in the graph.

Slopes

Slopes show how fast or at what rate, the dependant variable is changing in response to a change in the independent variable.

Schedule

Schedule is the tabular representation. For example Demand schedule is a tabular statement showing various quantities of a commodity being demanded at various levels of price, during a given period of time

Key takeaways

- Business economics deals with many economic relations and various concepts such as variables, functions, equations, graph, curves and slopes.

Household

All those people living under one roof are considered a household.

Households do two fundamental things vital to the economy.

1. Demand goods and services from product markets

2. Supply labor, capital, land, and entrepreneurial ability to resource markets.

Economists think of each household acting as a single decision-maker.

Householder: The key decision-maker in the household.

Economists assume that individuals, and thus households, attempt to maximize their utility.

UTILITY: The satisfaction received from consumption; the sense of well being. Utility is subjective (not objective). One household may have different goals than another.

Rational: They act in their own best interest (in the interest of their own goals- maximizing their utility), would not make choices that would make them worse off.

Households as Demanders

Personal income is allocated among three uses:

1. Savings

2. Consumption

3. Taxes

Consumption:

1. Durable goods

2. Nondurable goods

3. Services

Resource suppliers

- Households use their limited resources (labor, capital, land, and entrepreneurial ability) to maximize their own utility.

- They can use these resources at home, or they can sell these resources in the resource market to earn money to spend in the product market.

Firms

Business firms are a combination of manpower, financial, and physical resources which help in making managerial decisions. Societies can be classified into two main categories − production and consumption. Firms are the economic entities and are on the production side, whereas consumers are on the consumption side.

The performances of firms get analyzed in the framework of an economic model. The economic model of a firm is called the theory of the firm. Business decisions include many vital decisions like whether a firm should undertake research and development program, should a company launch a new product, etc.

Business decisions made by the managers are very important for the success and failure of a firm. Complexity in the business world continuously grows making the role of a manager or a decision maker of an organisation more challenging! The impact of goods production, marketing, and technological changes highly contribute to the complexity of the business environment.

Kinds of firms

1. Sole Proprietorships: A firm with a single owner who has the right to all profits and who bears unlimited liability for the firm's debts. Must raise all the money to start business, is solely responsible for all debts.

2. Partnerships: A firm with multiple owners who share the firm's profits and each of who bears unlimited liability for the firm's debts. Two or more people agree to contribute resources in return for a share of the profit or loss.

3. Corporations: A legal entity owned by stockholders whose liability is limited to the value of their stock.

Consumer

A consumer is a person (or group) who pays to consume the goods and/or services produced by a seller. A consumer can be a person (or group of people), generally categorized as an end user or target demographic for a product, good, or service.

Consumption, in economics, the use of goods and services by households. Consumption is distinct from consumption expenditure, which is the purchase of goods and services for use by households. Consumption differs from consumption expenditure primarily because durable goods, such as automobiles, generate an expenditure mainly in the period when they are purchased, but they generate “consumption services” (for example, an automobile provides transportation services) until they are replaced or scrapped.

The study of consumption behaviour plays a central role in both macroeconomics and microeconomics. Macroeconomists are interested in aggregate consumption for two distinct reasons. First, aggregate consumption determines aggregate saving, because saving is defined as the portion of income that is not consumed. Because aggregate saving feeds through the financial system to create the national supply of capital, it follows that aggregate consumption and saving behaviour has a powerful influence on an economy’s long-term productive capacity. Second, since consumption expenditure accounts for most of national output, understanding the dynamics of aggregate consumption expenditure is essential to understanding macroeconomic fluctuations and the business cycle.

Macroeconomists have studied consumption behaviour for many different reasons, using consumption data to measure poverty, to examine households’ preparedness for retirement, or to test theories of competition in retail industries.

Plant and industry

In the study of economics, a plant is an integrated workplace, usually all in one location. A plant generally consists of the physical capital, like the building and the equipment at a particular location that is used for the production of goods. A plant is also called a factory.

In a plant or industrial undertaking it may be required to take decisions on the following goals or objectives:

(1) The Inventory Goal:

The main aim is to have optimum inventory at all times. Large inventory will tie up a big working capital, whereas less inventory will involve hazards of running out of stock. The inventory level is decided by striking a balance between the cost of running out of stock and the cost of holding stock.

(2) The Production Goal:

It involves decisions on setting the level of output, low production costs, and maintenance of a stable work force.

(3) The Market Goals:

They are considered while taking decisions on sales strategy, i.e., when, deciding a level (amount) of sales and the (market) share of a particular concern in the total market sale.

(4) The Profit Goal:

Profit is actually a measure of performance and an excellent indicator of the general efficiency of a plant or industrial undertaking. The decision involved in profit goal is the determination of the aspiration level of the concern with regard to profits. Taking from shareholders to the workers everybody is interested to maximize the profits.

Key takeaways

- All those people living under one roof are considered a household.

- A consumer is a person (or group) who pays to consume the goods and/or services produced by a seller

- A plant generally consists of the physical capital, like the building and the equipment at a particular location that is used for the production of goods.

Economic objectives of the firm

|

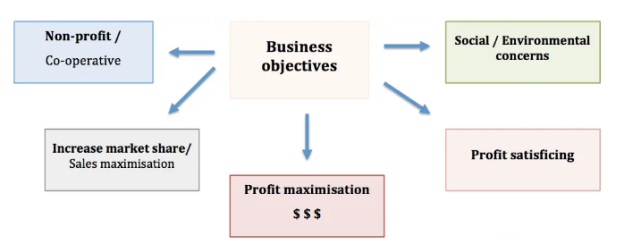

The main objectives of firms are:

- Profit maximization - Usually, in economics, we assume firms are concerned with maximizing profit. Higher profit means:

- Higher dividends for shareholders.

- More profit can be used to finance research and development.

- Higher profit makes the firm less vulnerable to takeover.

- Higher profit enables higher salaries for workers

- Sales maximization – Firms wants to increase their market share – even if it means less profit. This could occur for various reasons:

- Increased market share increases monopoly power and may enable the firm to put up prices and make more profit in the long run.

- Managers prefer to work for bigger companies as it leads to greater prestige and higher salaries.

- Increasing market share may force rivals out of business.

- Social/environmental concerns - A firm may incur extra expense to choose products which don’t harm the environment or products not tested on animals. Alternatively, firms may be concerned about local community / charitable concerns.

- Profit satisficing – Profit satisficing is a situation where there is a separation of ownership and control. As a result, the owners are likely to have different objectives to the managers and workers. In short, owners wish to maximise profits, but workers and managers may not. It is an example of the principal-agent problem

- Co-operatives - A co-operative is run to maximise the welfare of all stakeholders – especially workers. Any profit the co-operative makes will be shared amongst all members.

Non economic goals of the firm

- Good work environment for employees

- Quality products and services for customers

- Good corporate citizenship and social responsibility

Key takeaways

- The main objectives of the firm include Profit maximization, Sales maximization, Increased market share/market dominance, Social/environmental concerns, Profit satisficing, Co-operatives

References

- Business economics by H.L Ahuja

- Business economics application and analysis by Dr. Raj kumar

- Business economics by T Aryamala

- Business economics by SK Agarwal