Unit-II

Profits prior to Incorporation

From time to time, companies are made to buy a particular running or going concern. A company is born only after its registration, that is, its establishment. A company can only make a profit after it is founded, but not before it is founded. In many cases, the acquisition date of a business may not coincide with the establishment date.

For example, a company founded on May 1, 2004 may purchase a business from January 1, 2004, which is the start date of the fiscal year. In general, a going concern assumption is purchased based on the idea of the last record

It's more convenient for both-sellers, and therefore sellers. If you want to buy a business on a date other than the balance sheet date, you need to acquire and validate accounts such as stocks, assets, and liabilities. The process is a tedious task. To avoid this tedious task, you can also buy a business from the day the company creates its last final account.

Private companies can start their business immediately after they are established, but public companies can only start their business after obtaining a business start certificate. In other words, all profits earned before the establishment of a corporation in the case of a private company and before the start of a business in the case of a public company should be regarded as capital gains. However, keep in mind that the pre-establishment profit and loss calculation takes into account the date of establishment, not the date of business start.

For example, a company founded on January 4, 2004 agrees to require a business that has been running since January 1, 2004. The account will be closed on December 31st. The company is entitled to receive profits or losses from January 4, 2004 to December 31, 2004, as well as profits or losses from January 1, 2004 to 31.3.2004. The profits earned before incorporation, that is, from January 1, 2004 to 31.3.2004, are understood as pre-incorporation profits. This is not considered a profit, but it is a capital profit.

Such profits may be transferred to capital reserves or used to assess financial losses. If a loss occurs during the pre-establishment period, the loss must be debited to the goodwill account. The profits earned during the post period, that is, between January 4, 2004 and December 31, 2004 in the above example, are profits and profits that can be used for dividends.

Allocation of "profit / loss" to pre-establishment and post-establishment periods:

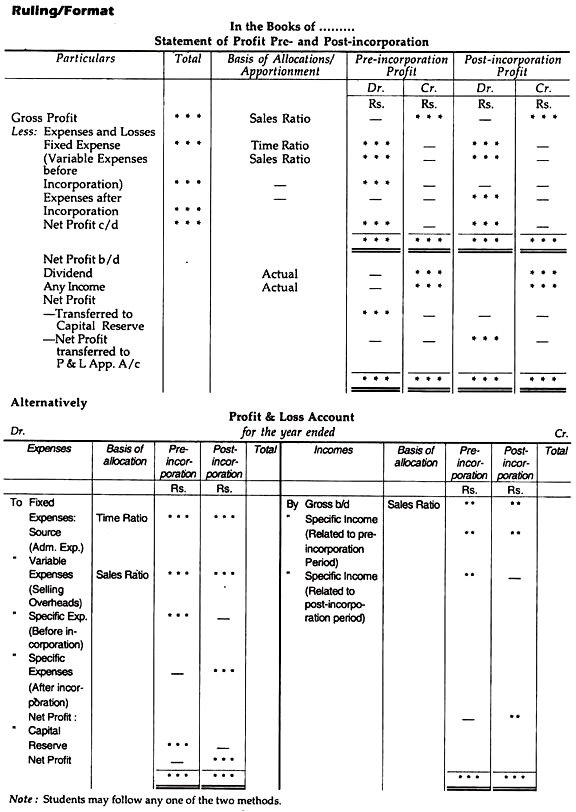

Pre-incorporated profits cannot be used for dividends and must be separated from divisible profits. This is possible if the income statement is prepared separately for the pre-establishment period and the post-establishment period. And this is only possible by closing the books and inventory for the two periods. These are tedious tasks. Therefore, profits or losses are estimated by allocating on a time, sales, impartial or practical reasonable basis.

In practice, an equivalent set of books is maintained throughout the fiscal year.

The P & L account is ready at the beginning of the year, after which profits or losses are allocated between the two periods.

- From the date of purchase to the date of establishment (pre-establishment period) and

- From the date of establishment to the end of the fiscal year (period after establishment).

Accounting method:

To find profits or losses before and after establishment:

1. We will have one trading account for the entire period. Do not consider the date of establishment. Therefore, you will receive one number of gross margins for the entire period.

2. Gross profit margin is distributed between two periods, pre-establishment and post-establishment, based on the concept of sales within the two periods.

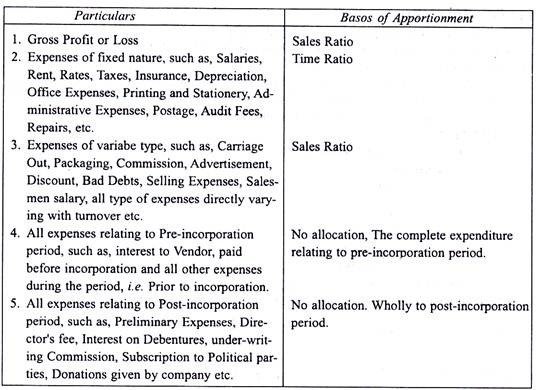

The various costs shown on the income statement should be divided into pre-establishment and post-establishment periods on a logical and appropriate basis.

Sales ratio:

In a simple matter where sales are evenly distributed over the entire period, sales are distributed between pre-establishment and post-establishment periods at a rate of that period. However, in many cases sales fluctuate from time to time. Therefore, the sales ratio is recognized based on the concept of each sale, taking into account the pre-establishment and post-establishment periods. (Sales and time basis.)

Handling of pre-establishment results:

Profit or loss from the date of purchase of the business to the date of establishment belongs to the company. Such profits should not be considered transaction profits. Pre-establishment profits are treated as capital gains and cannot be distributed as dividends to the shareholders of the purchasing company.

The income statement is prepared at the end of the year and then the profit and loss are allocated between the two periods.

(I) from the date of purchase to the date of establishment (pre-establishment period) and

(II) From the date of establishment to the end of the fiscal year (period after establishment).

Accounting method:

To find profits or losses before and after establishment:

1. Set up one trading account for the entire period. Do not consider the date of establishment. Therefore, you will reach one figure of gross profit for the entire period.

2. Gross profit is distributed to two periods, pre-establishment and post-establishment, based on sales in the two periods.

3. The various costs shown on the income statement should be divided into pre-establishment and post-establishment periods on a logical and appropriate basis.

They are shown below.

Sales ratio:

In a simple matter where sales are evenly distributed over the entire period, sales are distributed between pre-establishment and post-establishment periods at a rate of that period. However, in many cases sales fluctuate from time to time. Therefore, the sales ratio is calculated based on each sale, taking into account the pre-establishment and post-establishment periods. (Sales and time basis.)

Handling of pre-establishment results:

Gains and losses from the date of purchase of the business to the date of establishment belong to the company. Such profits should not be considered transaction profits. Pre-establishment profits are treated as capital gains and cannot be distributed as dividends to the shareholders of the purchasing company.

The handling of the results before the establishment is as follows.

(A) Profit before establishment:

1. Profit has the nature of capital gains.

2. Do not use capital gains to pay dividends.

3. Can be used to evaluate goodwill or capital loss.

4. The unused portion of profit can be transferred to capital reserve.

(B) Loss before establishment:

1. You can treat it as goodwill and add it to your goodwill account.

2. It may also be treated as a deferred revenue expense and amortized on profits over the years.

3. The special account (loss before establishment of corporation) may be debited.

Key takeaways:

- Incorporation is a way for a business to be formally organized and formally established.

- The process of establishment involves creating a document called the Articles of Incorporation and listing the shareholders of the company.

- In a company, the assets and cash flows of an entity are separated from the assets and cash flows of the owner and investor, which is called limited liability.

- Profit or loss from the date of purchase of the business to the date of establishment belongs to the company.

- Pre-incorporated profits cannot be used for dividends and must be separated from divisible profits.

Preparation of separate, combined and columnar Profit and Loss Account including different basis of allocation of expenses/ incomes

The article below details how to calculate your pre-establishment profit and loss.

1. Introduction of profit / loss before establishment

2. Calculation method of profit / loss before establishment

3. Accounting method

4. Accounting treatment

Pre-establishment profit / loss summary:

If you take over the business from a date before the establishment / start, the profits earned by the establishment / start date (established for a private company, started for a public company) are called “Profit before establishment”

The same is treated as capital gains, as these are the profits earned before the company was founded. In short, profits earned after the date of purchase of a business are called "profit after incorporation or acquisition", and profits earned before the date of purchase of a business are called "profit before incorporation".

For example, X Ltd. Was founded on April 1, 2006, acquired the operating business Y Ltd. From January 1, 2006, and closed its account on December 31, 2006. Currently X Ltd. Is Y Ltd from April 1st to December 31st, 2006, Y Ltd. From January 1, 2006 to March 31, 2006, as well as profits / losses due to Profit / loss .

Therefore, profits and losses generated before establishment are called "profit (loss) before establishment", are treated as capital gains, and cannot be distributed as business profits. Therefore, it cannot be distributed as a dividend.

The same can be transferred to capital reserves or adjusted for goodwill. "Pre-establishment loss" is treated as a capital loss, so the same thing appears under the "Other Expenditures" heading on the asset side of the balance sheet.

How to calculate profit / loss before establishment:

You need to prepare an income statement on the date of establishment to confirm the profit before the establishment. But in reality, the same books are maintained throughout the fiscal year.

The income statement is prepared at the end of the year, after which profits (or losses) are allocated between the two periods.

- From the date of purchase to the date of establishment or the period before establishment.

- From the date of establishment to the end of the fiscal year or the period after establishment.

Accounting method for profit and loss before establishment:

Procedures may be suggested to identify profits or losses prior to establishment.

Step I:

In order to calculate the gross profit amount, you must first create a trading account for the entire term, from the purchase date to the last account date.

Step II:

Calculate the following two ratios.

- Sales ratio Sales must be calculated for the pre-establishment and post-establishment periods.

- Time ratio: It is calculated considering the period. That is, you need to calculate the period from the date of purchase to the date of establishment and the period from the date of establishment to the date of presentation of the final account.

Step III:

You need to make a statement to calculate the net income before and after the establishment individually based on the following principles.

- Gross profit must be allocated to the two periods based on the sales ratio that represents the gross profit for the two separate periods. Before and after incorporation of company.

- Fixed or time-based costs, such as rent, salary, depreciation, and interest, must be allocated in two periods based on a time ratio.

- Variable or sales-related expenses must be distributed over two periods based on the sales ratio.

- Certain costs, such as partner salaries, director salaries, reserves, and corporate bond interest, are not allocated as they are related to a particular period. For example, partner salaries are billed for pre-acquisition profits, and director compensation, corporate bond interest, etc. are billed for post-acquisition profits.

List of Expenses: Assigned based on sales / sales:

(A) Gross profit

(B) Selling expenses

(C) Advertising

(D) Outward transportation

(E) Warehouse rent

(F) Discounts are allowed

(G) Salesman salary

(H) Commission to salesman

(I) Sales promotion expenses

(J) Distribution cost (variable part)

(K) Free sample provided

(L) Costs for after-sales service, etc.

(M) The cost of the delivery van.

List of Expenses: Allotted based on time:

(A) Administrative and administrative expenses

(B) Salary to office staff

(C) Rent, charges, taxes

(D) Depreciation of fixed assets

(E) Printing and stationery

(F) Insurance

(G) Audit fee

(H) Miscellaneous expenses

(I) Distribution costs (fixed part)

(J) Travel expenses (general)

(K) Interest on corporate bonds

(L) General expenses

List of Expenses: Allotted based on time:

(A) Administrative and administrative expenses

(B) Selling expenses

(C) Advertising

(D) Outward transportation

(E) Warehouse rent

(F) Insurance

(G) Audit fee

(H) Miscellaneous expenses

(I) Distribution costs (fixed part)

(J) Travel expenses (general)

(K) Interest on corporate bonds

(L) General expenses

(M)Fixed costs in nature.

Pre-establishment profit / loss application / accounting:

(A) Profit before establishment:

Since "pre-establishment profit" is a capital gain, the same must be amortized for:

- Reserve expense account

- Formation cost account

- Clearing expense account

- If the fixed asset is worth it, write it down

- Goodwill account

- If there is a balance, it will be transferred to the capital reserve.

(B) Loss before establishment:

The same is adjusted because "pre-establishment loss" is a capital loss.

- Capital gains

- Debit the goodwill account

- Depreciation of fictitious assets

- Capital reserve.

Figure 1:

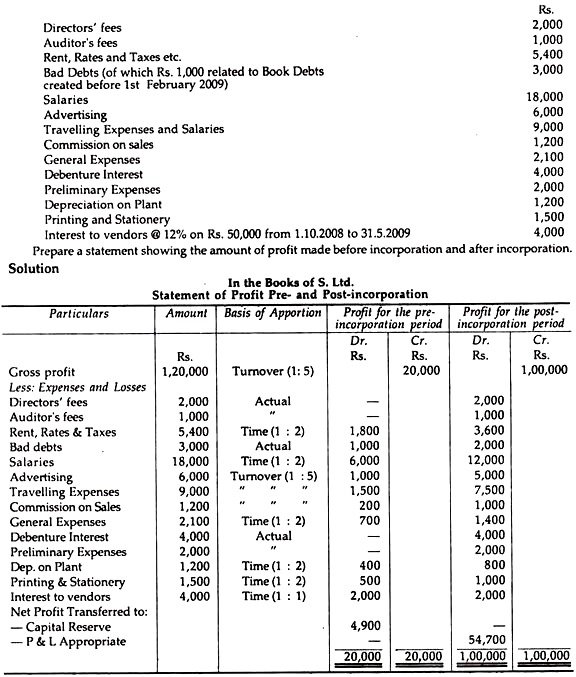

Problem 1:

S. Ltd was registered on January 1, 2000 to acquire the business of M / s P. Ltd. On October 1, 2008, and has a certificate of start of business on February 1, 2009. I got.

The company's accounting for the period ended September 30, 2009 disclosed the following facts:

- Sales for the entire period reached rupees. 3,000,000 rupees 50,000 related to the period from October 1, 2008 to February 1, 2009.

- The trading account showed gross profit of Rs. 1, 20,000.

- The following items are displayed in the income statement.

Note:

1. Sales-related costs are allocated based on sales (that is, 1: 5).

2. Other costs will be allocated based on time only (i.e. 1: 2).

3. From the profit before establishment, you can also charge a reserve cost for the capital reserve.

Problem 2:

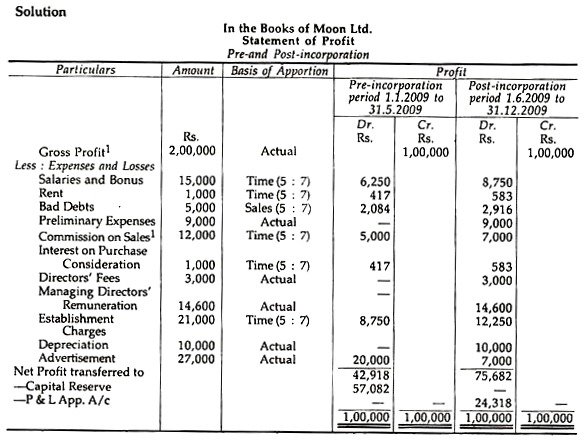

Moon Ltd was established on June 1, 2009. He has taken over the business of N, which is the ownership of Rs, from January 1, 2009. All profits earned after January 1, 2009 are 100,000, provided they belong to the company. The following is the income statement data for the year ended December 31, 2009.

Gross profit Rs. 2,00,000; salary and bonus Rs. 15,000; Rent Rs. 1,000; Bad debt Rs. 5,000; Reserve Rs. 9,000; Committee of Sales Rs. 12,000; Interest paid on or against the purchase price Rs. 1,000; Board membership fee Rs. 3,000; Managing Director Reward Rs. 14,600; Establishment cost Rs. 21,000; Depreciation Rs. 10,000; and advertising Rs. 27,000.

(A) Sales for the first 6 months were rupees. 10, 00,000; Gross profit margin is 12% of sales. Gross profit margin was 8% in the second half. The sales commission was 6% throughout the year. Inventory and work in process issues do not occur in business.

(B) Until March 1, 2009, N was operating on its premises with only cash sales and no depreciable assets.

(C) The ads for the first 6 months were at Rs rates. 4,000 per month.

Create pre-incorporation and post-incorporation period profit accounts in a column format that provides the basis for separation for each item. How much was the profit before the establishment? It takes calendar months of the same length limit to the given data only.

How it works:

Therefore, the profit before the establishment reached rupees. 57,082. Gross profit reached rupees 2, 00,000 or 12 months. Profit for the first 6 months reached rupees. At 1,20,000 (Rs. 10,00,000 x 12/100), the profit for the next 6 months remains, that is, Rs. 80,000 (Rs. 2,00,000 – Rs. 1,20,000) is 8% of sales. Sales Rs for the next 6 month, assume 10, 00,000 (Rs. 80,000 x 100/8), sales evenly distributed by month. The sales ratio for the two periods is 5: 7. Sales commissions will be allocated accordingly.

Problem 3:

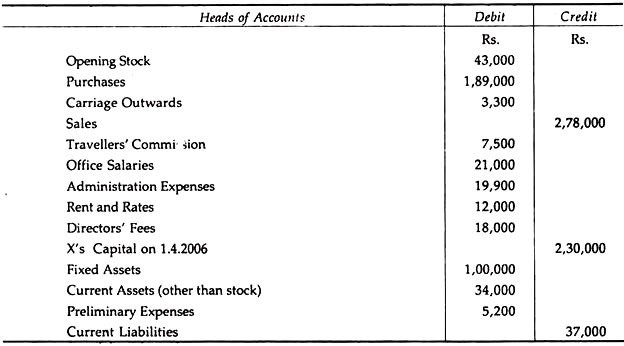

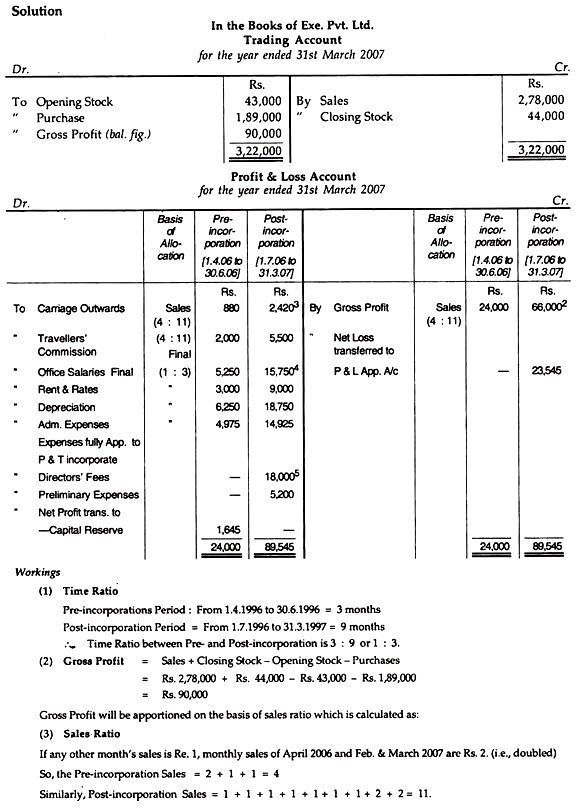

Mr. X founded a limited company under the name and style of Exe. Pvt. It will take over the existing business from April 1, 2006, but was not established until January 7, 2006. There was no mention of the business transfer in the books that continued until March 31, 2007.

As of March 31, 2007, the following balances have been extracted from the books.

You too:

(A) Shares on March 31, 2007 reached Rupees. 44,000.

(B) The gross profit margin is constant, and monthly sales in April 2006, February 2007, and March 2007 are twice the average monthly sales for the year.

(C) It was agreed that the purchase price would be met by the issuance of shares of Rs 3,000. 100 each

(D) Reserve costs are amortized.

(E) Outbound shipping and traveller fees must be assumed to change in direct proportion to sales.

You need to prepare a trading account and a profit and loss account for the fiscal year ending March 31, 2007, to allocate the profit and loss for the period before and after the establishment. Depreciation shall be provided at an annual rate of 25% about fixed assets.

Following information is given:

(A) Shares on March 31, 2007 reached Rupees. 44,000.

(B) The gross profit margin is constant, and monthly sales in April 2006, February 2007, and March 2007 are twice the average monthly sales for the year.

(C) It was agreed that the purchase price would be met by the issuance of shares of Rs 3,000 100 each.

(D) Reserve costs are amortized.

(E) Outbound shipping and traveller fees must be assumed to change in direct proportion to sales.

You need to prepare a trading account and a profit and loss account for the fiscal year ending March 31, 2007, to allocate the profit and loss for the period before and after the establishment. Depreciation shall be provided at an annual rate of 25% about fixed assets.

Therefore, the sales ratio before and after establishment is 4:11

(4) Outward transportation and Travellers’ Com. = Sales ratio, that is, 4:11.

(5) Other time-based costs:

Salary; Administration costs; Rent, fees, depreciation costs (Rs. 25,000, or Rs. 1, 00,000 x 25/100)

(6) The remaining costs will be charged for the profit after the acquisition.

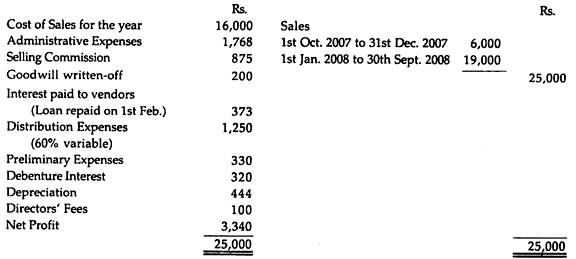

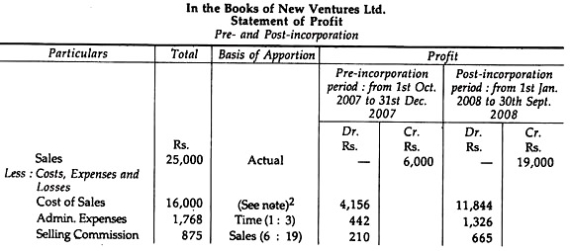

Problem 4:

New Ventures Ltd. Was founded on January 1, 2008 and has authorized capital of Rs 5,000. R. Bros since October 1, 2007 10 each to take over the operating business of Bros. The following is a summary of the income statement for the fiscal year ended September 30, 2008.

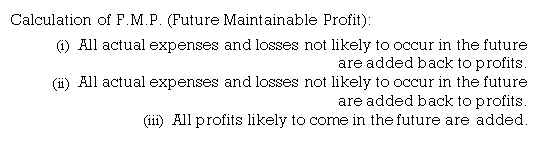

The company handles one type of product. When compared to the pre-establishment period, the unit sales price for the post-establishment period decreased by 10%. Between the pre-establishment and post-establishment periods, the amount of net income that provides the basis for the apportionment must be apportioned.

Income statement before and after establishment

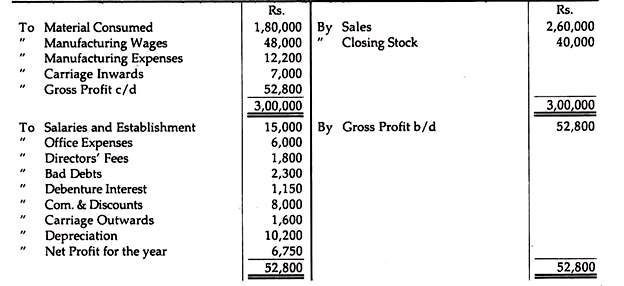

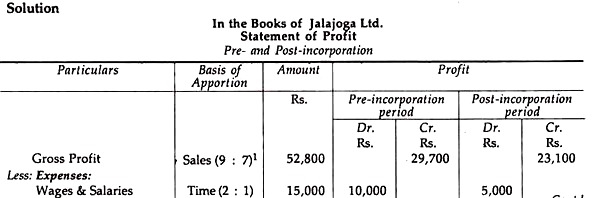

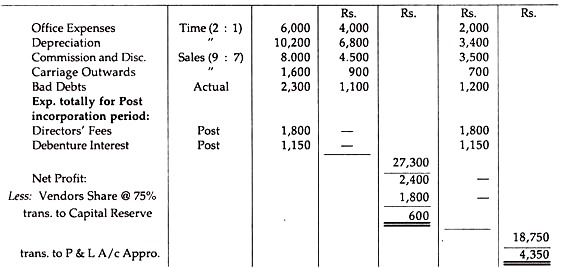

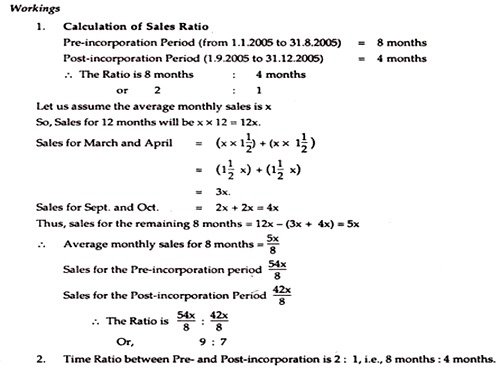

Problem 5:

Jalajga Ltd. Was established as a privately held company on March 1, 1995 to take over the business as a going concern from January 1, 2005. Vendors will receive 75% of the profits earned before March 1, 2015. The trading and P & L accounts for the year ended December 31, 2015 are as follows:

Sales in March and April are 1.5 times higher, with average monthly sales. Sales in September and October are twice the average monthly sales. Bad debt of 1,110 rs cases were amortized in June. Make statements showing pre- and post-establishment benefits. It also indicates the disposal of such profits.

To sum up:

(A) Gross profit must be distributed between pre-establishment and post-establishment periods based on the ratio of sales. If you're not given gross profit, you can do the same by creating a trading account.

(B) It is necessary to calculate the time ratio between the period before establishment and the period after establishment. Fixed costs are usually allocated based on a time ratio. Rent, taxes, insurance, depreciation, interest, salaries to clerical staff, etc.

(C) The ratio of sales must be known before and after the establishment, and selling, or variable costs are usually allocated based on the ratio of sales. Advertising, warehousing rent, storage and discount permits, freight costs, salesman salaries and commissions, etc.

(D) The costs excluding the period after establishment are as follows.

- Board membership fees, corporate bond interest, reserve funds, tax reserves, dividend proposals, etc.

(E) The costs excluding the period before establishment are as follows.

- Interest on the partner's capital, partner salary, etc.

(F) Expenses related to both pre-establishment and post-establishment must be billed for both periods on an hourly basis. Audit fees, interest paid to vendors, etc.

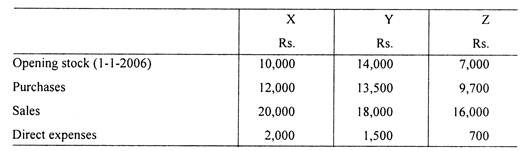

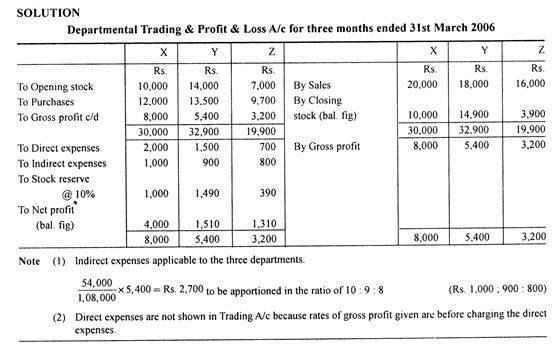

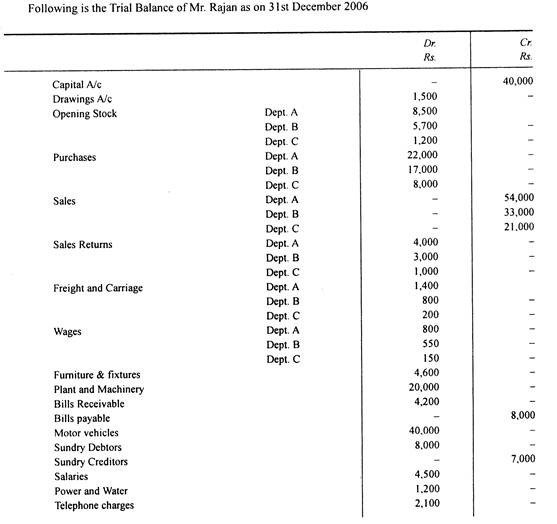

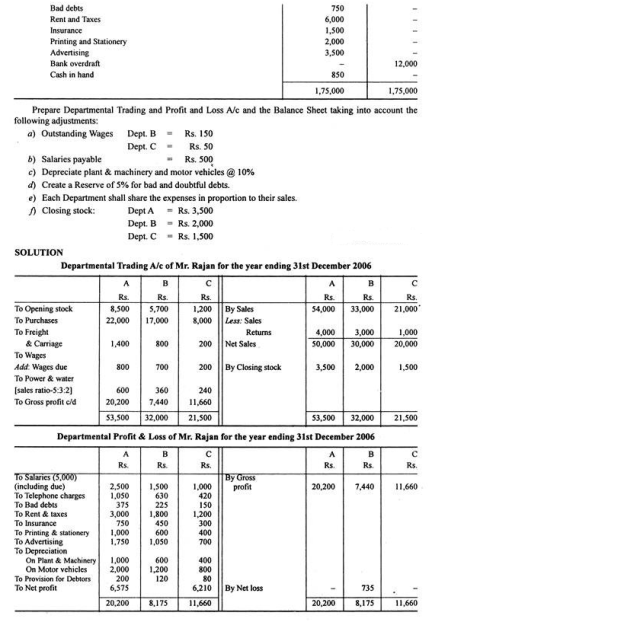

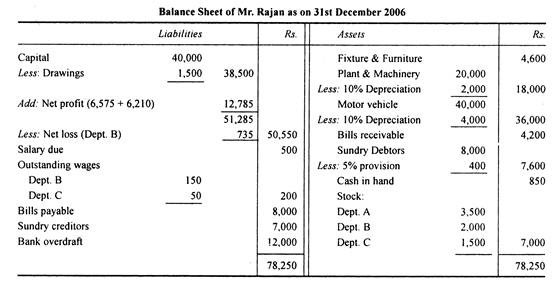

Problem 6:

The owners of a major retailer wanted to see the net income of the X, Y, and Z divisions individually for the three months ended March 31, 2006. It is not realistic to actually acquire the shares on that day, but the proper system accounting of the department is used, and the normal gross profit margin of the three departments involved is the sales before the direct cost is charged at 40%, 30%, and 20% respectively. Overhead is billed in proportion to the department's sales.

Below are the numbers for the department.

The total overhead costs during the period (including those related to other departments) were rupees. The total sale of Rs is 5,400 1, 08,000. Create a statement showing approximate net income with a 10% stock reserve for each sector against the March 31, 2006 estimate

Problem 7:

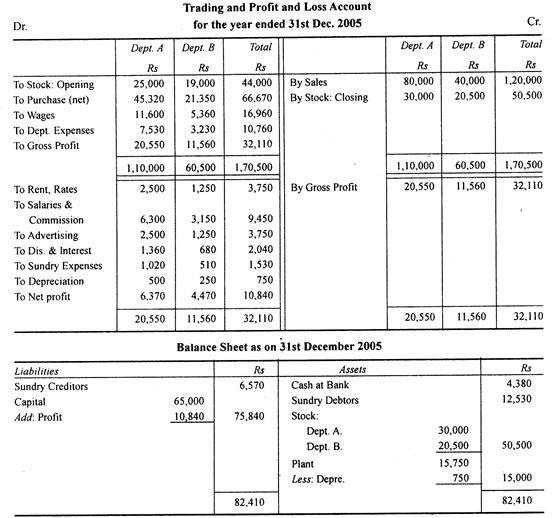

From the details below, you need to prepare a trading and P & L account for the year ended December 31, 2005, showing the gross and net income of each sector. Allocate general business expenses based on sales. You will also create a balance sheet. Stock in-hand inventory on December 31, 2005 Division A Rs 30.000 and B Rs 20,500.

The total sales are 1.20.000 rupees, that is, department A is 80.000 rupees and B is 40.000 rupees. Percentage of general or indirect expenses charged to A2 / 3 and B1 / 3. (B.Com. Madurai. MS. Bharathiar)

Solution:

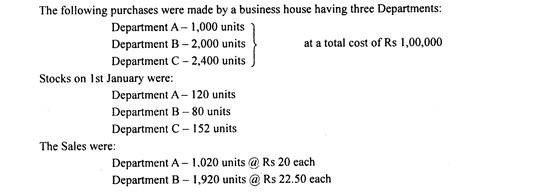

Problem 8:

Department C – 2,496 units @ 25 rupees each

The gross profit margin is the same in both cases. Set up a department trading account.

Solution:

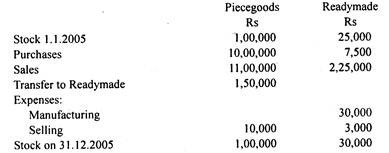

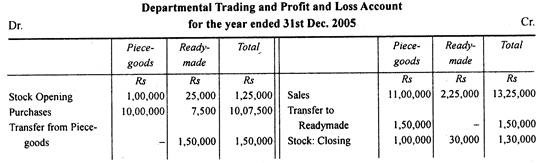

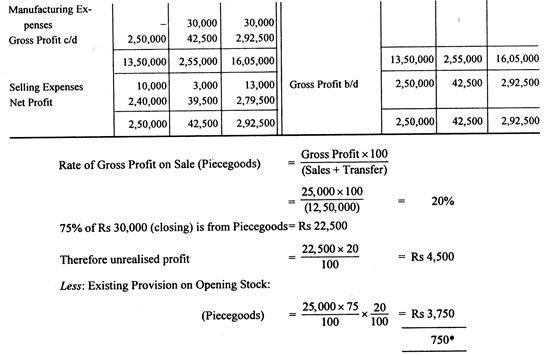

Problem 9:

The company has two divisions: piece goods and ready-made dresses. All merchandise purchased by the ready-made department from the Peace Merchandise Department will be billed at normal selling prices.

From the details below, create a departmental transaction and income statement for the year ended December 31, 2005.

Peace goods and ready-made

The ready-made department inventory is considered to consist of 75% cloth supplied by the Peace Goods department. And 25% cost and cloth from the outside. The Peace Goods division made gross profits in 2004 at the same rate as in 2005. The general cost of the entire business in 2005 was Rs 45,000.

Solution:

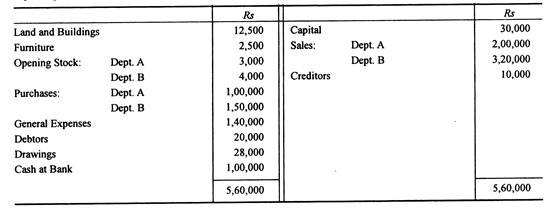

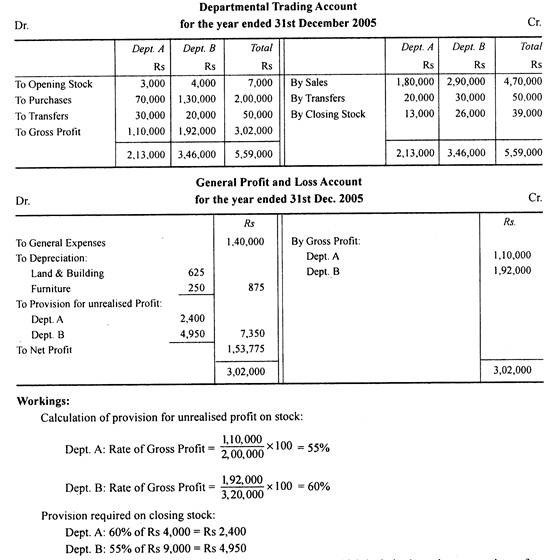

Problem 10:

From the following balances extracted from the company's books, create a department transaction and general profit and loss account for the year ended December 31, 2005, and a balance sheet for that day after adjusting for unrealized department profits.

Additional Information:

1. Close inventory in department A – Rs 13,000 including Rs 4,000 products at costs from department B to department A.

2. Final inventory of department B – Rs26,000-Includes goods from department AR 9,000 to department B.

3. Sales department A includes the transfer of goods worth 20,000 rupees to department B, and sales of department B include the transfer of goods worth 30,000 rupees to department A at the market price included.

4. The starting inventory of department A and department B includes goods from department B and department A worth Rs 1,000 and Rs 1,500 respectively at cost to the transfer department.

5. Depreciate land and buildings by 5% and depreciate furniture by 10% annually.

Solution:

No adjustment of opening inventory, including N.B. Inter-departmental transfers, is required. This is because the goods are valued at cost to the transfer department rather than the transferee department.

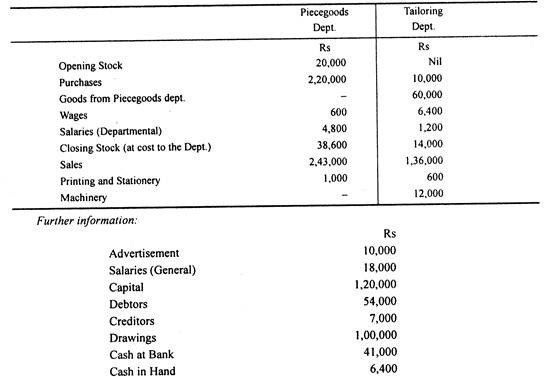

Problem 11:

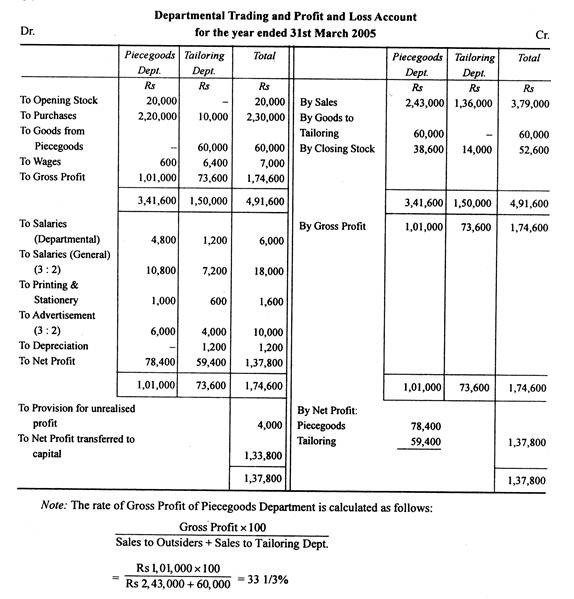

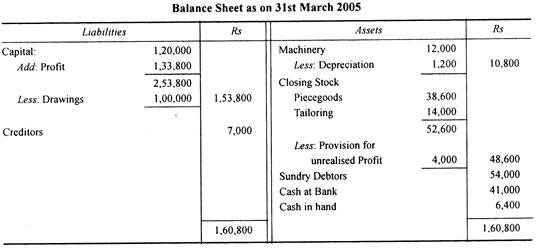

The company has two departments. Peace goods and tailoring. All merchandise purchased by the tailoring department from the piece goods department will be sold at the same normal market price as the price charged to external customers.

From the details below, create a department transaction and income statement and balance sheet as of March 31, 2005.

Depreciate the machine by 10%. Typical unallocated costs are allocated in a ratio of piece merchandise-3 to tailoring-2.

Solution:

Calculation of reserve for unrealized gains:

The composition of the tailoring department's closing stock is not shown. The tailoring department owns a stake of Rs 14,000. There is no doubt that the inventory consists of piece products and external products. You can assume that your inventory consists of both piece goods and external types of goods.

Therefore, the value of the goods in the piece merchandise department in the final inventory of the tailoring department can be calculated as follows:

Problem 12:

Note: All costs will be split by sales ratio as instructed.

Note: All costs will be split by sales ratio as instructed.

Sales ratio = A – Rs. 50.000, B – Rupee 30,000 C – Rupee 20,000 or 5: 3: 2

Key takeaways:

- The income statement is a financial statement that summarizes the income, costs, and expenses incurred over a specified period of time.

- The income statement, along with the balance sheet and cash flow statement, is one of three financial statements issued quarterly and annually by all public companies.

- It is important to compare the income statements for different accounting periods, as revenue, operating costs, R & D costs, and net income over time are more meaningful than the numbers themselves.

- The income statement, along with the balance sheet and cash flow statement, provides details of the company's financial performance.

- The income statement is one of the three main financial statements (along with the balance sheet and cash flow statement) that report a company's financial performance for a particular accounting period.

- Net Income = (Gross Income + Profit) – (Total Cost + Loss)

- Total revenue is the sum of operating revenue and non-operating revenue, and total costs include costs incurred by primary and secondary activities.

- Income is not a receipt. Revenue is earned and reported to the income statement. Receipts (receipt or payment of cash) are not.

- The income statement provides valuable insights into a company's operations, operational efficiency, poorly performing sectors, and performance compared to its peers.

Provisions Relating to Financial Statements as Per the Companies Act, 2013

- Section 129 of the Companies Act 2013 provides for the preparation of financial statements.

- 2.2 (40) includes the Balance Sheet, Income Statement / Income Statement, Cash Flow Statement, Statement of changes in Shareholders' Equity, and the description attached above.

- The new section 129 corresponds to the existing section 210. The financial statements shall provide a true and fair view of the company's situation and shall comply with the accounting standards notified in the new Section 133.

- It is also stipulated that the Financial Statements will be prepared in the format specified in the new Schedule III of the Companies Act 2013.

- Note that the new Schedule III provides Balance Sheet preparation and income statement provisions in the same row as the existing Schedule VI.

- In addition, the new Schedule III mandates the consolidation of subsidiary accounts in Section 129, which gives detailed instructions on the preparation of consolidated financial statements.

- Note that for the first time in new section 129 (3), a provision was created that if a company has one or more subsidiaries, the consolidated financial statements of the company and all of its subsidiaries must be prepared. In the format provided in the new Schedule III of the Companies Act 2013.

- The company must also attack its Financial Statements, along with other financial statements that contain the salient features of the subsidiary's finances in a manner as provided in the rules.

- In addition, if a company is interested in an affiliated company or joint venture, the accounting for that company and the joint venture shall be integrated.

- Affiliates are defined in the new Section 2 (6) for this purpose. The company has an important influence. Manages 20% of the company's total equity capital, or contractual business decisions.

- The Central Government has the authority to exempt companies from complying with any of the requirements created under this section.

General Instruction for Preparation of Balance Sheet and Statement of Profit and Loss of a Company (Section 129) | |||||||

General instructions | (1) where compliance with the requirements of the act including accounting standards as applicable to the companies require any change in treatment or disclosure including addition, amendment, substitution or deletion in the head or sub-head or any changes, in the financial statements or statements forming part thereof, the same shall be made and the requirements of this schedule shall stand modified accordingly.(2) the disclosure requirements specified in this schedule are in addition to and not in substitution of the disclosure requirements specified in the accounting standards prescribed under the companies act, 2013. Additional disclosures specified in the accounting standards shall be made in the notes to accounts or by way of additional statement unless required to be disclosed on the face of the financial statements. Similarly, all other disclosures as required by the companies’ act shall be made in the notes to accounts in addition to the requirements set out in this schedule. (3) (i) notes to accounts shall contain information in addition to that presented in the financial statements and shall provide where required A) narrative descriptions or disaggregation’s of items recognized in those statements; and B) information about items that do not qualify for recognition in those statements. (ii) each item on the face of the balance sheet and statement of profit and loss shall be cross-referenced to any related information in the notes to accounts. In preparing the financial statements including the notes to accounts, a balance shall be maintained between providing excessive detail that may not assist users of financial statements and not providing important information as a result of too much aggregation (4) (i) depending upon the turnover of the company, the figures appearing in the financial statements maybe rounded off as given below: —

| ||||||

(ii) once a unit of measurement is used, it shall be used uniformly in the financial statements. (5) except in the case of the first financial statements laid before the company (after its incorporation) the corresponding amounts (comparatives) for the immediately preceding reporting period for all items shown in the financial statements including notes shall also be given. (6) for the purpose of this schedule, the terms used herein shall be as per the applicable | |||||||

Accounting standards. | Note: —this part of schedule sets out the minimum requirements for on the face of the balance sheet, and the statement of profit and loss (hereinafter referred to as —financial statements || for the purpose of this schedule) and notes. Line items, sub-line items and sub-totals shall be presented as an addition or substitution on the face of the financial statements when such presentation is relevant to an understanding of the company’s financial position or performance or to cater to industry/sector-specific disclosure requirements or when required for compliance with the amendments to the companies act or under the Accounting Standards. | ||||||

Part 1- format of balance sheet

Name of the company

Balance sheet as at

| Notes | Current year | Previous year |

(in rs.) | (in rs.) | ||

Equity and liabilities |

|

|

|

Shareholder’s fund |

|

|

|

Share capital | 1 |

|

|

Reserves & surplus | 2 |

|

|

Money received against warrants |

|

|

|

|

|

|

|

|

|

|

|

Share application money pending allotment |

|

|

|

|

|

|

|

Non-current liabilities |

|

|

|

Long term borrowings | 3 |

|

|

Deferred tax liabilities (net) | 4 |

|

|

Other long-term liabilities | 5 |

|

|

Long term provisions | 6 |

|

|

|

|

|

|

Current liabilities |

|

|

|

Short term borrowings | 7 |

|

|

Trade payables | 8 |

|

|

Other current liabilities | 9 |

|

|

Short term provisions | 10 |

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

Assets |

|

|

|

Non-current assets |

|

|

|

Fixed assets | 11 |

|

|

Tangible assets |

|

|

|

Intangible assets |

|

|

|

Capital work-in-progress |

|

|

|

Intangible assets under development |

|

|

|

Non-current investments | 12 |

|

|

Deferred tax assets (net) |

|

|

|

Long term loans & advances | 13 |

|

|

Other non-current assets | 14 |

|

|

|

|

|

|

Current assets |

|

|

|

Current investments | 15 |

|

|

Inventories | 16 |

|

|

Trade receivables | 17 |

|

|

Cash and cash equivalents | 18 |

|

|

Short term loans & advances | 19 |

|

|

Other current assets | 20 |

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

Significant accounting policies |

|

|

|

The accompanying notes are an integral part of the financial statements |

|

|

|

General instructions for preparation of balance sheet

| Particulars |

|

|

1. | When an asset shall be classified as current? | If it satisfies any of the given criteria | (a) it is expected to be realised, or is intended for sale or consumption, in the company’s normal operating cycle; or (b) it is held primarily for the purpose of being traded; or (c) it is expected to be realised within twelve months after the reporting date; or (d) it is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date. |

2. | When an asset shall be classified as non-current? |

| Asset other than current asset shall be classified as non-current |

| Operating cycle | Time between the acquisition of assets for processing and Their realisation in cash or cash equivalents | Where the normal operating cycle cannot be identified: it is assumed to have a duration of 12 months |

| When liability shall be classified as current ? | If it satisfies any of thegiven criteria | (a) it is expected to be settled in the company normal operating cycle; or (b) it is held primarily for the purpose of being traded; or (c) it is due to be settled within twelve months after the reporting date; or (d)the company does not have an unconditional right to defer settlement of the liability for least twelve months after the reporting cm terms of a liability that could, at the option the counterparty, result in its settlement by the issue of equity instruments do not affect its classification. |

| When a liability shall be classified as non-current? |

| Liability other than current liability shall be classified as non-current. |

| When receivable shall be classified as a “trade receivable”? | If it is in respect of the amount due on account of goods sold or services rendered | In the normal course of business |

| When payable shall be classified as a “trade payable”? | If it is in respect of the amount due on account of goods purchased or services received | In the normal course of business |

1 | Share capital | For each class of share capital (different classes of preference shares to be treated separately) | A. The number and amount of shares authorized. B. The number of shares issued, subscribed and fully paid, and subscribed but not fully paid. C. Par value per share. D. A reconciliation of the number of shares outstanding at the beginning and at the end of the reporting period. E. The rights, preferences and restrictions attaching to each class of shares including restrictions on the distribution of dividends and the repayment of capital. F. Shares in respect of each class in the company held by its holding company or its ultimate holding company including shares held by or by subsidiaries or associates of the holding company or the ultimate holding company in aggregate. G. Shares in the company held by each shareholder holding more than 5 per cent, shares specifying the number of shares held. H. Shares reserved for issue under options and contracts/commitments for the sale of shares/disinvestment, including the terms and amounts. I. For the period of five years immediately preceding the date as at which the balance sheet is prepared. I. Aggregate number and class of shares allotted as fully paid-up pursuant to contract(s) without payment being received in cash. Ii. Aggregate number and class of shares allotted as fully paid-up by way of bonus shares. Iii. Aggregate number and class of shares bought back. J. Terms of any securities convertible into equity/preference shares issued along with the earliest date of conversion in descending order starting from the farthest such date. K. Calls unpaid (showing aggregate value of calls unpaid by directors and officers). L. Forfeited shares (amount originally paid-up). |

2 | Reserves and surplus | Shall be classified as | 1) capital reserves; 2) capital redemption reserve; 3) securities premium reserve; 4) debenture redemption reserve; 5) revaluation reserve; 6) share options outstanding account; 7) other reserves (specify the nature and purpose of each reserve and the amount in respect thereof); 8) surplus i.e., balance in statement of profit and loss disclosing allocations and appropriations such as dividend, bonus snares and transfer to/from reserves, etc.; (Additions and deductions since last balance sheet to be shown under each of the specified heads); |

Reserve specifically represented | By earmarked investments shall be termed as a “fund”. | ||

Debit balance of statement of profit and loss | Shall be shown as a negative figure under the head “surplus”. Similarly, the balance of “reserves and surplus”, after adjusting negative balance of surplus, if any, shall be shown under the head “reserves and surplus” even if the resulting figure is in the negative. | ||

3. | Long-term borrowings | Shall be classified as | 1) bonds/debentures; 2) term loans: (i) from banks. (ii) from other parties 3) deferred payment liabilities; 4) deposits; 5) loans and advances from related parties; 6) long term maturities of finance lease obligations; 7) other loans and advances (specify nature) |

Shall be further sub-classified as | Secured and unsecured (nature of security shall be specified separately in each case) | ||

Where loans have been guaranteed by directors or others | The aggregate amount of such loans under each head shall be disclosed. | ||

|

| Bonds/debentures (along with the rate of interest and particulars of redemption or conversion, as the case maybe) | Shall be stated in descending order of maturity or conversion, starting from farthest redemption or conversion date, as the case may be. Where bonds/debentures are redeemable by instalments, the date of maturity for this purpose must be reckoned as the date on which the first instalment becomes due. |

Particulars of any redeemed bonds/debentures | Which the company has power to reissue shall be disclosed | ||

Shall state | Terms of repayment of term loans and other loans | ||

Shall specify | Period and amount of continuing default as on the balance sheet date in repayment of loans and interest (separately in each case) | ||

4. | Other long-term liabilities | Shall be classified as | (1) trade payables; (2) others. |

5. | Long-term provisions | Shall be classified as | 1) provision for employee benefits; 2) others (specify nature). |

6. | Short-term borrowings | Shall be classified as | 1) loans repayable on demand; (i) from banks. (ii) from other parties. (2) loans and advances from related parties; (3) deposits; (4) other loans and advances (specify nature). |

Borrowings shall further be sub-classified as | Secured and unsecured (nature of security shall be specified separately in each case) | ||

Where loans have been guaranteed by directors or others | The aggregate amount of such loans under each head shall be disclosed. | ||

Shall specify | Period and amount of continuing default as on the balance sheet date in repayment of loans and interest (separately in each case) | ||

7. | Other current liabilities | Shall be classified as | 1) current maturities of long-term debt; 2) current maturities of finance lease obligations; 3) interest accrued but not due on borrowings; 4) interest accrued and due on borrowings; 5) income received in advance; 6) unpaid dividends; 7) application money received for allotment of securities and due for refund and interest accrued thereon. Share application money includes advances towards allotment of share capital. The terms and conditions including the number of shares proposed to be issued, the amount of premium, if any, and the period before which shares shall be allotted shall be disclosed. It shall also be disclosed whether the company has sufficient authorised capital to cover the share capital amount resulting from allotment of shares out of such share application money. Further, the period for which the share application money has been pending beyond the period for allotment as mentioned in the document inviting application for shares along with the reason for such share application money being pending shall be disclosed. Share application money not exceeding the issued capital and to the extent not refundable shall be shown under the head equity and share application money to the extent refundable, i.e., the amount in excess of subscription or in case the requirements of minimum subscription are not met, shall be separately shown under “other current liabilities”; 8) unpaid matured deposits and interest accrued thereon; 9) unpaid matured debentures and interest accrued thereon; 10) other payables (specify nature). |

8 | Short-term provisions | Shall be classified as | 1) provision for employee benefits 2) others (specify nature). |

9. | Tangible assets | Classification shall be given as | 1) land; 2) buildings; 3) plant and equipment; 4) furniture and fixtures; 5) vehicles; 6) office equipment; 7) others (specify nature). |

| Under lease shall be separately specified | Under each class of asset | |

| A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period | Showing additions, disposals, acquisitions through business combinations and other adjustments and the related depreciation and impairment losses/reversals shall be disclosed separately. | |

|

| Where sums have been written-off on a education of capital or revaluation of assets or where sums have been added on revaluation of assets, every balance sheet subsequent to date of such write-off, or addition | Shall show the reduced or increased figures as applicable and shall by way of a note also show the amount of the reduction or increase as applicable together with the date thereof for the first five years subsequent to the date of such reduction or increase. |

10 | Intangible assets | Classification shall be given as | 1) goodwill; 2) brands /trademarks; 3) computer software; 4) mastheads and publishing titles; 5) mining rights; 6) copyrights, and patents and other intellectual property rights, services and operating rights; 7) recipes, formulae, models, designs and prototypes; 8) licences and franchise; 9) others (specify nature). |

A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period | Showing additions, disposals, acquisitions through business combinations and other adjustments and the related depreciation and impairment losses/reversals shall be disclosed separately. | ||

Where sums have been written-off on a education of capital or revaluation of assets or where sums have been added on revaluation of assets, every balance sheet subsequent to date of such write-off, or addition | Shall show the reduced or increased figures as applicable and shall by way of a note also show the amount of the reduction or increase as applicable together with the date thereof for the first five years subsequent to the date of such reduction or increase. | ||

11. | Non-current investments | Shall be classified as trade investments and other investments and further classified as | 1) investment property; 2) investments in equity instruments; 3) investments in preference shares; 4) investments in government or trust securities; 5) investments in debentures or bonds; 6) investments in mutual funds; 7) investments in partnership firms; 8) other non-current investments (specify nature). Under each classification, details shall be given of names of the body’s corporate indicating separately whether such bodies are (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities in whom investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly-paid). In regard to investments in the capital of partnership firms, the names of the firms (with the names of all their partners, total capital and the shares of each partner) shall be given. |

Investments carried at other than at cost | Should be separately stated specifying the basis for valuation thereof; | ||

The following shall also be disclosed | 1) aggregate amount of quoted investments and market value thereof; 2) aggregate amount of unquoted investments; 3) aggregate provision for diminution in value of investments. | ||

12. | Long-term loans and advances | Loans and advances shall be classified as: | 1) capital advances; 2) security deposits; 3) loans and advances to related parties (giving details thereof); 4) other loans and advances (specify nature). |

The above shall also be separately sub-classified as: | 1) secured, considered good; 2) unsecured, considered good; 3) doubtful. | ||

Allowance for bad and doubtful loans and advances | Shall be disclosed under the relevant heads separately. | ||

Loans and advances due by directors or other officers of the company or any of them either severally or jointly with any other persons or amounts due by firms or private companies respectively in which any director is a partner or a director or a member | Should be separately stated. | ||

13. | Other non-current assets | Shall be classified as | 1) long-term trade receivables (including trade receivables on deferred credit terms); 2) others (specify nature); 3) long term trade receivables, shall be sub-classified as: |

| (i) secured, considered good; (ii) unsecured, considered good; (iii) doubtful Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately. Debts due by directors or other officers of the company or any of them either severally or jointly with any other person or debts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated. | ||

14. | Current investments | Shall be classified as | 1) investments in equity instruments; 2) investment in preference shares; 3) investments in government or trust securities: 4) investments in debentures or bonds; 5) investments in mutual funds; 6) investments in partnership firms; 7) other investments (specify nature). |

Under each classification | Details shall be given of names of the body’s corporate indicating separately whether such bodies are: (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities in whom investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly paid). In regard to investments in the capital of partnership firms, the names of the firms (with the names of all their partners, total capital and the shares of each partner) shall be given. | ||

|

| Following shall also be disclosed: | 1) the basis of valuation of individual investments 2) aggregate amount of quoted investments and market value thereof; 3) aggregate amount of unquoted investments; 4) aggregate provision made for diminution in value of investments |

15. | Inventories | Inventories shall be classified as: | 1) raw materials; 2) work-in-progress; 3) finished goods; 4) stock-in-trade (in respect of goods acquired for trading); 5) stores and spares; 6) loose tools; 7) others (specify nature) |

Goods-in-transit | Shall be disclosed under the relevant sub-head of inventories | ||

Mode of valuation | Shall be stated | ||

16. | Trade receivables | Shall separately state shall be sub-classified as | Aggregate amount of trade receivables outstanding for a period exceeding six months from the date they are due for payment |

1) secured, considered good; 2) unsecured, considered good; 3) doubtful. Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately. Debts due by directors or other officers of the company or any of them either severally or jointly with any other person or debts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated. | |||

17. | Cash and cash equivalents | Shall be classified as | 1) balances with banks; 2) cheques, drafts on hand; 3) cash on hand; 4) others (specify nature) |

Earmarked balances with banks (for example, for unpaid dividend) | Shall be separately stated | ||

Balances with banks to the extent held as margin money or security against the borrowings, guarantees, other commitments | Shall be disclosed separately. | ||

|

| Repatriation restrictions, if any, in respect of cash and bank balances | Shall be disclosed separately. |

Bank deposits with more than twelve months maturity | Shall be disclosed separately. | ||

18. | Short-term loans and advances | Shall be classified as: | 1) loans and advances to related parties (giving details thereof); 2) others (specify nature). |

Above shall also be sub-classified as | 1) secured, considered good; 2) unsecured, considered good; 3) doubtful. | ||

Allowance for bad and doubtful loans and advances | Shall be disclosed under the relevant heads separately | ||

Loans and advances due by directors or other officers of the company or any of them either severally or jointly with any other person or amounts due by firms or private companies respectively in which any director is a partner or a director or a member | Shall be separately stated | ||

19. | Other current assets (specify nature) | An all-inclusive heading | Which incorporates current assets that do not fit into any other asset categories |

20. | Contingent liabilities (to the extent not | Shall be classified as | 1) claims against the company not acknowledged as debt; |

| Provided for) commitments (to the extent not provided for) | Shall be classified as | 2) guarantees; 3) other money for which the company is contingently liable. 1) estimated amount of contracts remaining to be executed on capital account and not provided for; 2) uncalled liability on shares and other investments partly paid; 3) other commitments (specify nature). |

Part 1- Format of Balance Sheet

Name of the company

Balance sheet as at

| Notes | Current year | Previous year |

(in rs.) | (in rs.) | ||

Equity and liabilities |

|

|

|

Shareholder’s fund |

|

|

|

Share capital | 1 |

|

|

Reserves & surplus | 2 |

|

|

Money received against warrants |

|

|

|

|

|

|

|

|

|

|

|

Share application money pending allotment |

|

|

|

|

|

|

|

Non-current liabilities |

|

|

|

Long term borrowings | 3 |

|

|

Deferred tax liabilities (net) | 4 |

|

|

Other long-term liabilities | 5 |

|

|

Long term provisions | 6 |

|

|

|

|

|

|

Current liabilities |

|

|

|

Short term borrowings | 7 |

|

|

Trade payables | 8 |

|

|

Other current liabilities | 9 |

|

|

Short term provisions | 10 |

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

Assets |

|

|

|

Non-current assets |

|

|

|

Fixed assets | 11 |

|

|

Tangible assets |

|

|

|

Intangible assets |

|

|

|

Capital work-in-progress |

|

|

|

Intangible assets under development |

|

|

|

Non-current investments | 12 |

|

|

Deferred tax assets (net) |

|

|

|

Long term loans & advances | 13 |

|

|

Other non-current assets | 14 |

|

|

|

|

|

|

Current assets |

|

|

|

Current investments | 15 |

|

|

Inventories | 16 |

|

|

Trade receivables | 17 |

|

|

Cash and cash equivalents | 18 |

|

|

Short term loans & advances | 19 |

|

|

Other current assets | 20 |

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

Significant accounting policies |

|

|

|

The accompanying notes are an integral part of the financial statements |

|

|

|

General instructions for preparation of Balance Sheet

| Particulars |

|

|

1. | When an asset shall be classified as current? | If it satisfies any of the given criteria | (a) it is expected to be realised, or is intended for sale or consumption, in the company’s normal operating cycle; or (b) it is held primarily for the purpose of being traded; or (c) it is expected to be realised within twelve months after the reporting date; or (d) it is cash or cash equivalent unless it is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting date. |

2. | When an asset shall be classified as non-current? |

| Asset other than current asset shall be classified as non-current |

| Operating cycle | Time between the acquisition of assets for processing and Their realisation in cash or cash equivalents | Where the normal operating cycle cannot be identified: it is assumed to have a duration of 12 months |

| When liability shall be classified as current? | If it satisfies any of the given criteria | (a) it is expected to be settled in the company normal operating cycle; or (b) it is held primarily for the purpose of being traded; or (c) it is due to be settled within twelve months after the reporting date; or (d)the company does not have an unconditional right to defer settlement of the liability for least twelve months after the reporting cm terms of a liability that could, at the option the counterparty, result in its settlement by the issue of equity instruments do not affect its classification. |

| When a liability shall be classified as non-current? |

| Liability other than current liability shall be classified as non-current. |

| When receivable shall be classified as a “trade receivable”? | If it is in respect of the amount due on account of goods sold or services rendered | In the normal course of business |

| When payable shall be classified as a “trade payable”? | If it is in respect of the amount due on account of goods purchased or services received | In the normal course of business |

1 | Share capital | For each class of share capital (different classes of preference shares to be treated separately) | A. The number and amount of shares authorized. B. The number of shares issued, subscribed and fully paid, and subscribed but not fully paid. C. Par value per share. D. A reconciliation of the number of shares outstanding at the beginning and at the end of the reporting period. E. The rights, preferences and restrictions attaching to each class of shares including restrictions on the distribution of dividends and the repayment of capital. F. Shares in respect of each class in the company held by its holding company or its ultimate holding company including shares held by or by subsidiaries or associates of the holding company or the ultimate holding company in aggregate. G. Shares in the company held by each shareholder holding more than 5 per cent, shares specifying the number of shares held. H. Shares reserved for issue under options and contracts/commitments for the sale of shares/disinvestment, including the terms and amounts. I. For the period of five years immediately preceding the date as at which the balance sheet is prepared. I. Aggregate number and class of shares allotted as fully paid-up pursuant to contract(s) without payment being received in cash. Ii. Aggregate number and class of shares allotted as fully paid-up by way of bonus shares. Iii. Aggregate number and class of shares bought back. J. Terms of any securities convertible into equity/preference shares issued along with the earliest date of conversion in descending order starting from the farthest such date. K. Calls unpaid (showing aggregate value of calls unpaid by directors and officers). L. Forfeited shares (amount originally paid-up). |

2 | Reserves and surplus | Shall be classified as | 1) capital reserves; 2) capital redemption reserve; 3) securities premium reserve; 4) debenture redemption reserve; 5) revaluation reserve; 6) share options outstanding account; 7) other reserves(specify the nature and purpose of each reserve and the amount in respect thereof); 8) surplus i.e., balance in statement of profit and loss disclosing allocations and appropriations such as dividend, bonus snares and transfer to/from reserves, etc.; (additions and deductions since last balance sheet to be shown under each of the specified heads); |

Reserve specifically represented | By earmarked investments shall be termed as a “fund”. | ||

Debit balance of statement of profit and loss | Shall be shown as a negative figure under the head “surplus”. Similarly, the balance of “reserves and surplus”, after adjusting negative balance of surplus, if any, shall be shown under the head “reserves and surplus” even if the resulting figure is in the negative. | ||

3. | Long-term borrowings | Shall be classified as | 1) bonds/debentures; 2) term loans: (i) from banks. (ii) from other parties 3) deferred payment liabilities; 4) deposits; 5) loans and advances from related parties; 6) long term maturities of finance lease obligations; 7) other loans and advances (specify nature) |

Shall be further sub-classified as | Secured and unsecured (nature of security shall be specified separately in each case) | ||

Where loans have been guaranteed by directors or others | The aggregate amount of such loans under each head shall be disclosed. | ||

|

| Bonds/debentures (along with the rate of interest and particulars of redemption or conversion, as the case maybe) | Shall be stated in descending order of maturity or conversion, starting from farthest redemption or conversion date, as the case may be. Where bonds/debentures are redeemable by instalments, the date of maturity for this purpose must be reckoned as the date on which the first instalment becomes due. |

Particulars of any redeemed bonds/debentures | Which the company has power to reissue shall be disclosed | ||

Shall state | Terms of repayment of term loans and other loans | ||

Shall specify | Period and amount of continuing default as on the balance sheet date in repayment of loans and interest(separately in each case) | ||

4. | Other long-term liabilities | Shall be classified as | (1) trade payables; (2) others. |

5. | Long-term provisions | Shall be classified as | 1) provision for employee benefits; 2) others (specify nature). |

6. | Short-term borrowings | Shall be classified as | 1) loans repayable on demand; (i) from banks. (ii) from other parties. (2) loans and advances from related parties; (3) deposits; (4) other loans and advances (specify nature). |

Borrowings shall further be sub-classified as | Secured and unsecured(nature of security shall be specified separately in each case) | ||

Where loans have been guaranteed by directors or others | The aggregate amount of such loans under each head shall be disclosed. | ||

Shall specify | Period and amount of continuing default as on the balance sheet date in repayment of loans and interest (separately in each case) | ||

7. | Other current liabilities | Shall be classified as | 1) current maturities of long-term debt; 2) current maturities of finance lease obligations; 3) interest accrued but not due on borrowings; 4) interest accrued and due on borrowings; 5) income received in advance; 6) unpaid jividends; 7) application money received for allotment of securities and due for refund and interest accrued thereon. Share application money includes advances towards allotment of share capital. The terms and conditions including the number of shares proposed to be issued, the amount of premium, if any, and the period before which shares shall be allotted shall be disclosed. It shall also be disclosed whether the company has sufficient authorised capital to cover the share capital amount resulting from allotment of shares out of such share application money. Further, the period for which the share application money has been pending beyond the period for allotment as mentioned in the document inviting application for shares along with the reason for such share application money being pending shall be disclosed. Share application money not exceeding the issued capital and to the extent not refundable shall be shown under the head equity and share application money to the extent refundable, i.e., the amount in excess of subscription or in case the requirements of minimum subscription are not met, shall be separately shown under “other current liabilities”; 8) unpaid matured deposits and interest accrued thereon; 9) unpaid matured debentures and interest accrued thereon; 10) other payables (specify nature). |

8 | Short-term provisions | Shall be classified as | 1) provision for employee benefits 2) others (specify nature). |

9. | Tangible assets | Classification shall be given as | 1) land; 2) buildings; 3) plant and equipment; 4) furniture and fixtures; 5) vehicles; 6) office equipment; 7) others (specify nature). |

| Under lease shall be separately specified | Under each class of asset | |

| A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period | Showing additions, disposals, acquisitions through business combinations and other adjustments and the related depreciation and impairment losses/reversals shall be disclosed separately. | |

|

| Where sums have been written-off on a eduction of capital or revaluation of assets or where sums have been added on revaluation of assets, every balance sheet subsequent to date of such write-off, or addition | Shall show the reduced or increased figures as applicable and shall by way of a note also show the amount of the reduction or increase as applicable together with the date thereof for the first five years subsequent to the date of such reduction or increase. |

10 | Intangible assets | Classification shall be given as | 1) goodwill; 2) brands /trademarks; 3) computer software; 4) mastheads and publishing titles; 5) mining rights; 6) copyrights, and patents and other intellectual property rights, services and operating rights; 7) recipes, formulae, models, designs and prototypes; 8) licences and franchise; 9) others (specify nature). |

A reconciliation of the gross and net carrying amounts of each class of assets at the beginning and end of the reporting period | Showing additions, disposals, acquisitions through business combinations and other adjustments and the related depreciation and impairment losses/reversals shall be disclosed separately. | ||

Where sums have been written-off on a eduction of capital or revaluation of assets or where sums have been added on revaluation of assets, every balance sheet subsequent to date of such write-off, or addition | Shall show the reduced or increased figures as applicable and shall by way of a note also show the amount of the reduction or increase as applicable together with the date thereof for the first five years subsequent to the date of such reduction or increase. | ||

11. | Non-current investments | Shall be classified as trade investments and other investments and further classified as | 1) investment property; 2) investments in equity instruments; 3) investments in preference shares; 4) investments in government or trust securities; 5) investments in debentures or bonds; 6) investments in mutual funds; 7) investments in partnership firms; 8) other non-current investments (specify nature). Under each classification, details shall be given of names of the bodies corporate indicating separately whether such bodies are (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities in whom investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly-paid). In regard to investments in the capital of partnership firms, the names of the firms (with the names of all their partners, total capital and the shares of each partner) shall be given. |

Investments carried at other than at cost | Should be separately stated specifying the basis for valuation thereof; | ||

The following shall also be disclosed | 1) aggregate amount of quoted investments and market value thereof; 2) aggregate amount of unquoted investments; 3) aggregate provision for diminution in value of investments. | ||

12. | Long-term loans and advances | Loans and advances shall be classified as: | 1) capital advances; 2) security deposits; 3) loans and advances to related parties (giving details thereof); 4) other loans and advances (specify nature). |

The above shall also be separately sub-classified as: | 1) secured, considered good; 2) unsecured, considered good; 3) doubtful. | ||

Allowance for bad and doubtful loans and advances | Shall be disclosed under the relevant heads separately. | ||

Loans and advances due by directors or other officers of the company or any of them either severally or jointly with any other persons or amounts due by firms or private companies respectively in which any director is a partner or a director or a member | Should be separately stated. | ||

13. | Other non-current assets | Shall be classified as | 1) long-term trade receivables (including trade receivables on deferred credit terms); 2) others (specify nature); 3) long term trade receivables, shall be sub-classified as: |

| (i) secured, considered good; (ii) unsecured, considered good; (iii) doubtful Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately. Debts due by directors or other officers of the company or any of them either severally or jointly with any other person or debts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated. | ||

14. | Current investments | Shall be classified as | 1) investments in equity instruments; 2) investment in preference shares; 3) investments in government or trust securities: 4) investments in debentures or bonds; 5) investments in mutual funds; 6) investments in partnership firms; 7) other investments (specify nature). |

Under each classification | Details shall be given of names of the bodies corporate indicating separately whether such bodies are: (i) subsidiaries, (ii) associates, (iii) joint ventures, or (iv) controlled special purpose entities in whom investments have been made and the nature and extent of the investment so made in each such body corporate (showing separately investments which are partly paid). In regard to investments in the capital of partnership firms, the names of the firms (with the names of all their partners, total capital and the shares of each partner) shall be given. | ||

|

| Following shall also be disclosed: | 1) the basis of valuation of individual investments 2) aggregate amount of quoted investments and market value thereof; 3) aggregate amount of unquoted investments; 4) aggregate provision made for diminution in value of investments |

15. | Inventories | Inventories shall be classified as: | 1) raw materials; 2) work-in-progress; 3) finished goods; 4) stock-in-trade (in respect of goods acquired for trading); 5) stores and spares; 6) loose tools; 7) others (specify nature) |

Goods-in-transit | Shall be disclosed under the relevant sub-head of inventories | ||

Mode of valuation | Shall be stated | ||

16. | Trade receivables | Shall separately state shall be sub-classified as | Aggregate amount of trade receivables outstanding for a period exceeding six months from the date they are due for payment |

1) secured, considered good; 2) unsecured, considered good; 3) doubtful. Allowance for bad and doubtful debts shall be disclosed under the relevant heads separately. Debts due by directors or other officers of the company or any of them either severally or jointly with any other person or debts due by firms or private companies respectively in which any director is a partner or a director or a member should be separately stated. | |||

17. | Cash and cash equivalents | Shall be classified as | 1) balances with banks; 2) cheques, drafts on hand; 3) cash on hand; 4) others (specify nature) |

Earmarked balances with banks (for example, for unpaid dividend) | Shall be separately stated | ||

Balances with banks to the extent held as margin money or security against the borrowings, guarantees, other commitments | Shall be disclosed separately. | ||

|

| Repatriation restrictions, if any, in respect of cash and bank balances | Shall be disclosed separately. |

Bank deposits with more than twelve months maturity | Shall be disclosed separately. | ||

18. | Short-term loans and advances | Shall be classified as: | 1) loans and advances to related parties (giving details thereof); 2) others (specify nature). |

Above shall also be sub-classified as | 1) secured, considered good; 2) unsecured, considered good; 3) doubtful. | ||

Allowance for bad and doubtful loans and advances | Shall be disclosed under the relevant heads separately | ||

Loans and advances due by directors or other officers of the company or any of them either severally or jointly with any other person or amounts due by firms or private companies respectively in which any director is a partner or a director or a member | Shall be separately stated | ||

19. | Other current assets (specify nature) | An all-inclusive heading | Which incorporates current assets that do not fit into any other asset categories |

20. | Contingent liabilities (to the extent not | Shall be classified as | 1) claims against the company not acknowledged as debt; |

| Provided for) commitments (to the extent not provided for) | Shall be classified as | 2) guarantees; 3) other money for which the company is contingently liable. 1) estimated amount of contracts remaining to be executed on capital account and not provided for; 2) uncalled liability on shares and other investments partly paid; 3) other commitments (specify nature). |

Part 2- Format of Statement of Profit or Loss

| Notes | Current year | Previous year |

(in rs.) | (in rs.) | ||

Continuing operations |

|

|

|

|

|

|

|

Revenue | 2 |

|

|

Revenue from operations |

|

|

|

Less : excise duty |

|

|

|

Revenue from operations (net) | 21 |

|

|

Other income | 22 |

|

|

|

|

|

|

Total revenue |

|

|

|

|

|

|

|

Expenses |

|

|

|

Cost of materials consumed | 23 |

|

|

Purchases of stock-in-trade | 24 |

|

|

(increase)/decrease in inventories of fg/wip/stock-in-trade | 25 |

|

|

Employee benefit expenses | 26 |

|

|

Finance cost | 27 |

|

|

Depreciation & amortisation expenses | 28 |

|

|

Other expenses | 29 |

|

|

Total expenses |

|

|

|

|

|

|

|

Profit before exceptional and extraordinary items & tax |

|

|

|

Exceptional income / expenses |

|

|

|

|

|

|

|

Profit before extraordinary items & tax |

|

|

|

Prior period items |

|

|

|

Extraordinary items |

|

|

|

|

|

|

|

Profit before tax |

|

|

|

Provision for taxation | 30 |

|

|

|

|

|

|

Profit/(loss) for the period from continuing operations |

|

|

|

|

|

|

|

Discontinuing operations |

|

|

|

|

|

|

|

Profit/(loss) from discontinuing operations |

|

|

|

Tax expense of discontinuing operations |

|

|

|

Profit/(loss) from discontinuing operations after tax |

|

|

|

|

|

|

|

Profit/(loss) for the period |

|

|

|

|

|

|

|

Earnings per share | 3 |

|

|

Basic eps (in rs.) |

|

|

|

Diluted eps (in rs.) |

|

|

|

Details to be disclosed in the notes

a. Amount of “Revenue from operations” will be divided in –

i. Sale of products (including excise duty)

Ii. Sale of services

Iii. Other operating revenues

b. Finance cost will be distributed in –

i. Interest

Ii. Dividend on redeemable preference shares

Iii. Exchange Differences regarded as an adjustment to borrowing costs, and

Iv. Other borrowing costs (if any)

c. Other Income will be distributed in –

i. Interest Income,

Ii. Dividend Income, and

Iii. Other non-operating income

d. Other Comprehensive Income shall be classified into –

i. Items that will not be reclassified to profit or loss

1. Changes in revaluation surplus

2. Remeasurements of the defined benefit plans

3. Equity Instruments through Other Comprehensive Income

4. Fair value changes relating to own credit risk of financial liabilities designated at fair value through profit or loss

5.Share of Other Comprehensive Income in Associates and Joint Ventures, to the extent not to be classified into profit or loss, and

6. Others

Ii. Items that will be reclassified to profit or loss

1. Exchange differences in translating the financial statements of a foreign operation;

2. Debt instruments through Other Comprehensive Income;

3. The effective portion of gains and loss on hedging instruments in a cash flow hedge;

4. Share of other comprehensive income in Associates and Joint Ventures, to the extent to be classified into profit or loss; and

5. Others

e. Employees benefit expense

i. Salaries and wages,

Ii. Contribution to provident and other funds,

Iii. Share-based payments to employees

Iv. Staff welfare expenses

f. Depreciation and amortisation expense,

g. Interest Income,

h. Interest Expense,

i. Dividend Income,

j. Net gain or loss on sale of investments,

k. Net gain or loss on foreign currency transaction and translation (other than considered as finance cost),

l. Payment to the auditor as

i. Auditor

Ii. For taxation matters

Iii. For company law matters

Iv. For other services

v. For reimbursement of expenses

m. Amount of expenses incurred on corporate social responsibility activities,

n. Details of items of exceptional nature