UNIT-3

EXPORT FINANCE

There are various methods of payment. Each method of payment has its own advantages and limitations. The methods of payment can be broadly divided into 6 groups as follows:

1. Payment in Advance

This method does not involve any risk of bad debts, provided entire amount is received in advance. At times, a certain per cent is paid in advance, say 50% and the rest on delivery of products.

This method of payment is desirable when:

(a) The financial position of the buyer is weak or credit worthiness of the buyer is not known.

(b) The economic/ political conditions in the buyer's country are unstable.

(c) The seller is not willing to assume credit risk, as in the case of open account method.

2. Open Account Method

After the goods are dispatched, the exporter sends documents of title to goods to the importer along with his invoice and then waits for payment. If no credit is allowed, the importer pays immediately.

This method is simple and avoids additional charges involved in other methods of payment. However, there is a considerable risk involved in this method.

The exporter may follow this method only when:

The exporter is confident of the buyer's financial standing and reputation.

There is long- and well-established relationship between the two parties.

The exporter has enough financial regulations in the importer s country otherwise the importer may not pay the amount on stipulated date.

There are no exchange regulations in the importer's country otherwise the importer may not pay the amount on stipulated date.

The foreign exchange regulations of the exporting country should permit such payment.

The political environment is sound and stable in the importer's country.

3. Payment against Shipment on Consignment

The exporter supplies the goods to the overseas consignee or agent, without actually giving up the title. Payment is made only when the goods are ultimately old by the overseas consignee to other parties.

This method is costly, because of commission to be paid to the consignee, apart from other charges and at the same time it is very risky. The consignee may return the goods back if remained unsold and even the consignee may not clear of the dues in time. The price to be realised is also uncertain as it depends on market conditions in the buyer's country.

In India prior approval is required to be taken from the exchange control department of RBI for shipment on consignment basis.

4. Documentary Bills

Under this method, the exporter agrees to submit the document to his bank along with the bill of exchange. The documents required are (a) a full set of bill of lading (b) invoice (c) marine insurance policy and other documents, if required.

There are two main types of documentary bills:

(a) Documents against Payment (DP)

(b) Documents against Acceptance (DA)

(a) Documents against Payment (DP Bills):

The documents are released to the importer against payment. This method indicates that the payment is made against Sight Draft Necessary arrangements will have to be made to store the goods, a delay in payment occurs.

The risk involved is that the importer may refuse to accept the documents and to pay against them. The reasons for non-acceptance may be political or commercial ones. In India, ECGC covers losses arising out of such risks.

(b) Documents against Acceptance (DA Bills):

The documents are released against acceptance of the bill o exchange. The credit is allowed for a certain period, say 90 days. However, the exporter need not wait for payment till the bill is met on due date; as he can discount the bill with the negotiating bank and can obtain funds immediately after shipment of goods.

In case of D/A as compared to D/P bills, the risk involved is much greater, as the importer takes the possession of goods before the final payment is made to the exporter. This means, there are chances of bad debts, if bill of exchange is dishonoured.

If the importer fails to pay on due date, the exporter, will have to start civil proceedings to receive his payment, if all other alternatives fail. The risk involved can be insured with ECGC.

5. Deferred Credit Payment:

Generally, capital goods are sold on deferred credit basis. The credit period allowed is more than 180 days, and it can be even 10 years depending on the value of goods and other terms of contract. The exporter receives the payment in instalment over a period of time. The payment is generally received through the bank in the form of bank drafts. The exporter needs to send reminders to the importer to make payment of instalments on the due dates as per the contract.

6. Letter of Credit

This method of payment has become the most popular form in recent times, as it is more secured as compared to other methods of payment (other than advance payment).

A letter of credit can be defined as "an undertaking by importer's bank stating that payment will be made to the exporter it the required documents are presented to the bank within the validity of the L/C".

The various parties to LC include:

(a) Applicant-the importer who makes an application to his bank for LC

(b) Issuing Bank - the importer's bank which issues the LC.

(c) Advising Bank-the bank in exporter's country which informs the exporter regarding the receipt of LC.

(d) Beneficiary— the exporter or the third party (if LC is transferred) who gets the money of LC.

(e) Confirming Bank - the bank in exporter's country that guarantees the LC

(f) Negotiating Bank - the exporter's bank that negotiates th export documents and realizes LC proceeds.

The following are the steps in the process of opening of a letter of credit:

Exporter's Request: The exporter requests the importer to issue LC in his favour. LC is the most secured form of payment in foreign trade.

Importer's Request to his Bank: The importer requests his bank to open a L/C. He may either pay the amount of credit in advance or may request the bank to open credit in his current account with the bank.

Issue of LC: The issuing bank issues the L/C and forwards it to its correspondent bank with a request to inform the beneficiary that the L/C has been opened. The issuing bank may also request the advising bank to add its confirmation to the L/C, if so required by the beneficiary.

Receipt of LC: The exporter takes in his possession the L/C. He should see to it that the L/C is confirmed.

Shipment of Goods: Then the exporter supplies the goods and presents the full set of documents along with the draft to the negotiating bank.

Scrutiny of Documents: The negotiating bank then scrutinises the documents and if they are in order makes the payment to the exporter.

Realisation of Payment: The issuing bank will reimburse the amount (which is paid to the exporter) to the negotiating bank.

Documents to Importer: The issuing Bank in turn presents the documents to the importer and debit his account for the corresponding amount.

TYPES OF LETTER OF CREDIT

There are several types of letter of credit, which are stated as follows.

1. Revocable L/C

Revocable L/C is one which can be cancelled or modified at any time without notice to the beneficiary. In this type of L/C, the issuing bank reserves the right to withdraw, cancel of modify the credit, at any time. It might be revoked before the goods are dispatched. The major weakness of revocable L/C is that it may be cancelled or modified without prior permission of the beneficiary by the issuing bank. This type of L/C is not very popular.

2. Irrevocable L/C

This type of L/C is preferred to revocable letter of credit. In this type, once the L/C is accepted by the exporter, it cannot be cancelled or modified by the buyer of issuing bank without prior permission of the beneficiary and other parties involved such as confirming bank. Exporters normally insist on irrevocable letter of credit because it does not have inherent weakness of revocable letter of credit.

3. Confirmed L/C

When it is necessary for an irrevocable credit to be confirmed for the beneficiary by another bank, arrangements bank adds its confirmation on receiving necessary authorization from the issuing bank, it binds itself to negotiate documents there under.

4. Unconfirmed L/C

As the name indicates, Unconfirmed L/C is one to which confirmation is not added by the advising bank. Therefore, the bank does not accept the liability to make payment. The risk of non-payment is high.

5. With Recourse L/C

In this type, the exporter is held liable to the paying/negotiating bank, if the draft/bill drawn against L/C is not honored by the importer issuing bank. The negotiating bank can make the exporter to pay the amount along with the interest, which it has already paid to the beneficiary.

6. Without Recourse L/C

It is popularly known as sans recourse L/C. this L/C is without the condition. In case the bill is not honoured by the importer and the negotiating bank has already paid to the exporter, the negotiating bank cannot ask the exporter, to refund the amount. The negotiating bank can take recourse to the opening bank and the opening bank can demand money from the importer. This is generally an irrevocable L/C which projects the interests of the exporter. Hence an irrevocable, without recourse and confirmed L/C is the most secured L/C.

7. Revolving Letter of Credit

The importer opens a L/C with substantial amount for a specific period in favour of the exporter. The exporter can make one or more shipments and withdraw payment against the original L/C. when the amount and restores the balance. This L/C is suitable when there is regular flow of trade activities between the importer and exporter.

8. Transferable L/C

A transferable L/C is one which contains an express provision that the benefits under it may be transferred either fully or partly to one or more parties. In our country, such L/C can be transferred only once and that too within the country.

9. Red Clause L/C

It is a special clause incorporated in red ink in the documentary credit, which authorised the negotiating bank of grant advances, on the receipt of full set of shipping documents. The exporter receives payments from his bank on the submission of shipping documents.

10. Back-to –Back L/C

It is a domestic L/C. it is an ancillary credit created by a bank based on a confirmed export L/C received by the direct exporters. The direct exporter keeps the original L/C with the negotiating or some other bank in India, as a security, and obtains another L/C in favour of domestic supplier. Through this route the domestic supplier gains direct access to a pre-shipment loan based on the receipt of domestic or back-to-back L/C.

11. Traveller‘s L/C

This type of L/C is issued to a person who plans to visit foreign countries. Up to the amount mentioned in L/C, the person can draw cheques which the banks will honour. It is of great convenience for the person because he can draw several cheques up to the amount mentioned in L/C.

COUNTERTRADE - TYPES

Countertrade is a reciprocal form of international trade in which goods or services for exchanged for other goods or services rather than for hard currency. This type of international Trade is more common in lesser-developed countries with limited foreign exchange or credit facilities.

Wikipedia "Countertrade means exchanging goods or service which are paid for, in whole or part, with other goods or services rather than with money. A monetary valuation can however be used in countertrade for accounting purposes. "

Countertrade takes place due to the following reasons:

Shortage of hard currency

Lack of credit

BOP problems

Low commodity prices - low export income Surplus capacity

Arms trade

Lack of a well-developed private sector

Lack of international trading experience

LDCs - low share of manufactured goods in international market

There are mainly eight types of countertrade:

1.Barter:

Barter system is the oldest form of exchange of goods for goods. In barter trade, there is exchange of products directly for other products without the use of money as means of payment. Generally, under barter exchange, principal commodities are exchange between two parties in two different countries. For example, oil can be exchanged for wheat or sulphuric acid for ammonia, and so on.

A "shadow price" is determined for both products to calculate the quantities of these to be traded. It is often a short-term contract to guard against currency exchange fluctuations.

2. Counter Purchase:

it is also called as parallel trading or parallel Barter. It invoices payment in cash.

In a counter purchase:

• The first contract is the original sales contract, outlining the terms in which an initial buyer purchases from an initial seller.

• The second parallel contract outlines the terms in which the original seller agrees to buy unrelated goods from the original buyer.

Basically, this is a contractually enforced relationship between two parties who agree, at some point, to provide business for one another.

Thus, countertrade involves 2 contracts, 2 sales, 2 deliveries of more or less equal amount.

3. Buyback:

It occurs when a firm builds a plant in a country -or supplies technology, equipment, training, or other services to the country and agrees to take a certain percentage of the plant's output as partial payment for the contract.

For example, an exporter of textile machinery agrees to buy a specified portion of the manufactured goods (cloth) as an incentive to the buyer.

4. Offset:

In an offset arrangement in which the seller assists in marketing products manufactured by the buying country or allows part of the exported product's assembly to be carried out by manufacturers in the buying country. This practice is common in aerospace, defense and certain infrastructure industries. For example: A Government' purchases expensive military equipment where the importing country reduces its cost by locally manufacturing or assembling part of the equipment. The local component (offset) is usually not more than 20 to 30% of the deal value.

5. Compensation Trade:

Compensation trade is a form of barter in which one of the transactions is partly in goods and partly in hard currency.

6. Cooperation Agreements:

It involves a triangular deal between three parties of three different countries. It is suitable for bulky and heavy goods. For example: An exporter from USA sells to a cash-strapped Eastern European country that delivers the bartered goods to a Western European one which, in turn, pays the US company.

7. Hybrid Countertrade:

It requires approval of foreign investment by a Government on the condition that all or most of the production ot the investing company is to be exported. In other words, approval of foreign investment is subject to export condition.

BENEFITS OF COUNTERTRADE

There are several benefits of Counter-Trade:

1. Entry in Difficult Markets:

Countertrade enables the entry in difficult markets. At times, there are sanctions imposed on certain countries by the United Nations due to various reasons. The barter trade of principal commodities is allowed on humanitarian grounds. Therefore, the consumers in the affected country (on whom sanctions are imposed) can get basic goods on account of barter trade approved by UN.

2. Overcomes Problem of Exchange Rate

Fluctuations: Countertrade overcomes the problem of exchange rate fluctuations. For instance, in cases like barter trade, the goods are exchanged for goods, which means the exchange is not determined in currency terms. Therefore, countertrade is not affected by exchange rate fluctuations.

3. Optimum Use of Production Capacity:

Countertrade enables firms or countries to make optimum use of production resources. This is because countertrade increases the demand for goods and services, which in turn results in more production, thereby making optimum use of production capacity.

4. Overcomes Foreign Exchange Reserves Problem:

Countertrade overcomes the problem of foreign exchange reserves problem. Since in certain cases, there is no outflow of foreign exchange, there is no effect on Balance of Payments position of country which is importing goods under countertrade.

5. Markets for Products in Decline Stage of PLC:

Countertrade may create markets for products which are in the decline stage of product life cycle. For instance, certain products become outdated in certain countries, especially in developed countries. Therefore, such products can be exported in less developed or backward countries, where there is demand for such goods.

6. Overcomes Credit Difficulties:

Generally, there is no need to provide credit facilities to the importers as goods are exchanged for goods. Therefore, countertrade helps to overcome credit difficulties such as chances of bad debts for the exporters.

7. Bilateral Ties Between Countries:

Countertrade may help to develop good bilateral relations between participating countries. At times, some countries drastically need basic goods as they are deprived of such goods on account of embargo or sanctions by UN. However, on humanitarian grounds UN may allow barter trade of principal commodities.

8. Allows Inputs at Lower Rates:

Countertrade facilitates the import of inputs at lower rates. Under certain cases of countertrade there is an agreement between two parties to transact business for the exchange of finished goods with that of inputs. As such the parties may agree to trade finished goods in exchange for inputs (raw materials or parts) at lower rates.

MEANING: Pre-shipment finance also popularly known as packing credit. It is an advance credit facility contained by an exporter from a bank or financial institution. The reserve bank of India defines it as “any loan to exporter for financing the purchase, processing, manufacturing or packing of goods‟. Precisely, it is an interim advance provided by a bank for helping the exporter to purchase, process, and pack and ship the goods. Packing credit is working capital extended to an exporter.

FEATURES OF PRE-SHIPMENT FINANCE

The salient features of packing credit are as follows

1. Eligibility-

Packing credit is granted to those exporters who have export order or a letter of credit in their name from the foreign buyer. An indirect exporter can also obtain packing credit if:

He produces a letter from concerned export house or other concerned party stating that a portion of the export has been allotted in this favour.

The export houses or other concerned party should also state that they don’t wish to obtain packing credit for the same.

2. Purpose-

Packing credit is provided to the exporter to meet working capital requirements before shipment of goods such as payment of raw material, payment of wages etc.

3. Documentary Evidence-

Pre-shipment finance is granted against the evidence of irrevocable L/C confirmed order for export. The document of L/C confirmed order must be deposited with the lending institution.

4. Form of Finance-

Packing credit can be either in the form of funded or non-funded advance. Red Clause/Green clause L/Cs are the forms of funded finance. Non-funded facilities include domestic L/Cs, back-to-back L/Cs and various guarantees.

5. Amount of Packing Credit-

The amount of packing credit depends on the amount of export order and credit rating of the exporters by the bank. The bank may also consider the export incentives receivable such as DBK, IPRS etc.

6. Period of Packing Credit-

It is normally granted for a period of 180 days. Further extension of 90 days is considered with the prior permission of RBI.

7. Rate of Interest-

Packing credit is provided at a concessional rate of interest. The difference in normal rate of interest and export finance rate of interest is reimbursed by RBI to banks.

8. Loan Agreement-

Before disbursement of loan, the banks require the exporter to execute a formal loan agreement.

9. Maintenance of Accounts-

As per RBI directives bank must maintain separate accounts in respect of each pre-shipment advance. However, running accounts are permitted in case of certain items produced in FTZs/EPZs and 100% EOUs.

10. Disbursement of loan-

Normally, pre-shipment finance advance not sanctioned in lump sum, but it is disbursed in a phased manner.

11. Monitoring The Use of Advance-

The bank advancing packing credit should monitor the use of pre-shipment finance by exporter i.e. whether the amount is used for export purpose or not penalty can be imposed for misuse.

12. Repayment-

The exporter is expected to liquidate or repay the amount of advance together with interest charge as soon as the export proceeds or incentives are realized.

MEANING: When an advance or a loan is needed by an Indian exporter after completing the process of shipment of goods, it is termed as “Post-shipment Finance”. This finance is needed after making the shipment and before realization of payment from overseas buyers. Post-shipment finance is provided to meet working capital requirements after the actual shipment of goods.

FEATURES

The main features of post-shipment finances are as follows-

1. Eligibility- This facility is available to the exporters who have actually shipped the goods or to an exporter in whose name the export documents are transferred.

2. Purpose- Post-shipment finance provides working capital to the exporter from the date of shipment to the date of realization of export proceeds.

3. Documentary Evidence- It is extended against the evidence of shipping documents indicating the compliance of actual shipment of goods or other necessary evidence in case of deemed and project exports.

4. Forms of Post-Shipment Finance- Banks provide post-shipment finance under different forms such as discounting of export bills, advance against goods sent on consignment basis, advance against retention money etc.

5. Amount of Post-Shipment Credit- The amount of post-shipment finance depends upon the working capital requirements of the exporter after shipment of goods.

6. Period of Post-Shipment Finance- Short term loan is provided by commercial banks usually for 90 day. EXIM bank provide medium term finance for a period between 90 day and 5 years and long term loan provided by EXIM bank in case of export of capital goods and turnkey projects for a period between 5 years and 12 years.

7. Rate of Interest- Post-shipment finance facility is granted at a concessional rate of interest, as compared to the rate of interest charged for domestic or local parties.

8. Loan Agreement- The exporter is required to execute a formal loan agreement with the bank before the amount of loan is actually disbursed.

9. Maintenance of Accounts- As per RBI directives, banks must maintain separate account in respect of each post-shipment advance. However, running accounts are permitted in case of units in SEZ/EPZ and 100% EOUs.

10. Disbursement of Loan Accounts- Normally, post-shipment credit advances are not given in lump sums. It is disbursed in instalments as and when required by the concerned exporter.

11. Monitoring the use of Advance- The bank advancing post-shipment credit should monitor, the use of post-shipment credit by the exporter i.e. whether the amount is used for export purpose or not. Penalty can be imposed for misuse.

Exporter obtain packing credit and post shipment credit to meet working capital needs. The procedure in export financing is as follows:

Application: The exporter must make an application in prescribed form to the bank. The application must be supported with relevant documents such as:

(A) In case of Packing Credit

An undertaking stating that the advance will be utilised for the specific purpose in respect of export of goods.

An undertaking stating that the shipment will be effected within a certain time limit and submit the relevant shipping documents to the bank in time.

Agreement of hypothecation or letter of pledge.

Demand pro-note signed on behalf of the company/firm.

Letter of continuity signed on behalf of the company/ firm.

Confirmed export order and/or LC in original.

Appropriate policy/ guarantee of ECGC.

Any other documents as required by the bank.

(B) In case of Post Shipment Credit

Shipping documents attested by custom authorities.

Demand pro-note signed on behalf of the company/firm.

Letter of continuity signed on behalf of the company/ firm.

Certificate of the Board of Directors resolution.

Letter of authority to operate the account.

(C) Processing of Application:

The application is processed taking into consideration the following:

Documentary evidence in the form of export order/LC (in the case of packing credit) and shipping document (in case of post-shipment) or correspondence exchanged between the applicant and the importer.

Credit worthiness of the applicant.

3. Sanctioning of Loan:

If the application is found in order, the bank sanctions the amount. Normally the loan is sanctioned depending upon FOB value of export order / LC or market value of the goods whichever is less.

4. Loan Agreement:

Before disbursement of loan, the banks require the exporter to execute a formal loan agreement. The loan agreement contains terms and conditions relating to the loan.

5. Loan Disbursement:

Normally, packing credit / post shipment advances are not sanctioned in lump-sum but are disbursed in a phased manner.

6. Maintenance of Accounts:

As per RBI directives, banks must maintain separate accounts in respect of each pre-shipment / post-shipment advance. However, running accounts are permitted in case of units in EPZ / SEZ and 100% EOUs.

7. Monitoring of Accounts:

The bank advancing packing credit/ post-shipment should monitor the use of packing credit by the exporter, i.e. whether the amount is used for export purpose or not.

8. Repayment:

As soon as the export proceeds and/ or incentives are received, the exporter should repay the amount to bank advancing credit. Normally the advancing bank realises the export proceeds and then makes necessary entries in the exporter's account.

BASIS FOR COMPARISON | PRE-SHIPMENT FINANCE | POST-SHIPMENT FINANCE |

Meaning | Pre-shipment finance is a facility of extending working capital finance, to the exporter of the goods, in order to export them in another country. | Post shipment finance is a form of the loan extended by the bank to the exporter against the shipment of goods which is already done. |

Objective | To help the exporters to procure raw material, labour, supplies, so as to produce, package, store and transport the goods. | To finance export receivables right from the date documents are submitted to the exporter's bank till the date of realization of proceeds from exported goods. |

Eligibility | Export company or company exporting goods through export houses. | Exporter himself or the person in whose name export documents are transferred. |

Source of Repayment | Proceeds from the contract | Proceeds from exports |

Risk involved | Payment and performance risk | Payment risk only |

Period | The period is upto 270 days before shipment of goods. | The period is upto 180 days after shipment of goods. |

Beneficiary | It is offered to Indian exporters/suppliers of export goods. | It is offered to Indian parties as well as to overseas buyers and agencies. |

Documentary evidence | Pre-shipment is provided against the documentary evidence of export order/LC. | Post-shipment is provided against the documentary evidence of shipping documents attested by customs. |

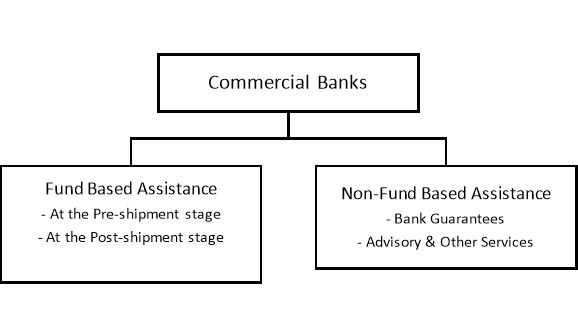

ROLE OF COMMERCIAL BANKS

A major part of export finance is provided by commercial banks. They also provide other facilities and services to the exporters. The functions of commercial banks can be grouped under two heads:

(A) Fund Based Assistance

(B) Non-Fund Based Assistance.

The assistance provided by commercial banks in respect of export finance can be charted as follows:

|

(A) Fund Based Facilities:

The commercial banks provide fund based activities at

(i) Pre-shipment Stage and

(ii) Post-Shipment Stage.

(i) At the pre-shipment stage: The commercial banks provide finance on short terms basis for a normal period of 180 days at a very concessional rate of interest. The various forms of advance are:

Cash packing credit loan

Advance against hypothecation

Advance against pledge, etc.

(ii) At the post-shipment stage: The commercial banks provide finance at the post-shipment stage normally for a period of 90 days at a concessional rate of interest. The various forms of post-shipment finance are:

Negotiation of Bills drawn under LC

Purchase / Discounting of Bills

Overdraft against bills under collection, etc.

(B) Non-Fund Based Assistance:

(i) Bank Guarantees:

RBI has authorised commercial banks to issue guarantees and furnish bid bonds in favour of overseas buyer. Prior permission of RBI is not required except in case of exports of capital goods under deferred payments, construction contracts, consultancy and technical services contracts and turnkey projects. Their various guarantees issued by banks are:

Guarantee for foreign currency loans sanctioned by a financial institution abroad to Indian exporters who raise funds to finance their projects abroad.

Performance guarantee which is generally required in export of capital goods and also in case of turnkey and construction projects.

Banks issue a guarantee for payment of retention money by the overseas party who would release the retention money to the Indian party only after receiving guarantee from bank.

The banks also issue advance payment guarantee to the overseas buyer who normally makes certain advance payment to the Indian exporter against a bank guarantee.

Banks issue bid bonds so as to enable exporters to participate in various global tenders.

(ii) Other services:

They collect export proceeds from the importer and credit the same to exporter’s account.

The bank assists the exporter in the collection of useful information of the credit worthiness of the foreign buyer through their foreign agents/branches.

The banks issue bank drafts is case of payment of freight charges and such other charges.

EXIM BANK

The Export Import Bank of India came into existence in 1982. it has its headquarters at Mumbai and branches and offices in important cities in India and abroad.

The EXIM bank of India is a public sector financial institution established on 1st January, 1982. It started operating from 1st march, 1982. It was established by an Act of Parliament, for the purpose of financing, facilitating and promoting foreign trade. It is also the principal financial institution for coordinating the working of institutions engaged in financing India’s foreign trade. This bank was mainly created for the purpose of financing medium and long

term loans to exporters there by promoting the country’s foreign trade.

The assistance provided by Exim Bank to the exporters can be grouped under two heads:

A) Fund Based Assistance

B) Non-Fund Based Assistance.

The various assistant provided by Exim Bank can be charted as follows:

OBJECTIVES OF EXIM BANK

The main objectives and purposes of EXIM bank are as follows

Financing of export and imports of goods and services not only of India but also of third world countries.

Financing of joint ventures in foreign countries.

Financing of Indian manufactured goods, consultancy and technological services of deferred payment terms.

Financing R&D and techno-economic study.

Co-financing global and regional development agencies.

ROLE OF SIDBI

Small Industries Development Bank of India (SIDBI), was set up on April 2, 1990 under an Act of Indian Parliament. Presently it acts as the Principal Financial Institution for the Promotion, Financing and Development of the Micro, Small and Medium Enterprise (MSME) sector and also co-ordinates the functions of the institutions engaged in similar activities.

SIDBI has its head office in Lucknow (UP) and has a network of 15 regional offices and about 31 branch offices in India.

FUNCTIONS OF SIDBI

SIDBI provides various schemes for the promotion, finance and development of units in the micro and small enterprises sector. Some of the schemes are broadly classified into three groups:

I. REFINANCE ASSISTANCE

1. Seed Capital Scheme:

SFCS / SIDCs provide seed capital to promoters of SSI units The SFC / SIDC can then obtain refinance from SIDBI. The scheme enables the entrepreneurs to meet promoters contribution towards equity.

2. Equipment Refinance Scheme:

SFCs/SIDCs provide equipment refinance to SSI units to purchase equipment for the purpose of expansion and modernisation. The SFC/ SIDC can then obtain refinance from SIDBI, if so required.

3. Tourism Related Finance Scheme:

SFCS / SIDCs provide finance to entrepreneurs tor setting up tourism related activities, such as development of amusement parks, cultural centres, restaurants, etc. The SFC / SIDC can then obtain refinance from SIDBI.

II. SCHEMES OF DIRECT ASSISTANCE

4. Project Finance Scheme:

SIDBI provides direct finance to SSI units for setting up new projects. Preference is given to those units with export orientation, import substitution, hi-tech and those promoted by entrepreneurs with good track record.

The project cost should not be less than 75 lakh and the debt equity ratio not to exceed 2:1.

5. ISO 9000 Scheme:

SIDBI provides direct finance to obtain ISO 9000 certification The objective is to promote quality systems in SSI units, with a view to strengthen their marketing and export capabilities. This scheme enables the SSI unit to meet the expenses on consultancy, documentation, audit, certification fee, equipment and calibrating instruments required for obtaining 1S0 900 certification.

6. Equipment Finance Scheme:

SIDBI provides direct finance to SSI units for the purchase of equipment, required for the purpose of expansion and modernisation.

7

III. BLLS SCHEMES

7. Direct Discounting Scheme (DDS): SIDBI directly discounts the bills drawn by MSEs.

The DDS is of two types:

(a) DDS (Equipment)-where bills are normally of 5 years and minimum transaction value 1 lakh.

(b) DDS (Components) -where unexpired period is not more than 90 days.

8. Bills Rediscounting Scheme (BRS):

SIDBI also rediscounts the bills that were earlier discounted by commercial banks. There are too types of BRS:

(a) BRS (Equipment) - where the usance of bills is normally 5 years.

(b) BRS (Short Term)-where the unexpired usance is not more than 90 days.

ECGC

In order to provide export credit and insurance support to Indian exporters, the GOI has set up the Export Risks Insurance Corporation(ERIC) in July, 1957. It is now known as Export Credit Guarantee Corporation (ECGC) of India limited.

ECGC is a company wholly owned by the GOI. It functions under the administrative control of the Ministry of Commerce and is managed by board of directors representing Government, Banking, Insurance, Trade and Industry.

OBJECTIVES The main objectives of ECGC are as follows

1. ECGC is designed to protect exporters from the consequences of payment risks both political and commercial.

2. It helps exporters to expand their overseas business without fear of loss.

3. It enables exporters to get timely and liberal/bank finance.

4. It provides to banks financial guarantees to safe guard their interests.

5. It enables exporters and importers to take calculated risks in business.

Covers issued by ECGC

The covers issued by ECGC can be divided broadly into four groups:

A. Standard policies- issued to exporters to protect them against payment risk involved in exports on short term credit.

B. Specific policies - designed to protect Indian firms against payment risk involved in (i) exports on deferred terms of payment (ii) services rendered to foreign parties and (iii) construction works and turnkey projects undertaken abroad.

C. Financial guarantees - issue to banks in India to protect them from risk of loss involved in their extending financial support to exporters at Pre-shipment and post-shipment stages.

D. Special Schemes such as Transfer Guarantee meant to protect banks which add confirmation to letter of credit opened by foreign banks, Insurance cover for Buyer's Credit, etc.

References

- Export Marketing Imperative by Michael R. Czinkota

- International Marketing and Export Management by Edwin Duerr, Gerald Albaum